Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

|

The Dollar Index is a popular way to think about and trade “the dollar.” However, it has become less relevant as a reflection of the dollar’s performance or representative of trade, capital flows, market capitalization. Economists often use a trade-weighted basket, and the Federal Reserve’s real broad trade-weighted index is an input in official and private-sector forecasts.

|

|

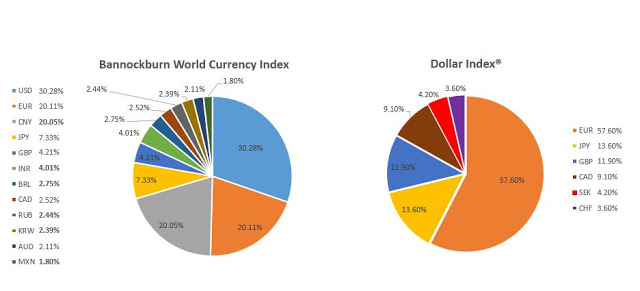

| As an alternative, we present Bannockburn’s World Currency Index (BWCI). It is weighted by the World Bank’s GDP estimate and includes the top dozen countries, with one notable exception, the eurozone counts as one entity. Half of the members of the BWCI are from developing countries, and the other half are from high-income countries.

Unlike other measures, it is truly a world currency basket and includes the US dollar. The dollar is currently about 30% of the world’s GDP and has a 30% share of BWCI. While the weighting may change over the years, the dollar is always worth a dollar, so the exchange rate is constant. The Chinese yuan is not in the Dollar Index, and its share in the IMF’s Special Drawing Right (SDR) is not quite 11%. However, its share of world GDP is a little more than a fifth, and it will likely surpass the eurozone this year. It has a little more than a 20% weighting in the BWCI. Based on GDP, the Bannockburn World Currency Index represents about 80% of the world’s GDP and equity market capitalization. The currencies included account for a little more than 85% of the turnover in the foreign exchange market and almost 95% of the global bond market. The other innovation of the BWCI is that it is a basket of one-month forwards, using Bloomberg forward indices. From the forward rates, we can interpolate a new one-month benchmark rate that reflects the funding cost of buying the GDP-weighted basket. For the US dollar’s component, we used LIBOR but are prepared to adopt its replacement. |

Composition - Click to enlarge |

| Both the BWCI <INDEX> and the interest rate component (BWCII <INDEX>) can be found on Bloomberg with historical data. Unlike the Dollar Index, which has remained constant, but for replacing the legacy currencies by the euro, BWCI will be adjusted once a year by the World Bank’s calculations. The chart below shows how the composition has changed in recent years.

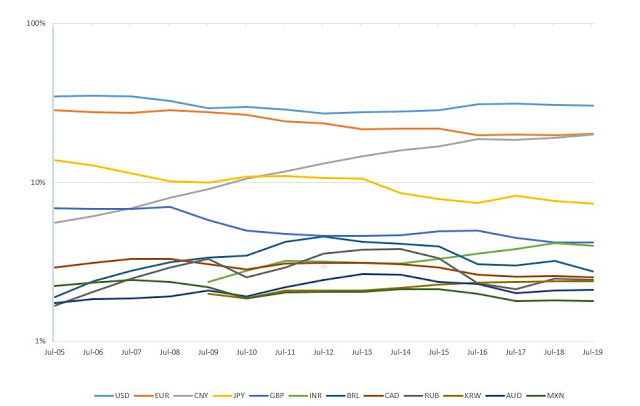

Traditionally, changes tend to be modest, even if rising steadily like China (gray line). India (green line) is also rising. The US share of world GDP has slipped only slightly over the past 15 years, the decline of Europe (EMU and UK) and Japan is more evident. This year and next year, the pandemic and policy response may create larger than usual shifts in the weightings. Of course, the GDP-weighted measure does not take into account other relevant economic conditions, like deficits and debt, or the disparity of income and wealth. Nevertheless, BWCI offers a global currency basket that is better reflective of the world in an intuitively straightforward way. It captures more of the world economic activity that the Dollar Index. It is dynamic the way other benchmarks, like the S&P 500 or Dow Jones Industrials. It is transparent, and the governing rules are simple. We officially launched the Bannockburn World Currency Index last week. Here is a link to that presentation (here), where I was joined by Suzanne Bishopric, who previously managed the UN pension fund and now advises central banks. As a practitioner, she sure her enthusiasm for an alternative to the Dollar Index and sees much in the BWCI that can be useful for international investors. A summary and several charts can be found here. |

Change in Composition, 2005-2020 - Click to enlarge |

Full story here Are you the author?

Tags: Featured,newsletter