Jeffrey P. Snider

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

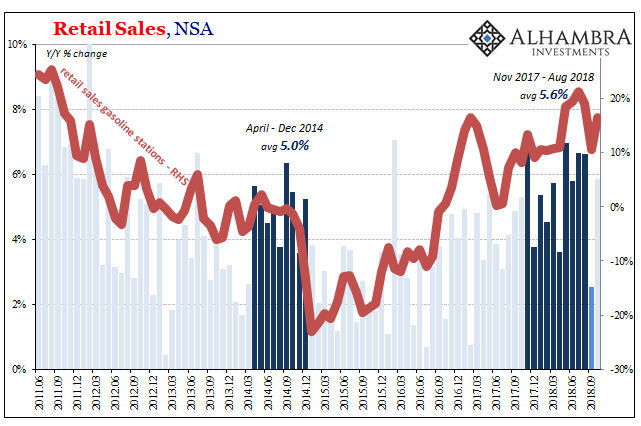

Retail sales rebounded 0.8% in October 2018 from September 2018, but it’s the downward revisions to the prior months that are cause for attention. The estimates for particularly September were moved sharply lower. Total retail sales two months ago had been figured last month at $485.8 billion (unadjusted) originally, but are now believed to have been just $483.0 billion. The difference takes the growth rate underneath 3% for the first time since February 2017.

| On a seasonally-adjusted basis, these revisions now suggest retail sales declined slightly in each of the prior two months before October. September storms are being blamed for weakness, but only Florence made US landfall during that month. In October, retail sales advanced despite disruption caused by Michael.

Gasoline sales in September weren’t as sharp compared to October. Total sales last month were up just 4.6% seasonally adjusted on a year-over-year basis, differing widely from the 5.9% increase unadjusted. A big part of either number was retail sales recorded by gasoline stations, those rising more than 16% (both) in October from the previous year. Removing gasoline sales, retail sales otherwise gained just 3.6% (seasonally adjusted) or 4.9% (unadjusted). |

U.S. Retail Sales, NSA 2011-2018(see more posts on U.S. Retail Sales, ) - Click to enlarge |

| Hurricanes, therefore, were not really the problem. The deceleration in consumer spending back toward recession-like levels began months before them. Starting in June, for five months retail sales have exhibited clear weakness despite, rather because the large increase in spending at filling stations. Americans are again paying more for gas leaving not much room for anything else.

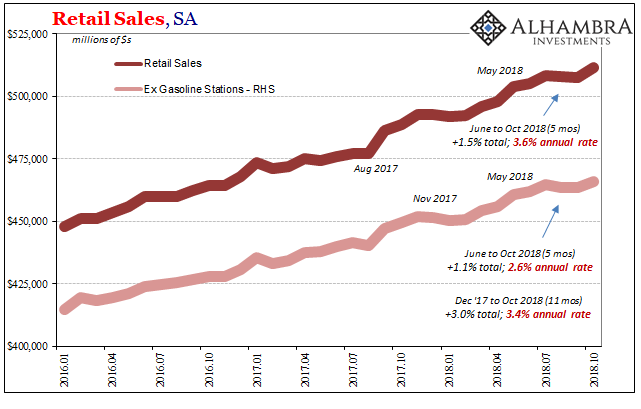

Including the contributions from gasoline, over the last five months (including revisions to August and more so September) total retail sales have increased by only 1.5%. That adds up to a very low 3.6% annual rate. A five-month lull reduces the chance this slowdown is the product of very short-term events like hurricanes. Taking out gasoline stations, retail sales are up just 1.1% meaning a 2.6% annual rate. Going back to last December, excluding gas retail sales are rising at a 3.4% annual rate. These are very bad indications. If oil prices continue to decline, after a lag total retail sales will converge in growth rates with those not counting gasoline. |

U.S. Retail Sales, SA 2016-2018(see more posts on U.S. Retail Sales, ) - Click to enlarge |

| A healthy economy, an actual boom, would produce retail sales growth between 6% and 9% consistently. Following a downturn like 2015-16, there should have been more than a couple months in double digits, with the worst during that time an infrequent month in the 6s.

