In March 2009, in the midst of recession, then Treasury secretary Timothy Geithner was pressed to respond on the question of whether or not another currency—possibly the IMF’s special drawing rights (SDRs)—might displace the US dollar as the dominant global reserve currency. Geithner responded that he’s open to more use of SDRs but then felt the need to clarify with “The dollar remains the world’s dominant reserve currency and I think that’s likely to continue for a long period of time.”

It’s not a coincidence that this occurred in the context of financial crises, recession, and some big changes in the global economy. Crises have a tendency to bring out questions about the dollar’s reserve-currency status. Similar discussions occurred in the late 1970s as the United States was experiencing stagflation. Policy makers and central bankers began discussing the possible benefits of “diversifying” away from the dollar in the global economy. It is true that during the 1970s the dollar’s reserve-currency status suffered somewhat to the benefit of the deutsche mark and Japanese yen. Nonetheless, decades later, the dollar remains the undisputed favorite.

Yet no global reserve currency retains its place forever. History is a graveyard for currencies that were once considered essential to global commerce, from the Spanish silver dollar in the sixteenth century to the Dutch guilder and French franc of later times.

The last time we saw a dominant global currency give way to its successor was in the first half of the twentieth century, when British pound sterling lost its position as the preferred global reserve currency and was replaced by the US dollar. History never quite repeats itself, but the story behind the fall of sterling and the rise of the dollar contains many familiar events such as war, inflation, and government spending. Many observers of the global currency scene continue to regard the dollar as untouchable, but their predecessors said the same thing about sterling. Indeed, the decline of Britain’s once exalted currency is a powerful cautionary tale about how global currencies lose their power.

The Rise of Pound Sterling

In its day, sterling was immensely important and central to global commerce. Since at least the early eighteenth century, sterling was among the most frequently traded and most trusted national currencies, and this helped establish London as an international financial center. Even after the Napoleonic Wars—period during which sterling was temporarily delinked from gold—the currency’s relatively swift return to gold ensured sterling would dominate international finance by the late nineteenth century. This dominance was greatly enhanced by the fact the British economy was among the most industrialized and strongest in the world. On top of this, the British state was thought to intervene in its monetary system less than other states and also believed to be more likely to make good on promises to convert banknotes into gold.

As Bo Karlstroem notes, during the late nineteenth century:

The overwhelming predominance of Great Britain in world trade . . . reflected the particular economic strength of Great Britain as the first country to reap the benefits of the industrial revolution. British industrial goods were in demand the world over, while Britain had a great appetite for raw materials and foodstuffs; it has been estimated that in 1860 the British market was absorbing over 30 per cent of the exports of all the other countries in the world. The share fell as other countries, notably Germany and France, reached the point of “take-off” into industrial growth, but in the 1890’s the percentage was still over 20. The trading in goods was accompanied by a wide range of exports of services, such as shipping and insurance, from Great Britain.

This was about more than the mere size of the British economy, however. After all, the American economy had surpassed the British economy in size in the 1870s. By 1900, the German economy was larger than the British economy as well. Yet until the First World War, sterling’s role in international reserves, trade, and investment remained disproportionately large.

For example, according to Barry Eichengreen, the sterling market was especially “deep and liquid” owing partly to the size of London’s global networks with the rest of the British Empire. Yet also key was the British regime’s reluctance to meddle in the gold mechanism, Eichengreen noted: “While the Bank of England occasionally resorted to the gold devices, modifying the effective price of gold, it never seriously interfered with the freedom of nonresidents to export gold. Few if any other financial centers could claim all these attributes.” At this time, both the Bank of France and the German Reichsbank engaged in various policies to make it more difficult for market participants to export gold. Meanwhile, the US dollar remained in the race to become a global reserve currency. Jeffrey Frankel explains that

prior to 1913, the dollar’s main problem was not size (the first criterion for an international currency) since the U.S. economy had surpassed the UK economy, at least as measured by national output, in 1872. Rather, the country lacked financial markets that were deep, liquid, dependable, and open. Indeed, it even lacked a central bank, which was considered a prerequisite for the development of markets in instruments such as bankers’ acceptances.

