The FDIC added 11 new banks to its Problem List in the first quarter of 2024, bringing the total to 63. The specific banks on this are kept confidential, but the endemic, underlying issues in the commercial banking sector are increasingly obvious.

Interest Rate Risk and Liquidity

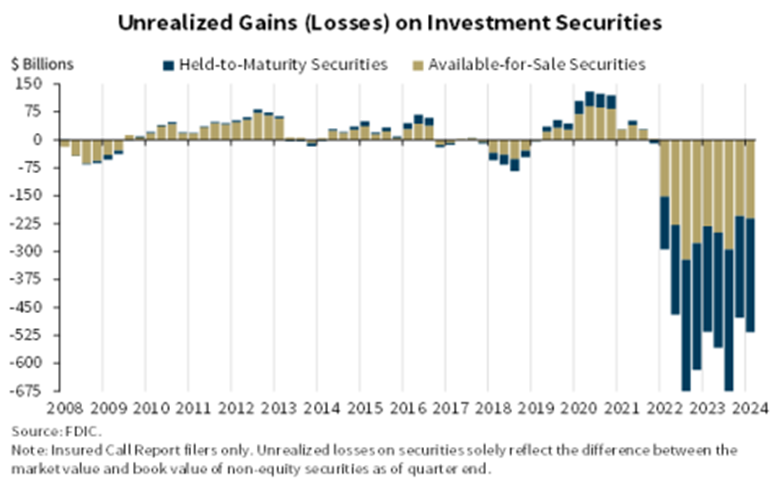

The FIDC reported that “Unrealized losses on securities totaled $516.5 billion in the first quarter, an increase of $38.9 billion (8.2 percent) from fourth quarter 2023. Higher unrealized losses on residential mortgage-backed securities accounted for almost 95 percent of the total decrease. Mortgage rates increased in the first quarter, which placed downward pressure on the underlying values of such investments.”

Source: Quarterly Banking Profile First Quarter 2024

https://www.fdic.gov/news/speeches/fdic-quarterly-banking-profile-first-quarter-2024

The public has paid more attention to the unrealized loss on Held-to-Maturity (HTM) securities since the collapse of Silicon Valley Bank, and for good reason. These losses do not affect the bank’s income statement but are devastating if the bank faces a major deposit outflow and has to sell the HTM securities to maintain liquidity.

