Two volatility ETFs (VXX and UVXY) are having almost half of the trading volume in the world’s largest ETF (SPY). How come?

First, the facts:

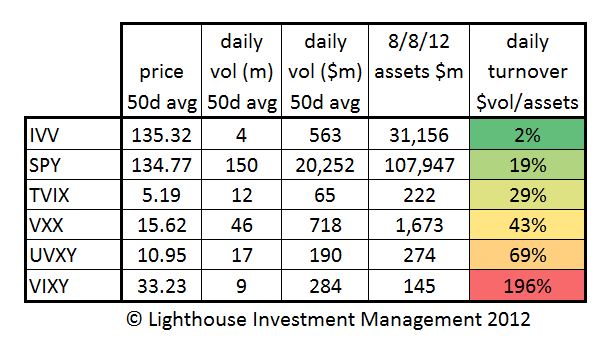

SPY is heavily traded (19% of assets daily turnover) compared to IVV (also referring to the S&P 500).

But then come the volatility ETFs. Tiny VIXY (assets $145m) turns itself over 2x per day.

Why are those long-volatility ETFs so popular, given they are wasting assets in an environment with a steep volatility-futures curve (source VixCentral):

(Ceterus paribus short-term long-vola ETF’s will suffer monthly roll-losses of 11% or roughly 0.5% per trading day)

The most likely explanation is that volatility-ETFs offer leverage without the need for margin:

On August 9, 2012, SPY had a trading range of 60bps. VXX offered 220bps, topped by UVXY with 440bps.

Tiny moves in the equity market can be amplified by using volatility ETFs (not that I would endorse this). It’s leverage without leverage for the day trader.

Alexander Gloy is founder and president of Lighthouse Investment Management.

Alexander Gloy is founder and president of Lighthouse Investment Management.

Tags: Alexander Gloy,Lighthouse Investment