Then as now, regimes and their friends in the financial sector viewed central banks as the best insurers of liquidity and of uniformity in a currency. It is no coincidence, for example, that sterling’s rise to power in Europe came in the decades following the British “financial revolution” and the creation of the Bank of England. Because the Americans lacked the institutional framework preferred by global investors and bankers, sterling reigned supreme throughout the nineteenth century and into the early twentieth century.

(It should be noted this lack of a central bank and a global currency did not prevent enormous gains in ordinary Americans’ standard of living throughout the late nineteenth and early twentieth centuries.)

World War One Changed Everything

Sterling’s undisputed reign came to an end with the First World War. The British state’s massive war debts and its abandonment of the classical gold standard crippled sterling’s ability to attract the same level of trust and investment it had before the war. Sterling’s competitors—except for the dollar—were sidelined as well. Karlstroem writes:

Many European countries introduced various kinds of controls on foreign exchange transactions during World War I, mainly in order to conserve their holdings of dollars; and European central banks stopped converting their currencies into gold on demand, thereby turning away from the gold standard. The United States, however, continued to follow its policy of convertibility. At the end of the war, there was a large pent-up demand from Europe for U.S. goods, and this demand was backed by rather substantial holdings of dollars. The United States was, of course, willing to supply these goods and it was also capable of doing so, not having suffered from the destruction of production facilities caused by the war as other countries had done.

The world’s central banks embraced both the dollar and the US’s new central bank, investing in dollars as reserves while private-sector bankers and importers in Europe demanded dollars to buy American goods.

Competition among Global Currencies

Yet sterling did not totally abandon the field to the dollar. When exactly the dollar overtook sterling as the most preferred currency is still a matter of debate, and it is an empirical question. In any case, there is good reason to believe that the dollar's position against sterling improved substantially after sterling went off the gold standard in 1931. That was not the end of the story, however, because dollar itself went off the gold standard two years later. According to Eichengreen and Marc Flandreau, the dollar eclipsed sterling as early as “the mid-1920s and . . . then widened its lead in the second half of the decade," but "With the devaluation of the dollar in 1933, sterling regained its place as the leading reserve currency. Contrary to much of the literature on reserve currency status, it does not appear that dominance, once lost, is gone forever.”

Indeed, it looks like the interwar years were characterized by a heated competition among major global currencies, with both sterling and the dollar near the top at various times. Eichengreen and Flandreau continue:

Our findings challenge the very notion that there necessarily exists a dominant reserve currency. They throw into question the idea that network effects and external scale economies leave room for only one significant international currency. A reasonable reading of the evidence is that sterling and the dollar shared reserve-currency status in the interwar period. Both New York and London were liquid financial markets. Neither the U.S. nor the UK had significant capital controls. Both were attractive places to hold reserves. As a group, central banks split their reserves between them, not wishing to put all their eggs in one basket.

What had been an “oligopoly” of global currencies dominated by sterling, the mark, the French franc was replaced after the war by a contest between the dollar and sterling. This could have gone on indefinitely had not the Second World War dealt another heavy blow to sterling. The war would prove to be even more devastating than the Great War for Britain in terms of human lives, infrastructure, finances, and fiscal stability. The coming ascendance of the dollar was so obvious by 1944 that Europe embraced the Bretton Woods system, which placed the dollar at the center of a new gold-exchange standard in which only the dollar was linked to gold.

Sterling was further wounded by mounting public debt and inflation in Britain. In 1949, the British state deliberately devalued sterling against the dollar—and therefore also against gold. Meanwhile, many of the world’s largest economies embraced capital controls. European regimes embraced even more intervention in the marketplace, increasing foreign exchange risk for those holding sterling or francs after the war. (The German, economy, of course, had been utterly destroyed in the war.) All of this further enhanced the dollar’s position. (Sterling was devalued a second time in 1967.) Meanwhile, American productive capacity continued to grow, further boosting international demand for dollars.

