Stocks MarketEM FX closed last week on a firm note, as the stronger than expected US jobs gain was mitigated by lower than expected average hourly earnings. Still, we believe that global liquidity conditions will continue to move against EM, as the Fed continues tightening and others join in. This week, BOC may be the first of the others to hike rates. Meanwhile, EM inflation readings this week are expected to remain low, underscoring that EM monetary policy is unlikely to be tightened anytime soon. That should lead to narrower interest rate differentials between DM and EM, which in turn should keep downward pressure on EM FX. |

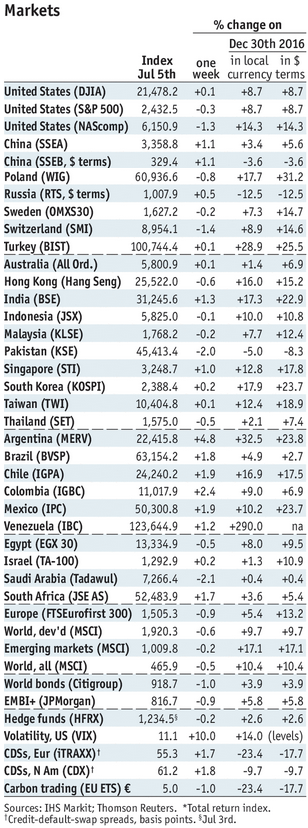

Stock Markets Emerging Markets, July 05 Source: economist.com - Click to enlarge |

ChinaChina reports June CPI and PPI Monday. The former is expected to rise 1.6% y/y and the latter by 5.5% y/y. New loan and money supply data will be reported during the week, but no data has been set. June trade will be reported Thursday, with exports expected to rise 9.0% y/y and imports by 14.0% y/y. TurkeyTurkey reports May IP Monday, which is expected to rise 5.0% y/y vs. 6.7% in April. It then reports May current account data Thursday, with the deficit expected at -$5 bln. If so, the 12-month total would widen to -$35.1 bln, the largest since October 2015. The external accounts are worsening just as global liquidity is tightening, which should put downward pressure on the lira. IsraelBank of Israel meets Monday and is expected to keep rates steady at 0.10%. Israel then reports June CPI Friday, which is expected to rise 0.3% y/y vs. 0.8% in May. If so, that would be the lowest rate since January and further below the 1-3% target range. For now, the preferred policy lever is a weaker shekel. HungaryHungary reports June CPI Tuesday, which is expected to rise 1.9% y/y vs. 2.1% in May. If so, that would be the lowest rate since December and back below the 2-4% target range. No wonder the central bank was comfortable easing again at its June meeting. Next policy meeting is July 18, no changes expected then. South AfricaSouth Africa reports May manufacturing production Tuesday, which is expected to contract -3.3% y/y vs. -4.1% in April. The economy remains very weak, but inflation has not fallen enough to warrant rate cuts in Q3. Rather, we see the first cut likely in Q4. Next SARB meeting is July 20, no change expected then. MexicoMexico reports June ANTAD retail sales Tuesday. It then reports May IP Wednesday, which is expected to rise 0.3% y/y vs. -4.4% in April. The real economy remains sluggish, while price pressures appear to be topping out. Whilst an easing cycle seems warranted, some central bank officials believe that it must keep pace with Fed hikes so that the interest rate differential is maintained. Next policy meeting is August 10, no change is expected then. MalayasiaMalaysia reports May IP Wednesday, which is expected to rise 4.4% y/y vs. 4.2% in April. Bank Negara then meets Thursday and is expected to keep rates steady at 3.0%. Inflation eased to 3.9% y/y in May, the lowest since January. While the central bank does not have an explicit inflation target, falling price pressures should allow it to remain on hold in H2 2017. SingaporeSingapore reports May retail sales Wednesday, which are expected to rise 2.0% y/y vs. 2.6% in April. It then reports advance Q2 GDP Thursday, which is expected to grow 2.8% y/y vs. 2.7% in Q1. With the economy sluggish, the MAS may not signal April tightening at its October policy meeting. Czech RepublicCzech Republic reports June CPI Wednesday, which is expected to rise 2.3% y/y vs. 2.4% in May. This would still be above the 2% target, though within the 1-3% target range. The central bank has signaled that the first rate hike will likely be in Q3, though timing will depend in large part on how strong the koruna gets. Next policy meeting is August 3, no change is expected then. IndiaIndia reports June CPI and May IP Wednesday. It then reports June WPI Friday. Price pressures have been lower than expected in recent months, but we would downplay talk of rate cuts. If anything, the RBI tightening cycle is likely on hold for now but lower rates seems unlikely. Next RBI policy meeting is August 2, no change is expected then. BrazilBrazil reports May retail sales Wednesday, which are expected to rise 3.4% y/y vs. 1.9% in April. Overall, the real economy remains weak even as price pressures continue to fall. Lower than expected IPCA inflation of 3% y/y for June has markets looking for a 100 bp cut from COPOM when it meets July 26. KoreaBank of Korea meets Thursday and is expected to keep rates steady at 1.25%. CPI rose a lower than expected 1.9% y/y in June, just below the 2% target. With the economy still sluggish, we see no need for the BOK to tighten anytime soon. ChileChile central bank meets Thursday and is expected to keep rates steady at 2.5%. CPI rose a lower than expected 1.7% y/y in June, the lowest since October 2013 and below the 2-4% target range for the first time since then. If the recovery does not pick up, we believe the central bank may resume cutting rates in Q4. PeruPeru central bank meets Thursday and is expected to cut rates 25 bp to 3.75%. CPI rose a lower than expected 2.7% y/y in June, the lowest since September 2014 and below the 1-3% target range. With the recovery lagging, we believe the central bank will continue cutting rates in H2. ColombiaColombia reports May IP and retail sales Friday. The central bank will also release its minutes that day. At that meeting, the bank cut rates by 50 bp to 5.75%. Next policy meeting is July 27, and another 50 bp cut seems likely. Inflation was 4.0% y/y in June, the lowest since January 2015 and right at the top of the 2-4% target range. |

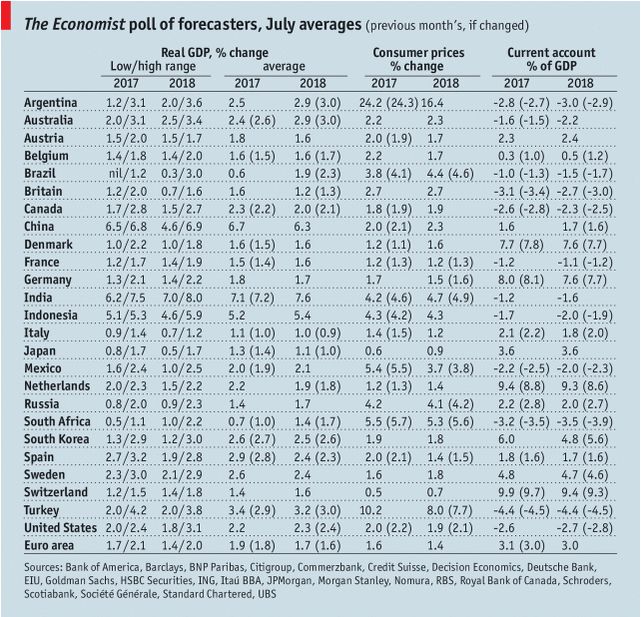

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, July 2017 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent