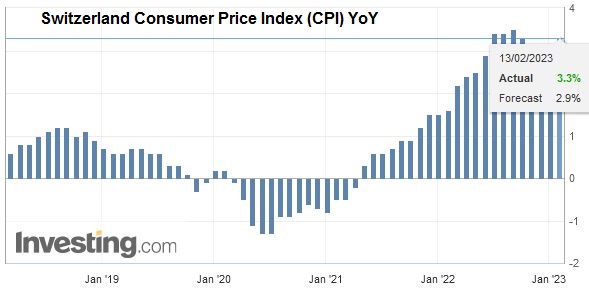

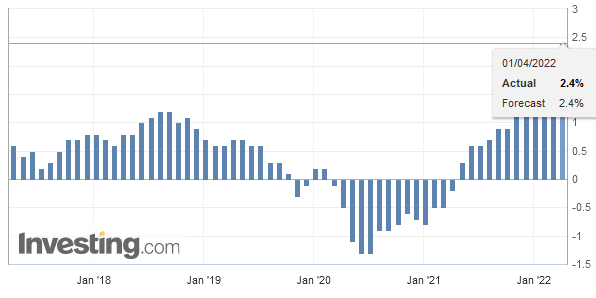

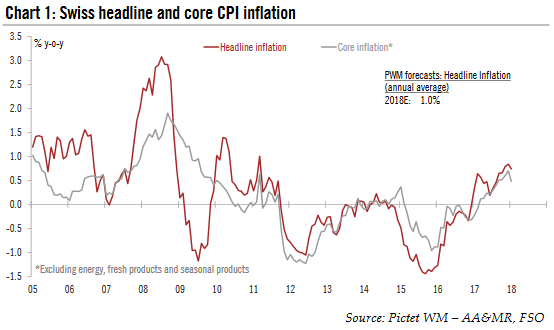

| According to the Swiss Federal Statistical Office (FSO), the headline consumer price index (CPI) inflation eased to 0.7% y-o-y in January from 0.8% y-o-y in December, in line with consensus and our own expectations. Core inflation (CPI excluding food, beverages, tobacco, seasonal products, energy and fuels) also eased, from 0.7 % y-o-y in December to 0.5% y-o-y in January (see Chart 1), back to the level of October 2017.

The FSO report showed that inflation for imported goods and services slowed down in January (to 2.0% y-o-y from 2.4% y-o-y in December) mainly due to the weaker franc and energy base effect. Meanwhile, inflation for domestic goods and services remained stable at 0.3% y-o-y in January. |

Swiss Headline and Core CPI Inflation, 2005 - 2018 - Click to enlarge |

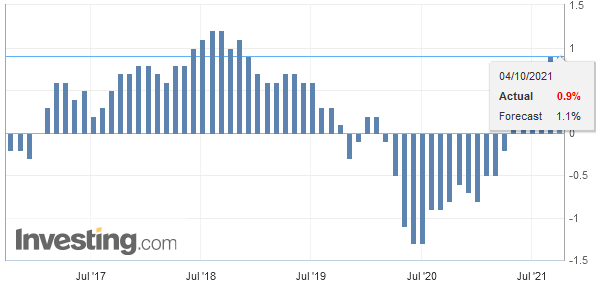

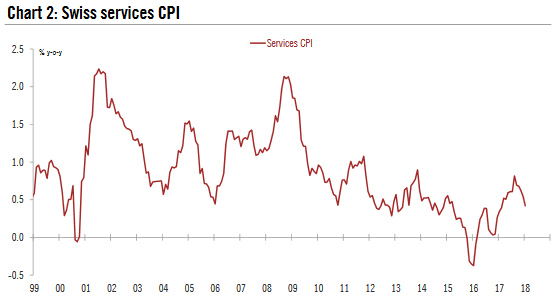

Keep an eye on services inflationCore inflation was rather disappointing. In particular, services inflation fell for a third successive month (by 0.1pp) to 0.4% y-o-y (see Chart 2), down from a peak of 0.8% y-o-y in August. The fall seems to have been exacerbated by special factors related to the health care sector, where prices for outpatient hospital medical services declined massively in January. By contrast, private services inflation remained broadly stable, at 0.7% y-o-y in January, for the third month in a row. Services inflation will be worth to following in the months ahead, as the trend of rising prices for services that emerged last summer seems to have broken down. |

Swiss Services CPI, 1999 - 2018 - Click to enlarge |

Swiss inflation outlook unchanged

Following FSO report, our inflation outlook remains unchanged. We expect headline inflation to firm up gradually as 2018 progresses, averaging 1.0% in 2018, but with risks tilted to the downside. The Swiss National Bank (SNB) is likely to keep a close eye on services inflation developments. Given the outlook for inflation is still contained, the SNB is likely to remain cautious and true to its current ‘two-pillar’ strategy (negative interest rates and a commitment to intervene in the FX market if needed). Our best guess is that there will be a first rate hike of 25bp in December 2018 (assuming that the European Central Bank (ECB) will have signalled the end of its asset – purchase programme by then). This would still leave the SNB’s policy rate below the ECB’s current deposit rate of – 0.40%. A second hike is then projected for Q3 2019, when we also expect the ECB to raise policy rates for the first time.

Full story here Are you the author?Tags: Macroview,newslettersent,Swiss headline inflation,Switzerland Consumer Price Index