Charles Hugh Smith

My articles My offerMy siteAbout meMy videosMy books

Follow on:TwitterFacebookYoutubeAmazon

Can $300 billion, or $600 billion, or even $1 trillion continue to prop up an increasingly risk-riddled, fragile $330 trillion global bubble in overvalued assets?

When is “Not-QE” QE? When Federal Reserve Chairperson Jerome Powell declares QE is not QE. We can constructively recall the story that Abraham Lincoln famously recounted in 1862: ‘If I should call a sheep’s tail a leg, how many legs would it have?’

‘No, only four; for my calling the tail a leg would not make it so.’

Calling QE not-QE doesn’t make it different than QE, but it does communicate the Fed’s panicky desire to mask its stupendous injection of financial cocaine into the financial system. The Fed’s level of panic is noteworthy, as is the absurd transparency of its laughable attempt to conceal its panic.

In the same fashion, the financial media is loudly declaring the current blowoff top in stocks is not a blowoff top.

The delicious irony here is these denials are reliable markers of blowoff tops: the louder the denials, the greater the odds that this is in fact the blowoff top that many pundits have been expecting for some time, but always in the future.

Garsh darn it, maybe the future has arrived. The financial media denied the Q4 1999 – Q1 2000 blowoff top was a blowoff top, and it repeated its denial of a blowoff top in housing in 2006-2007. The pundits of 1929 also denied the Q3 blowoff top in stocks was a blowoff top.

If you want a reliable signal that the blowoff top has peaked, listen to the screechy adamance of the deniers. The list of reasons why blowoff tops can’t be blowoff tops is practically endless: sentiment isn’t bullish enough, there’s a Wall of Worry for stocks to climb (overlooking the inconvenient reality that there is always a Wall of Worry), the consumer is still looking good, corporate earnings will rebound, the soft patch is behind us, the Internet will grow for decades to come, they’re not making any more land, capital flows favor higher asset prices, we owe it to ourselves (paging Paul Krugman–the Keynesian Cargo Cult is about to dance the humba-humba around the campfire and you’re needed…), debt doesn’t matter (it never matters until it does), price-earning ratios have plenty of room to move higher, and everyone’s favorite, don’t fight the all-powerful Fed (and we command you not to look behind the curtain while we worship false gods and wave dead chickens).

But nonetheless, blowoff tops in asset bubbles remain a feature of asset overvaluation, which by the way has once again reached historic extremes (GDP to equity valuation, etc.)

This introduces the other reliable indicator of blowoff tops: this time it’s different. It’s always different at blowoff tops, but not in the way that proponents of eternally rising asset valuations imagine.

Even geniuses misread blowoff tops. Popular culture has it that Isaac Newton made money in the South Sea Company bubble, sold for a handsome profit and then re-entered at a much higher price, losing a fortune when the blowoff top collapsed. Some historians have argued that this account is not accurate, but new research verifies that Newton did miscalculate and lose a fortune: Newton’s financial misadventures in the South Sea Bubble:

This paper presents extensive new evidence that while Newton was a successful investor before this event, the folk tale about his making large gains but then being drawn back into that mania and suffering large losses is almost certainly correct. It probably even understates the extent of his financial miscalculations.

Which brings us to the present blowoff top that is widely presented as not-a-blowoff-top because of XYZ, with XYZ boiling down to the omnipotence and omniscience of the Federal Reserve. The implicit belief currently holding sway (just as various implicit beliefs enabled the South Sea Bubble in 1720 and the bubbles in 1929, 2000 and 2008, to name but a few of a rogue’s gallery of blowoff tops) is the Fed has complete control of interest rates and the stock and bond markets, and the evidence for this belief is the Fed’s unparalleled success in inflating asset bubbles in stocks, bonds and real estate for a decade, a managerial feat now in its 11th year.

The possibilities that the Fed’s manipulation–oops, management–of markets might suffer from diminishing returns, or that markets might still be prone to nonlinear events generated by emergent properties of complex systems are dismissed as so unlikely that there’s no point in even discussing them.

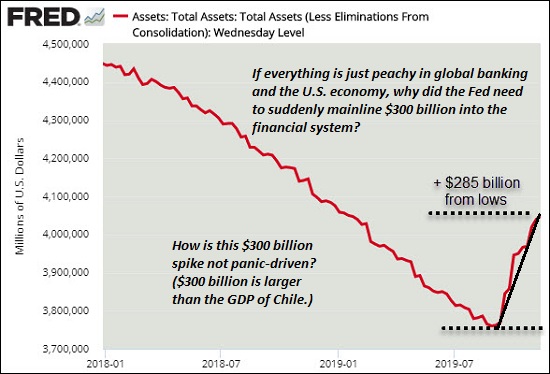

| All of which brings us to the Fed’s painfully obvious panic and pathetic attempt to conceal their panic, factors that are illustrated on this chart of the Fed balance sheet, which has suddenly exploded higher by $300 billion.

If everything’s just peachy in global banking and the U.S. economy, why the sudden mainlining of $300 billion of financial cocaine into the collapsing veins of the financial system? Just for context, that $300 billion is more than the entire GDP of Chile and a host of other nations. While the Fed’s $4 trillion balance sheet (up from a mere $800 billion prior to the Global Financial Meltdown in 2008) has jaded us to large numbers, $300 billion is still a monumental sum of “money” (i.e. currency created out of thin air by the Fed to distribute to banks, financiers, the super-wealthy and corporations.) We might want to recall here that the global asset bubble the Fed is attempting to keep inflating is several orders of magnitude larger: well north of $300 trillion in 2018. (It’s also worth recalling here that the Fed is not just the central bank of the USA, it’s also the central bank of last resort for the entire global economy. Much of the $23 trillion in loans, guarantees and backstops the Fed issued in 2008-2009 propped up non-U.S. banks and institutions.) Can $300 billion, or $600 billion, or even $1 trillion continue to prop up an increasingly risk-riddled, fragile $330 trillion global bubble in overvalued assets? Just as a matter of scale, the answer is “not likely.” The key variable here the belief of participants in the omnipotence and omniscience of the Fed. If the Fed can no longer keep the global bubbles inflating, then the bubble-sustaining belief that the Fed is in effect a new god will lose its self-predictive feedback loop: stocks go up because we believe the Fed will push them higher, so we buy stocks and our buying pushes stocks higher, doing the Fed’s work for it. Blowoff tops are rarely identified in the present. Even geniuses get fooled. But if we look at one simple indicator–the number of financial types denying this is a blowoff top and the number calling this the blowoff top of the entire 11-year Fed-induced frenzy of over-valuation– we have to conclude that the odds favor this being the blowoff top nobody expected until some far-off moment in the future. Well just maybe the future has arrived, but nobody noticed. |

Fed balance sheet 2018-2019 - Click to enlarge |

Full story here Are you the author?

Tags: newsletter