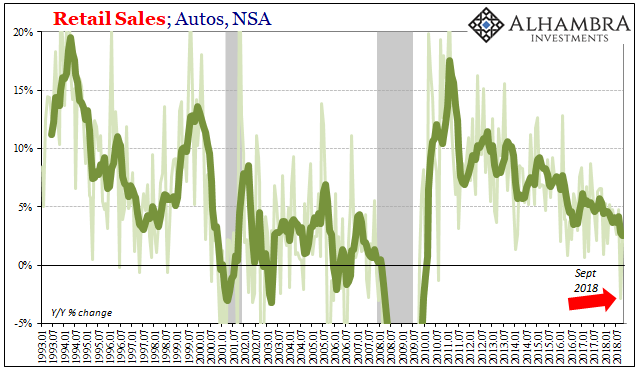

Instead, consumers are still going at sub-4% rates again. One of the major drags in revisions as well as original estimates was auto sales in September. In October, retail sales in this segment “rebounded” by rising just 2.2% (unadjusted) year-over-year. The revised estimates for September 2018 now show a decline of nearly 3% from the same month in 2017. It was the first contraction in auto sales since 2010, and by far the worst since the Great “Recession.” Undoubtedly, Hurricane Michael and perhaps Florence played some role in the softness, but even factoring the weather that’s an alarming result indicating like recent housing weakness there is a lurking downside in consumer spending (starting with gasoline eating up discretionary spending and then caution about purchasing big ticket items). |

U.S. Retail Sales, Autos, NSA 1993-2018(see more posts on U.S. Retail Sales, ) - Click to enlarge |

| If you talk to auto dealers, they’ll all tell you that the disappearance of 0% financing is to blame for renewed problems. Auto sales had peaked more than three years ago anyway, especially in terms of volume, but even if this is true about interest rates it again shows the forecast errors being made.

In other words, this isn’t how “stimulus” is supposed to play out. Low and even zero interest rates are intended to stir up spending by making it cheaper to finance goods, cars and trucks in particular. That increased economic activity was then expected to lead to more spending and jobs, kicking off the virtuous circle Keynes once described (pump priming). By the time you remove such interest rate “stimulus”, the economy is in high gear so that wage gains and robust employment totally offset and overcome the higher interest costs that then associate with financing. The boom that results can’t be just one in name only. The mere act of removing zero interest rates is not supposed to disrupt anything. If it does, it didn’t actually stimulate anything but perhaps the one economic segment most exposed to it. And that’s only the mainstream explanation for potential current and upcoming weakness. In specifically autos, as housing, there has been lurking softness for years already. It may be that higher priced gasoline (in comparison to the past few years, low prices consumers have normalized to) has tipped the balance further negative in combination with the lack of income and wage growth. |

US Retail Sales Stagnation 1992-2018(see more posts on U.S. Retail Sales, ) - Click to enlarge |

Either way, as retail sales in 2018 have shown, there is no economic boom despite tax cuts, the unemployment rate, and repeated emphasis upon it (trying to play up expectations). As has been the case all along the last eleven years, Americans aren’t spending more simply because they can’t. The small-scale factors pale in comparison to this one fact.

This is before the global downturn begins to bite. The proliferation of negative numbers throughout the world suggests we should prepare for recession-like retail sales numbers month after month ahead. Except we already have them.

Perhaps it won’t be the US economy that will stop booming because of a looming global downturn, rather maybe it’s a global downturn because the US economy never boomed at all. Imagine the grave disappointment all around the world when economic agents realize the promises of globally synchronized growth amounted to little or nothing. I’d start cutting back, too, money to production to trade to economy.

Tags: currencies,economy,Federal Reserve/Monetary Policy,Markets,newsletter,U.S. Retail Sales