It’s Swiss National Bank reserve figures Wednesday! That glorious day when we get to see how exactly the ingredients of the SNB’s cake have changed. Or to put it more literally, how have they been dealing with the masses of euro assets they are collecting.

Here’s the table in question. What it shows is that the SNB has cut its euro share of FX reserves to 48 per cent from 60 per cent in the second quarter of 2012 while the proportion of sterling and dollars being held increased.

Gasp? Well… yes.

The move is most significant when compared to the second quarter’s shift, when the share of euros being held in the SNB’s reserves surged to that 60 per cent figure from 51 per cent in the first quarter. That suggested the SNB was having a hard time getting rid of the euros it had acquired by defending its precious floor of SFr1.20 to the euro.

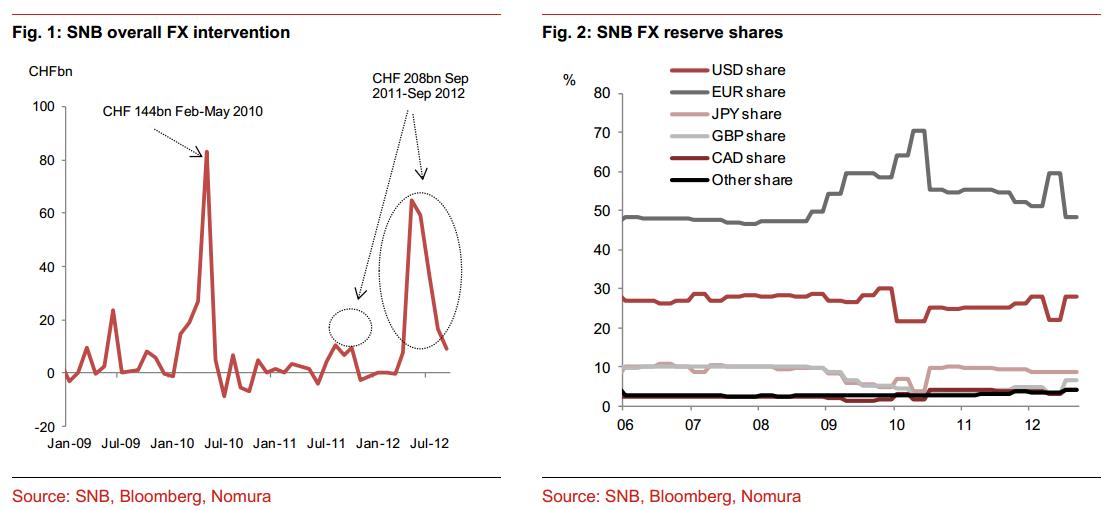

It’s also significant as it brings the euro reserves back to basically the same level they were at in 2008 — the share of 48 per cent is just 1 per cent higher than it was in the third quarter of 2008, as the chart from Nomura below on the right shows:

Reserves do tend to fall during periods of slower accumulation, which will naturally occur when the euro is doing ok, but this is still quite the reversal. However, it is tricky to read into the reserve moves precisely (and not just because of derivative muddiness).

For example, Citi’s Valentin Marinov said the following in advance of the data release on Wednesday (with our emphasis):

If the SNB reserves data suggests that the EUR-share remained close to 60%, this could corroborate the view that the central bank may be getting more comfortable with its exposure to the single currency. In addition, indications that the average duration of the reserves portfolio was lengthened again in Q3 could mean that the bank has increased its exposure to riskier longer-term EUR-denominated paper. More indications that SNB’s concerns about the outlook for the Eurozone are receding could in turn imply that the biggest obstacle for a higher SNB EURCHF floor– the fear of renewed bout of aggressive EURCHF selling – may now be diminishing. This could fuel market bets of a potential change in the currency peg ahead of the December SNB meeting and add to tailwinds for EURCHF.

On Wednesday, having digested the freshly release data, he said the euro was the biggest winner of the SNB’s reduction:

The EUR-share is the lowest since 2008 and indicates that the SNB was very quick to diversify away from the euros it amassed during the summer. This could mean that the SNB is still largely uncomfortable holding sizeable exposure to the single currency. In turn, this could imply that a potential adjustment higher in EURCHF peg maybe less likely ahead of the December SNB meeting. EUR ticked higher following the release potentially suggesting that investors were anticipating the selling pressure from the SNB to ease from here.

The results [showing that the share of non-euro currencies rose] highlight the SNB preference for liquidity in its assets. This seems to hold especially in the case of sterling with its share in reserves more than doubling despite the still weak economic outlook for the UK. In this regard we think that the AAA rating of the UK will continue to be an important support for sterling against EUR going forward.

We think that EUR could be supported following the SNB release especially against the G10 smalls especially if investors think that the reserves data implies that:

1/ The SNB maybe done cutting its EUR-longs

2/ The SNB prefers liquidity and less so quality of the euro alternatives

So, it seems both static reserves and a fall can be spun into euro positives. In the former case it’s a statement of confidence in the single currency’s prospects while in the latter it can be seen as a positive as the SNB might prefer to hold its remaining euros for the liquidity they provide. A necessary consequence of that decision would be less euros sold and thus less alternate currencies bought — something that would impact smaller currencies, such as the Swedish krona, in particular.

That idea is backed up by the euro reserves reverting to their 2008 level and Nomura argue that the decline suggests active diversification is now done and only further FX intervention to defend the floor would change this.

Of course you could also read the data in reverse — that a static figure would have suggested they couldn’t get rid of their euro holdings fast enough while the speedily falling figure suggests they want out of the euro and will keep up the rush to retreat, particularly if euro stress picks up in a meaningful way along with pressure on the SNB’s floor. Up to you really.

Related links:

The Swiss boson – FT Alphaville

Cofer catch-up time – FT Alphaville

The SNB’s bond buying: now with more context – FT Alphaville

Tags: FX,Reserves,Swiss National Bank