Between 2019 and 2022, the fortune of India’s Gautam Adani swelled from $9 billion to $127 billion. As the value of his seven publicly traded companies—providers of everything from natural gas to digital services—soared, he was briefly the world’s second-richest person. His meteoric rise caught the attention of Hindenburg Research, a small US investment firm devoted to profiting by exposing corporate malfeasance.

Viewing with suspicion the several-hundred-percent year-on-year gains of many of Adani’s companies, Hindenburg Research secretly began a two-year investigation into his sprawling corporate empire. Last week, they published their findings: Adani and his associates, many of them close family, have been engaged in a series of massive frauds.

The report, which runs over a hundred pages and includes several hundred sources, alleges numerous offenses, from accounting fraud to stock price manipulation, corruption, and intimidation. Hindenburg details first-hand accounts describing a network of Mauritius-based shell companies whose purpose is to move money covertly between Adani’s corporate entities, thereby making each firm’s financials look much better than they are, and they accuse Indian regulators of purposefully looking the other way while Adani and his cronies enrich themselves in this and other ways.

When the news surfaced, Adani quickly issued a blanket denial and threatened legal action. Markets weren’t reassured, however. Since Hindenburg’s report was published, Adani Group has shed 25 percent of its value, and Adani’s combined losses on the week amount to nearly $48 billion.

Investors are likely right to take heed. After all, though Hindenburg is only a few years old, its track record is fast becoming the stuff of legend.

Hindenburg exposed electric vehicle maker Nikola as a fraud, ultimately landing its founder, Trevor Milton, in jail—and this after the C-suiters at GM had agreed to take a huge partnership stake in the small firm. Hindenburg also blew the whistle on another electric vehicle maker, Lordstown, resulting in a massive overhaul of the company’s leadership and a lawsuit by shareholders.

| In both cases, Hindenburg’s research team took its suspicions about Nikola’s technology and Lordstown’s reservation numbers and launched intensive investigations, interviewing former employees and investigating on site. Discovering numerous falsehoods, Hindenburg took large short positions in each company before releasing its reports, netting a bundle as the prices of both Nikola and Lordstown plummeted.

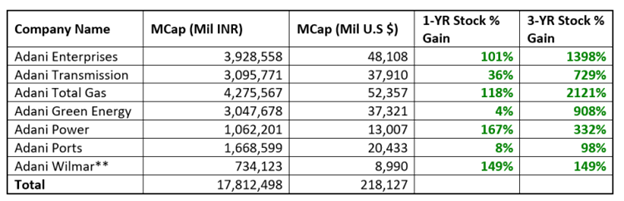

In the case of Adani’s empire, other than the eye-popping, several hundred–fold price increases (pictured below), Hindenburg spotted several immediate red flags. Among them was that the company couldn’t keep anyone in the chief financial officer position (with five in as many years). Also, the only independent audit outfit Adani Group listed on its payroll was a shadowy offshore entity with only a few apparent employees—this to oversee several hundred entities and their thousands of individual transactions. After tracking down former employees, scoring interviews with several former senior executives, and pulling public corporate records, researchers at Hindenburg concluded that, all criminal conduct aside, Adani’s combined ventures are likely 85 percent overvalued given their actual debt-to-capital ratios. |

Figure 1: Stock gains for Adani Group entities |

To confirm whether or not these businesses are so overvalued would require a true accounting of each firm.

This may be forthcoming.

With markets having failed to be calmed by Adani’s initial statements, or by the four-hundred-page defense Adani’s team published over the weekend (which answered almost none of Hindenburg’s eighty-eight concluding questions), the Economic Times reported early January 31 that Adani’s companies would engage one of the “big four” internationally recognized accounting firms to come in and do an independent audit.

Whether Adani follows through once his company’s secondary issue is concluded, something he says must happen first, will remain to be seen.

As things stand at the time of writing, with just days to go before the secondary offering closes, just 3 percent of the subscription has been filled.

Like with FTX, the predictable calls for more and new regulations are sure to come as this story unfolds. It is worth pointing out that apart from distorting markets, regulators, for all the powers they are given, are often asleep, captured, or otherwise ineffective. And even the higher accounting standards since the Sarbanes-Oxley Act haven’t eliminated corporate fraud.

Activist short sellers like Hindenburg represent the cutting edge of an alternate means of market regulation. Any distortions caused by a single firm could be quickly corrected, even in the event that an investigating firm released inaccurate information, tremendously improving markets’ efficiency. That a profit-seeking firm does a better job patrolling the market and informing investors of fraud than comfily protected bureaucrats should come as no surprise.

And as always, the rule of the market should always be the old caveat emptor, buyer beware!

Full story here Are you the author?

Tags: Featured,newsletter