Joseph Y. Calhoun

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

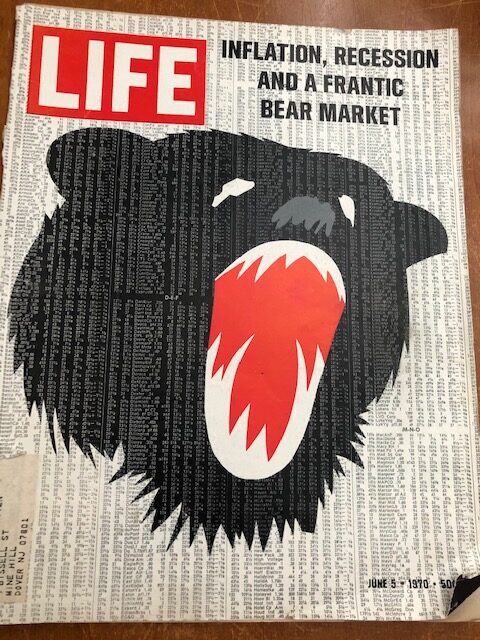

I stopped in a local antique shop over the weekend. The owner is retiring and trying to clear out as much as she can before they close the doors so I paid a mere $3 for the Life magazine above. I think it might be worth many multiples of that price for investors who think our situation today is somehow uniquely bad. The cover headline could just as easily be describing today as 1970.

The year 1970 was a tough one for America. Inflation averaged around 6% that year, although it had already peaked by the time of this Life issue. The stock market had peaked in December of 1968 and was already down 15% by the start of 1970. It would go on to lose a total of 34.9% by the time it made its low on May 26th, just before this issue was published.

We had political turmoil at home with 4 college kids killed at Kent State and we also heard the verdict for the Chicago 7 in February, where Jerry Rubin, Tom Hayden and Abby Hoffman were all acquitted of conspiracy but convicted of inciting a riot (all of which were overturned on appeal). Back in ’67 Hoffman had led the so called Yippies on Wall Street protest, throwing dollar bills from the balcony of the NYSE to protest capitalist greed. Occupy Wall Street wasn’t new.

We had geo-political intrigue abroad as Nixon widened the Vietnam war to Cambodia. And we had financial problems as well with the bankruptcy of Penn Central in the same month as this Life cover. Penn Central was the 6th largest company in the country and its bankruptcy was the biggest in American history to that time.

Unemployment rose throughout the year, starting at 3.5% and ending at 6.1%. Jobless claims rose from 202k in December of 1969 to 374k in April of ’70. The Fed funds rate peaked at 9.5% in late ’69 and the Fed was cutting rates for the entire year, proving once again that the Fed has no ability to stop a bear market with rate cuts. GDP growth was positive for the year but that hardly tells the story. GDP fell at a nearly 2% annualized rate in Q4 ’69, fell further in Q1 (-0.6%), rose in Q2 (+0.6%) and rebounded big in Q3 (+3.7%). Q4 was a disaster at -4.3%.

Short term Treasury rates peaked early in the year with the 1 year Treasury yield topping at 8.4% right at the end of ’69. Long term rates were more stubborn with the 10 year topping out the same day the stock market bottomed on May 26th. The peak 10 year rate that year was 8.2%. The yield curve (10 year/Fed Funds) inverted in August of the previous year at a max inversion of -3.9%. Yes, you read that right. Modern pundits fretting about an inversion of 40 basis points have no sense of history.

The S&P 500 bottomed that year on May 26th at 71.17 and rose by 30% through year end to 92.79 despite that awful Q4 GDP reading. Most of those gains came between August and year end. It would rally further to a peak in early 1973 at 121.74, a move of over 71% from trough to peak.

What do we learn from this history lesson? Well, most obvious is that our current situation isn’t unique at all. Markets have dealt with high inflation and an aggressive Fed before. It also highlights how hard it is sometimes to figure out where the economy is in real time. The 1969/70 recession wasn’t called a recession by the NBER until early 1971, after the recession had already ended. There was a lot of discussion at the time about whether it even was a recession. Sound familiar?

Another lesson is that stocks, like all markets, anticipate. The market bottomed in May when interest rates peaked even with the most negative quarter of the recession still ahead. And stocks don’t have to get “cheap” before finding a bottom. The S&P traded around 17 times earnings that year, down from around 22 before the bear market started.

We think today of meme stocks as something unique but the 60s were called the go-go 60s for a reason. The Nifty Fifty, the glamour stocks, the concept stocks, the conglomerates and the “gunslinger” fund managers who touted them were rock stars. George Tsai was the Cathie Wood of the day. When the Nifty Fifty finally expired in the early 70s, they had P/Es that rival anything seen today with Xerox at 49 times, Avon at 65 and Polaroid at 90.