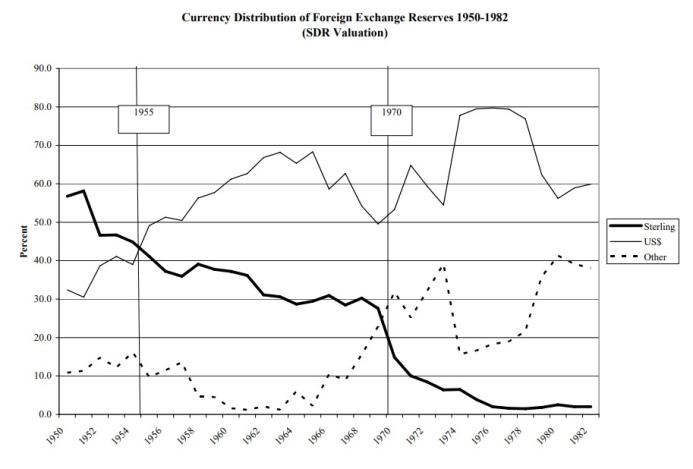

At this point, the dollar began an upward trend in global demand that would peak in the 1970s. The dollar reached levels of dominance rarely experienced by any currency. In 1955, sterling and the dollar were nearly equal in that both currencies made up about 45 percent of foreign reserves. Thirty years later, the dollar had surged to over 75 percent of all reserves and sterling had plummeted to under 10 percent.

Source: Catherine R. Schenk, “The Retirement of Sterling as a Reserve Currency after 1945: Lessons for the US Dollar?,” World Financial Review, May–June 2011.

Even after the US abandoned the remnants of the gold standard in 1971—thus ending the Bretton Woods system—no currency rivaled the dollar. This was partly due to the fact that even the end of Bretton Woods could not erase the fact that the dollar continued to be the most accessible and reliable currency in market terms. After the Second World War, Eichengreen and Flandreau note, “American economic and financial dominance was overwhelming, New York was the only truly deep and liquid financial market, and the U.S. was [the] only country to shun capital controls—and . . . the dollar, therefore, dominated the reserve holdings of central banks.”

Lessons from Sterling's Fall

In many ways, the decline of sterling as a global currency resulted from self-inflicted wounds. The British state chose to needlessly enter the First World War, incurring enormous war debts. It then attempted to apply wartime central planning to the domestic economy permanently, further hampering economic growth. Even worse, British participation in the First World War helped pave the way for an aggressive German state in the 1930s. The Second World War essentially bankrupted the United Kingdom, and the resulting inflation made the decline of sterling inevitable. Throughout most of the twentieth century, sterling inflation outpaced dollar inflation. Repeated devaluations sealed sterling’s fate. The dollar thus inherited a position that had been to a large extent unilaterally abandoned by sterling.

It remains to be seen how long the dollar will retain this position. So far, however, there are few signs of an imminent collapse on a level that would rival what happened to sterling after the Second World War.

Yes, the dollar has certainly retreated from its unparalleled highs in the mid-1970s, when it made up nearly 80 percent of global reserves. Yet the dollar is still clearly the most favored currency, with a role in the global economy well exceeding that of its closest rival, the euro. More than 55 percent of global reserves are in dollars, and only around 20 percent are in euros.

As British policy makers doomed sterling with their own policy choices, American policy makers can still do the same. Eichengreen warns:

Whether the dollar retains its reserve currency role depends, first and foremost, on America’s own policies. Serious economic mismanagement would lead to the substitution of other reserve currencies for the dollar. In this context, serious mismanagement means policies that allow unsustainably large current account deficits to persist, lead to the accumulation of large external debts, and result in a high rate of U.S. inflation and dollar depreciation.

However, recent experience suggests that “serious economic mismanagement” is here to stay. Were US policy makers to rein in deficits and allow interest rates to rise, all while keeping price inflation below that experienced in Japan and Europe, we could say the dollar faces no likely rivals. Yet it is extremely unlikely such reforms will actually happen.

This heightens the odds that the dollar will again face competition from other currencies as investors, central banks, and savers seek to avoid keeping all their eggs in the increasingly risky dollar basket.

Unlike the situation that existed after the First World War, however, there is no other economy or currency that stands ready to truly replace today’s favored currency. A more likely outcome is currency diversification such as existed in the interwar period, when dollars and sterling became essentially peer currencies and francs served a significant but supporting role.

The degree to which other currencies may look attractive compared to the dollar is up to American policy makers themselves. As Daniel Lacalle recently noted, no currency is poised to easily replace the dollar. But American policy makers could still cause the dollar to self-destruct by embracing even more reckless debt, spending, and monetary inflation.

Full story here Are you the author?Tags: Featured,newsletter