The shift to tighter monetary policies in the West is weakening credit markets. Over-indebted emerging markets face headwinds from rising borrowing costs and dollar shortages… Investors need to focus on their response to financial stresses in an era in which policymakers will be constrained.

The “everything bubble” is deflating. The fact that it’s happening relatively slowly shouldn’t blind us to the real threat: The world is dangerously underestimating how hard it’ll be to deal with the fallout once it pops.

Frothy markets can’t disguise the warning signs. The shift to tighter monetary policies in the West is putting pressure on global equity and real estate values. Even more critically, it’s weakening credit markets. Over-indebted emerging markets face headwinds from rising borrowing costs and dollar shortages.

At the same time, investors are underestimating how disruptive trade conflicts and sanctions could turn out to be. That’s not to mention rising non-financial risks — from the legal difficulties of the US administration, to the UK’s Brexit debacle, to political instability in France, Germany, Italy and even Saudi Arabia. Uncertainty will impact the real economy, primarily through the wealth effect of declining asset values and a reduced supply of credit.

Investors need to start focusing on how best to respond to a new crisis. The choices are more limited than many realize. Historically, central banks have needed to slash official rates as much as 4-5% in order to offset the effects of a financial crisis or an economic slowdown. That’s why former US Federal Reserve Chair Janet Yellen talked about the need to raise rates in good times — to provide room to cut when necessary.

Yet, even after recent US interest rate hikes, the Fed has nowhere near enough room to cut rates that much without going negative. In Europe and Japan, where rates are already less than zero, easing would require substantially negative levels, which would likely be politically impossible. Even current levels are controversial. Negative rates are a disguised way of writing down debt; they penalize savers and weaken the banking system.

Fiscal policy doesn’t offer much of an alternative. In most major economies, it’s already expansionary, albeit to differing degrees. The US government deficit is forecast to rise to $1 trillion as a result of tax cuts and higher public spending, according to the Congressional Budget Office. Most economies are pushing against high and rising government debt levels, as well as substantial unfunded liabilities for pensions and health care.

| Reversing the planned reduction of central bank balance sheets and restarting quantitative easing isn’t an option everywhere. The Fed can easily purchase government bonds given the increasing financing needs of the US government. But the European Central Bank is restricted by the capital key that governs the proportion of each EU member’s bonds that can be purchased. The Bank of Japan is already buying more than the government is issuing in new debt.In theory, central banks could aggressively expand the asset classes they buy to include corporate and bank debt, or real estate trusts and shares. The ECB, BOJ and the Swiss National Bank have already implemented such programs. But the ECB’s losses on bonds of troubled retailer Steinhoff International Holdings NV show how risky such a strategy can be.

Ultimately, central banks might have to resort to QE variations such as “helicopter money.” Originally a thought experiment of Milton Friedman, the government would print money and distribute it to the public to stimulate the economy. To make it palatable, the measure could be packaged as a way to rationalize welfare systems by reducing frictions and administration costs. |

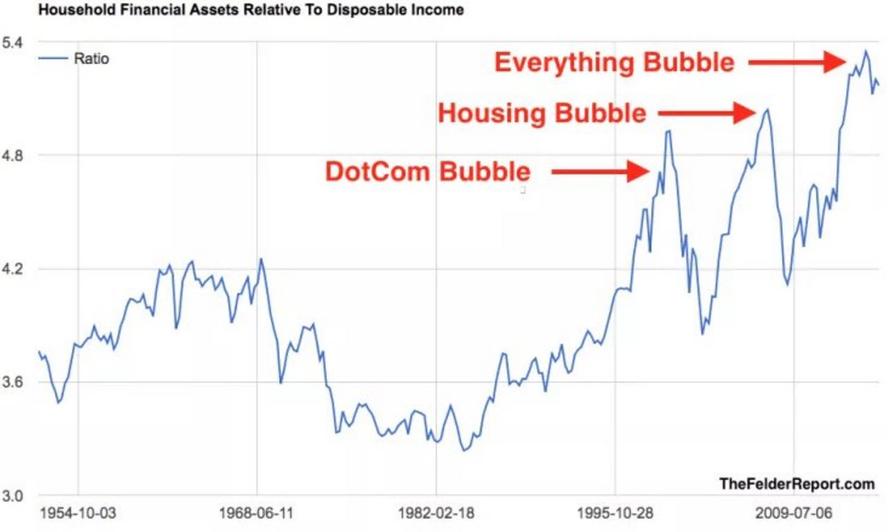

Household Financial Assets Relative to Disposable Income, Oct 1954 - 2018 - Click to enlarge |

Helicopter money would at least deflect criticism of QE programmes as favouring the wealthy and exacerbating inequality, as benefits would accrue to a wider spectrum of the population. Direct intervention, such as lending to or investing in businesses, or taking over banks and large parts of the economy to restart activity, are also possible.

Those would be awfully desperate measures, however, which points to the real problem. Since 2008, governments and central banks have stabilized the situation without fundamentally addressing high debt levels, weak banking systems and excessive financialization. Growth and inflation won’t recover until they’re dealt with. The surprise is that this comes as a surprise to policymakers, given that Japan’s experience since 1990 highlights the limits of available policy tools.

In any new crisis, then, policymakers are likely to be badly exposed. Central bank purchases of real estate and equities, helicopter money and more direct intervention could well fail to boost economic activity. That would contribute to a collapse in confidence in authorities, as the sight of governments forced to print money and throw it out of the window or take over markets increases people’s anxiety about the future.

There is already a crisis of trust – a democracy deficit – in many advanced economies, accompanied by rising political tensions. A loss of faith in the supposed technocratic abilities of policymakers to manage economies will compound these pressures.

The political economy could then accelerate towards the critical point identified by John Maynard Keynes in 1933, where “we must expect the progressive breakdown of the existing structure of contract and instruments of indebtedness, accompanied by the utter discredit of orthodox leadership in finance and government, with what ultimate outcome we cannot predict.”

Governments that want to avoid that dystopian prospect need to address the key underlying problems now, before it’s too late.

Full story here Are you the author?Tags: newsletter