In the last few months, the Federal Reserve has signaled that it is prepared to cut interest rates. Today’s 50bps rate cut, however, exceeded most expectations.

As ZeroHedge has noted, “only 9 of 113 economists surveyed” expected this sort of move, and the Fed’s own dot plot shows a growing appetite for more aggressive action in the near future.

Amazing what an 818K downward jobs revision that “nobody could have seen coming because the Biden economy was so strong” will do... pic.twitter.com/xvTwmE4eUJ

— zerohedge (@zerohedge) September 18, 2024

The Fed’s actions are best understood as acknowledging the obvious: the regime has been gaslighting the public about the economy. Despite the constant assistance from the Biden-Harris Administration and their reliable allies in the media that the economy is strong, today’s Fed action was a crisis-level response.

What changed? The job market is an obvious one. Once the go-to argument for the strength of the American economy, official numbers show there are now fewer full-time jobs in America than there were a year ago. This follows significant revisions to jobs reports that overstated almost a million jobs.

Of course, at the same time the Fed still continues to battle inflation that is well beyond its 2 percent target, with assets like housing, food prices, and stocks still at significant highs.

Have no fear, though; Chairman Jerome Powell assured the American economy is still “strong overall.” To further this point, the Fed pushed its go-to propaganda, with a variety of forecasts predicting that inflation will continue to go down, unemployment will continue to fall, and that all will be down.

This game has become quite predictable, as Jonathan Newman noted on X.

I was right! https://t.co/cteAcXPCPH pic.twitter.com/FIqUOWdk4z

— Jonathan Newman (@NewmanJ_R) September 18, 2024

The Fed’s specialty is propaganda through data, with a long record of failure. This is by design. Their communication tools must work in overtime, particularly in the face of a decision like this, to avoid “spooking markets”, though this veneer is easy to see through.

As Ryan McMaken noted recently, the Fed’s actions are itself one of the best indicators of a recession on the horizon.

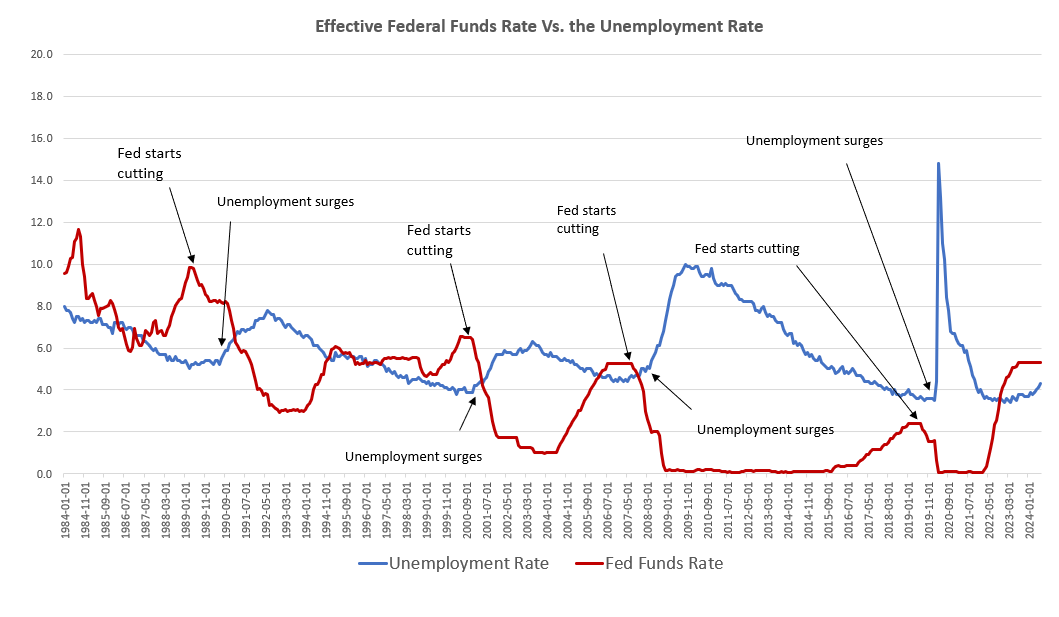

If we look back at the relationship between rate cuts and recessions, we see that in almost every case that recessions begin shortly after the Fed starts a cycle of rate cuts. The fed started cutting the Fed funds rate in 1989. Then we got the recession of the early 90s. In late 2000, the fed started the rate cuts again. We got a recession in 2001. The Fed did it again in late 2007. The recession began in December 2007, followed by a financial crisis several months later. This relationship even holds for the 2020 recession because even without covid there would have been a recession in late 2020. The Fed had begun to ease the target rate in summer 2019.

There was no soft landing in any of these cases, even though it has been routine for the Fed to promise a soft landing at least as early as 2001.

Fed rate cuts don’t cause recessions, of course. The boom-bust cycle is caused by reckless Fed-driven money creation.

But it makes sense that the Fed hits the panic button and starts cutting rates when it does because the Fed is reacting to fears about impending recessions. The same is true this time around. The Fed has no special prediction skills, so it sees what the rest of us see: a weakening economy and a much less rosy employment picture than what was sold to us by the administration over the past year. July’s weak jobs report with rising unemployment, combined with this week’s massive downward revision in 2023-2024 jobs numbers, gives us good reason to figure that the Fed is now trying to prevent a recession by flooding the economy with more easy money.

Naturally, when it comes to Fed policy, we cannot ignore the political environment around it. While it strongly holds on to a claim of “independence,” there is a long history of politics having direct influence over the actions of America’s central bank. There are certainly many within the Eccles Building hoping that today’s dovish decision will help create a sugar high going into November.

Any short-term relief will come at the expense of longer-term pain as the various consequences of the Fed’s monetary manipulation continues to undermine the foundations of the real economy.

Full story here Are you the author?Tags: Featured,newsletter