2022 will not be a replica of 1970 because there are differences between the two periods, mainly that the conditions back then were, if anything, worse than today. But there are some things that don’t change. It isn’t coincidence that the rally off the June lows this year started when interest rates peaked just as it did in 1970. Interest rates are important for their role in how we value stocks but why they move up and down is less important than the fact that they do.

There is truly nothing new under the sun or in markets. There are no new eras if you know history. Markets have been here before even if today’s participants haven’t. And that is always true too; there were traders in 1970 who had never been through a bad bear market. The last bear market in 1966 only lasted 8 months and stocks fell just 22%, barely even qualifying for the bear label. The last bear market with a drawdown more than 30% had been way back in 1942.

This bear market, like all others before it, will come to an end. It may be soon or it may have more to run but markets and investors have survived much worse conditions than what we face today.

Economy

The economic data released last week continued to show a modest improvement in the economy since July. The Dallas Fed Manufacturing survey improved in August although it was still slightly negative. Home price appreciation moderated, the Case-Shiller index up 0.4% from May and 18.6% yoy. I can’t imagine that the rate of change hasn’t continued to moderate since then.

JOLTS was much better than expected with job openings steady above 11 million although the quits rate was down a little. Conference Board consumer confidence improved much more than expected to 103.2 from 95.3 in July. Present situation and expectations readings were also up strongly. Purchasing intentions increased while vacation intentions reached an 8 month high.

Jobless claims fell for the 3rd week in a row. The peak in July was 261 and we’re back down to 232 now.

The ISM manufacturing survey improved in just about every way possible (see my comments here).

The employment report was about as expected with a solid rise in employment, a rise in the participation rate, an increase in the labor force which pushed up the unemployment rate slightly and average hourly earnings that grew less than expected.

The only real negative report for the week was Factory orders which fell 1% but that was a July reading. We’ll see in the next report whether it improved like most everything else in August.

Overall, the economy does not appear to be in recession or on the verge of it.

EnvironmentI’ve said it repeatedly, but one more time. The trend on rates and the dollar are both up and that has been true now for months. The dollar made its final low in the summer of last year and while there have been some pullbacks along the way, the trend is up and obvious. The 10 year Treasury yield has been rising since the summer of 2020 although there was a pullback in rates that lasted from April to August of last year. Rates moved up strongly at the beginning of this year but have been stalled since early May. Are we near a top in rates? Maybe. Upside momentum actually peaked with the May peak in rates; the rise into the June high was not confirmed by momentum readings. |

. |

| In our tactical framework we classify the environment based on economic growth and the dollar. In these weekly commentaries I generally refer to interest rates and the dollar. I do that because it takes the emotion out of classifying the economy as growth rising or growth falling. The nominal 10 year Treasury note yield is highly correlated with nominal growth and so when it is rising it means nominal growth expectations are improving, i.e. growth rising.

Of course, nominal growth isn’t the whole story. To get to real growth expectations we also have to look at real rates and inflation expectations. Today, real rates are also rising and because they are rising faster than nominal rates, inflation expectations are falling. Combined with the rise in nominal rates, it is hard to see how that could be classified as anything but a rising growth environment. But that isn’t the only way we can look at growth expectations, the yield curve provides information too. Unfortunately, that reading points to falling growth although the curve has been steepening some – in a good way – lately. I get asked all the time, “what quadrant are we in” and my answer is that it is rarely clear cut and today is no exception. In a rising growth, rising dollar environment the investments that tend to work well, such as growth stocks, are not. If you insist we are in a falling growth, rising dollar environment, some of the investments that tend to do well in that environment, such as long term bonds, also aren’t doing so great. The investing matrix we use is based on history but it only identifies tendencies. The fact that none of the quadrants exactly matches current markets should not be surprising since we are in a unique and rare situation – recovering from a pandemic. We do expect that when the COVID distortions are finally over, whenever that is, we will see historical tendencies return. In the interim, we think investors need to remain very flexible and open-minded. |

