Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The US dollar remains firm against most of the major currencies to start what promises to be a critical week for investors. There are two main considerations. The first is the last minute position adjustments ahead the key events that begin with the IMF's SDR decision later today, running through the start-of the month data (especially PMIs), central bank meetings in Australia, Canada, and then the big one, the ECB. The US monthly jobs report and the OPEC meeting cap the weeks. The second consideration is month-end plays, where fund managers adjust positions and hedges.

There were two important developments over the weekend to note. The EU and Turkey struck a deal on the refugee problem. In essence in exchange for financial resources to help Turkey cope with the estimated 2.5 mln refugees and a vague promise to restart EU ascension talks, Turkey has agreed to grant Syrian refugees working visas and take back some refugees that already traveled to the EU. The 3 bln euros Turkey is to receive was referred to as an "initial" payment, suggesting it will receive more financial assistance over time.

The other development was the France made an important concession on the climate deal being negotiated in Paris. France agreed to allow the agreement to be downgraded from treaty-status. This is key because it will allow Obama to minimize Congressional approval. The Senate needs to ratify treaties. While the accord itself appears to be legally binding, the precise emissions reduction targets are not. The softening of France position may help Hollande secure concessions or a better atmosphere to press for concessions in its attempt to build a "coalition of the willing" post-October 31.

Today's news stream is fairly light so far. A few items stand out. Japan reported better than improvement in October industrial production and retail sales. Industrial output rose 1.4% in October after a 1.1% rise in September. The consensus called for a somewhat larger increase (1.8%). It has not strung two consecutive monthly increases since last December and January and snaps a two-month decline. It is the strongest reading since June. Japan also reported that retail sales in October jumped 1.1% compared with expectations for a 0.3% rise. It is the biggest rise since Julyand suggests some mitigating factors to last week's report that overall household spending had fallen sharply.

Sweden reported that growth in Q3 was twice what the market expected. The 0.8% quarterly expansion compares with the Bloomberg consensus of 0.4%. The estimate for Q2 GDP was shaved to 1.0% from 1.1%. The krona gained against the euro on the news and was also resisted the firmer US dollar tone. The important take away is that the deflation forces that have pushed the Riksbank down the unconventional monetary policy path is not leading to a downward spiral in economic activity. Sweden is showing us that deflation does not necessarily mean recession or contraction. Spain, which is among the fastest growth EMU members, also has had among the strongest deflation pressures.

Meanwhile, disinflation forces intensified in Italy. The harmonized measure of CPI fell 0.5% in November, more than twice the decline the consensus forecast and the largest fall since July. The year-over-year rate of 0.1% is the lowest since the -0.1% print in April. Separately, German states also reported November consumer prices. That leaves the national figure that will be released shortly, set for a small rise to 0.3% year-over-year from 0.2%.

Lastly, we note that German unexpectedly reported a 0.4% decline in October retail sales. The consensus expected an increase of the same magnitude. Retail sales have contracted in two of the past three months and four of the past six months, with only one month increase (1.7% in July, with September being flat).

The focus is squarely on the ECB's meeting this week. Surveys suggest nearly everyone expects at least a 10 bp cut in the -20 bp deposit rate and about 80% expect an extension of the purchase program (to March 2017). About 2/3 expect an increase in the pace of purchases, but less than half expect the universe of assets that can be bought to increase.

US economic data due out today pales in comparison to the employment report. The Chicago PMI is thought to be a more important regional report that the Milwaukee ISM and Dallas Fed surveys. The Chicago PMI is expected to ease to 54.0 from 56.2. This is a little pay back after the surge in October form 48.7 in September. The 3-month moving average in Q3 52.6. October pending home sales are expected to have risen 1.0% in October, snapping a two-month decline.

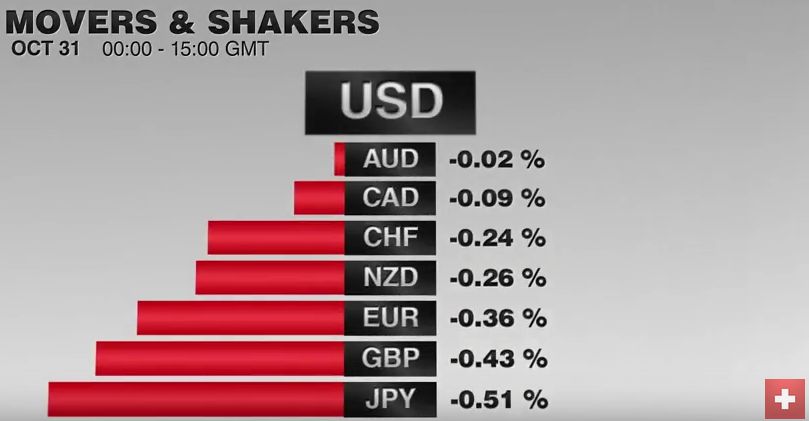

In terms of the price action, it seems unreasonable to expect much of a euro bounce. Today is thus far the first session in that the euro has remained below $1.06. It did not even do this in March or April. It may not be sustained, but it illustrates the extent of the bearishness toward the single currency ahead of the ECB meeting. The dollar is at five-day highs against the yen, having poked up to nearly JPY123.15. That might be the high of the session. Support is seen in the JPY122.60-JPY122.80 area. Sterling edged as close to $1.50 as possible without going through it. Bloomberg has it trading as low at $1.5001, its lowest level since April. Resistance is seen around $1.5040-$1.5050. The dollar-bloc is faring somewhat better. The Antipodeans are firm, and the Canadian dollar is flat.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: U.S. Chicago PMI