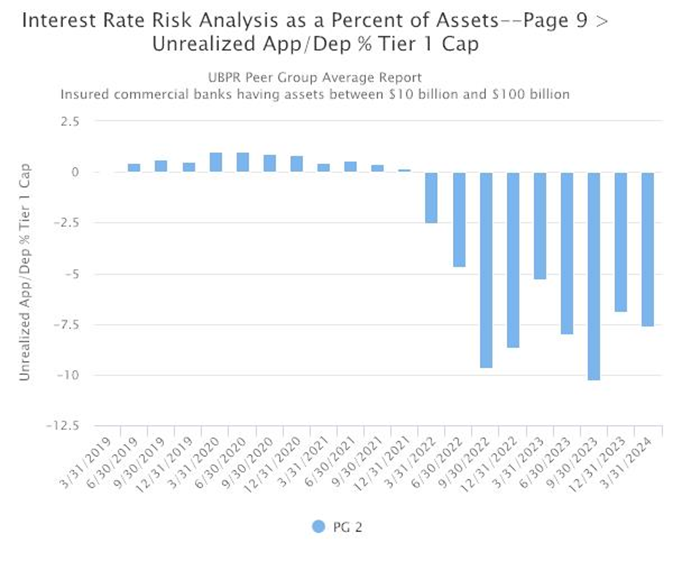

Source: FFIEC Unrealized Loss as percent of Tier 1 Capital. Peer Group 2 Average

https://cdr.ffiec.gov/public/ManageFacsimiles.aspx

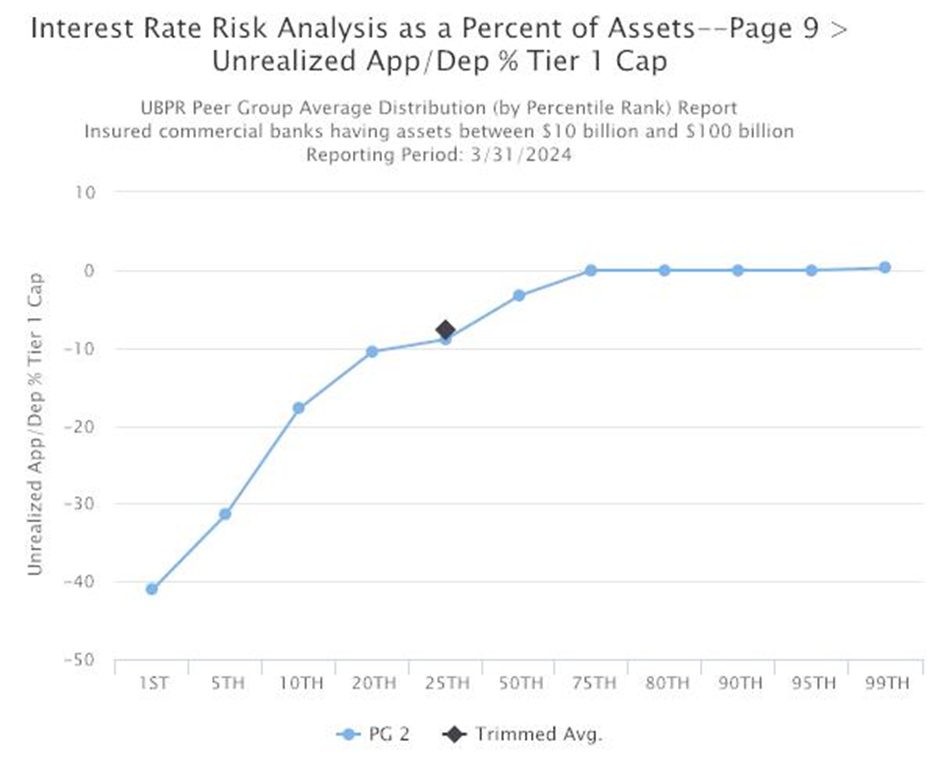

In this graph we see the unrealized gain/loss on HTM securities as a percentage of Tier 1 Capital (a combination of cash and highly liquid assets). Tier 1 is the liquidity cushion that banks need to cover deposit outflows. To interpret this graph, think of it in terms of the amount of potential liquidity banks are losing to rising interest rates every quarter. For example, a -10 percent means that, for every $100 of cushion, the bank lost $10 of fair value for its HTM securities. FFIEC Peer Group 2 ($10 - $100 billion in total assets) is a good gauge for the overall health of the banking system since it includes most of the regional giants like Zion’s National, First Interstate, Western Alliance, and Bank OZK. Peer Group 2 banks suffered an average of -7.61 percent of Tier 1 this quarter; 20 percent of Peer Group 2 banks suffered a loss of -10.47 percent or more.

Source: FFIEC Unrealized Loss as percent of Tier 1 Capital for Peer Group 2: Peer Group Average Distribution Report

https://cdr.ffiec.gov/public/ManageFacsimiles.aspx

Deteriorating Credit Quality

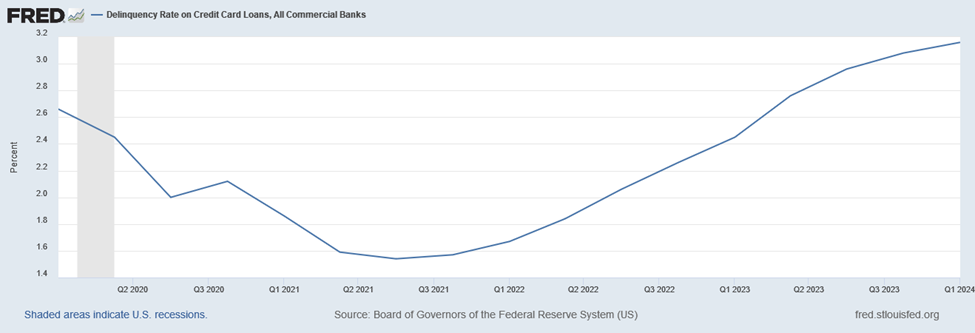

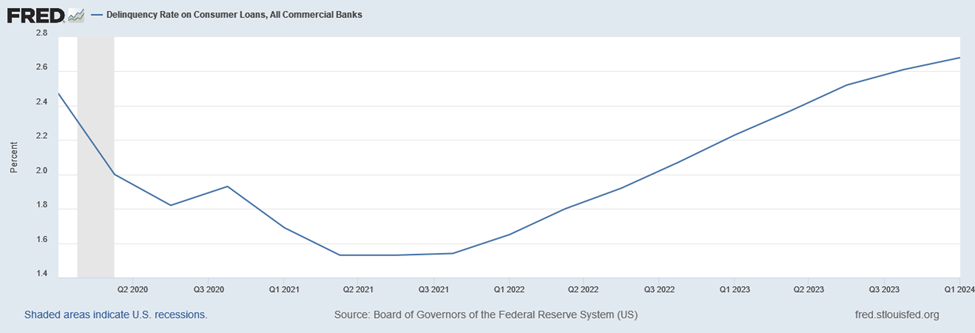

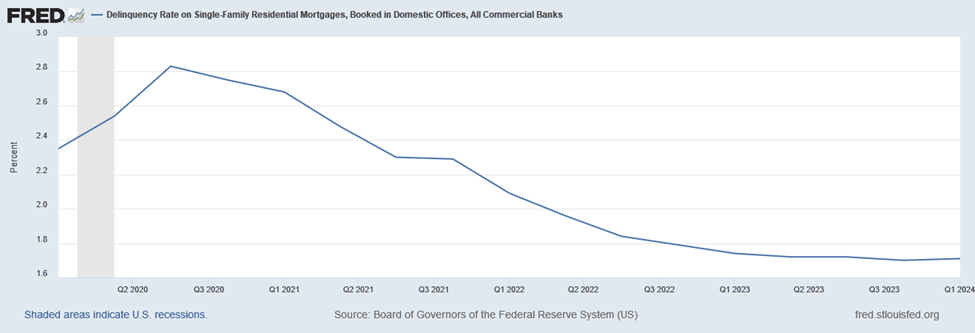

The banking industry has not seen a noticeable increase in residential mortgage delinquencies yet, but it has seen a noticeable increase in consumer credit delinquencies. When households face a tightening bottom line due to inflation, it’s generally safer to fall behind on credit card payments than mortgage payments, since the bank can repossess your house in the latter case.

FRED: Delinquency Rates on Credit Card Loans (All Commercial Banks).

Source : https://fred.stlouisfed.org/series/DRCCLACBS#

FRED: Delinquency Rates on Consumer Loans (All Commercial Banks).

Source : https://fred.stlouisfed.org/series/DRCLACBS

FRED: Delinquency Rates on Single Family Mortgages (All Commercial Banks). https://fred.stlouisfed.org/series/DRSFRMACBS

https://fred.stlouisfed.org/series/DRSFRMACBS

Commercial Real Estate Exposure

A final concerning trend in the banking milieu is the massive exposure to commercial real estate (CRE). According to a recent analysis from Florida Atlantic University, 67 of the 157 largest banks in the U.S. (total assets exceeding $10 billion) have CRE exposure exceeding 300 percent of their total capital. 9 of these banks have CRE exposure at or exceeding 500 percent of capital. Florida Atlantic included a handy screener in on their website that allows the user to sort through the banks. Among the highest concentrated are the Peer Group 2 regional banks discussed earlier: Zion’s National (439.7 percent of CRE to equity), First Interstate (347.9 percent), and Bank OZK (620.5 percent).

The Big Picture

Whether Powell will lower rates before the election is still uncertain, but even a major pivot is not going to reverse the decline in credit quality or fix bank balance sheets. In the case of major bank failures, may see the Fed bail out underwater securities portfolios through direct asset purchases, or a reversion to indefinite rounds quantitative easing. Either way, it is clear that the chickens are coming home to roost in the commercial banking industry.

Full story here Are you the author?Tags: Featured,newsletter