. |

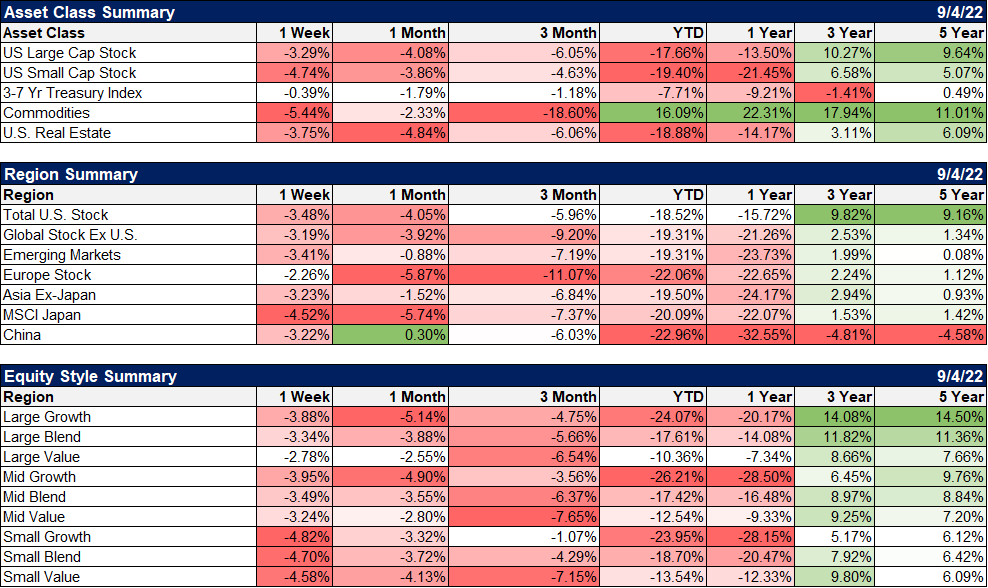

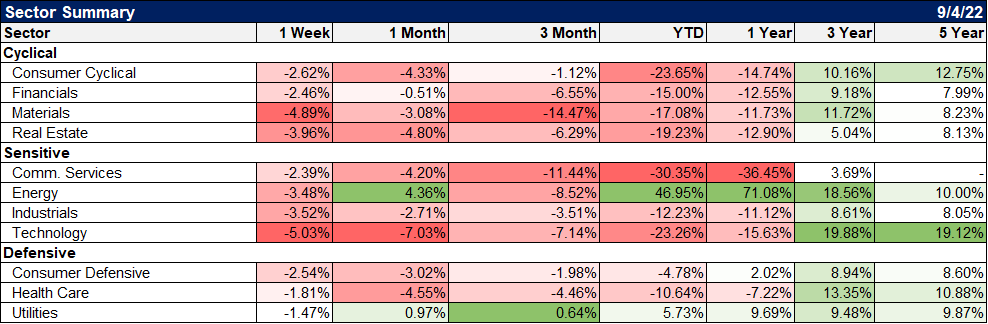

MarketsIt was another week of nowhere to hide. It looked like stocks might end the week on a positive note but the news late Friday that Russia would not re-open the natural gas pipeline to Europe killed the rally. Or at least that’s what all the news said; I don’t personally know why sellers suddenly emerged Friday afternoon. Oil moved back near its recent lows but the selloff in commodities was broad with copper actually leading the way, down over 7%. And no, I don’t put any stock in that Dr. Copper nonsense. The drop in commodities is about rising real rates not any signal about future growth. If you doubt that, go back and take a look at the late 90s. Copper peaked in early 1995 at around $1.40 and fell all the way to $0.61 in 1999. Maybe Dr. Copper was still working on his degree back then. Value outperformed last week and is well ahead on a YTD and YOY basis as well. |

. |

| Best performing sectors last week were defensive with utilities and healthcare leading the way. |

. |

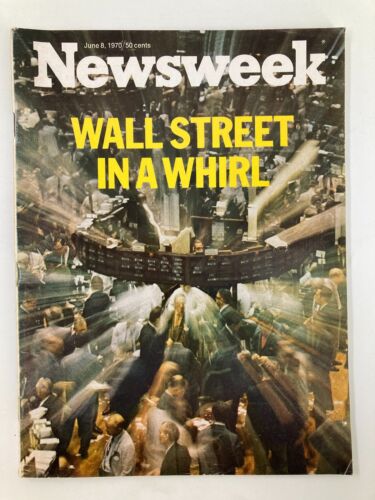

| History may not repeat but markets are made up of people and they do. Investors do the same things over and over, only the details differ. The magazine cover indicator has worked for a long time but it works best with general interest publications like Life and Newsweek (this is from the same week as the Life cover):

That is true because if a market or economic event ends up on the cover of a general interest magazine, it is already widely known and factored into current prices. We don’t have many magazines like that anymore (or many magazines for that matter) so the indicator is harder to use these days. There are other ways to discern market sentiment though and right now it is overwhelmingly negative, about the economy, about the stock market, about politics and about the global geo-political situation. Maybe things will get worse from here but if they do it would it really surprise anyone? More importantly, would it surprise markets? Know history and know yourself. |

. |

Full story here Are you the author?

Tags: Alhambra Portfolios,Alhambra Research,Bear Market,Bonds,commodities,Copper,currencies,economy,Featured,House Prices,inflation,Interest rates,Markets,newsletter,Real Estate,stocks,Unemployment,US dollar,valuations,value stocks