Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

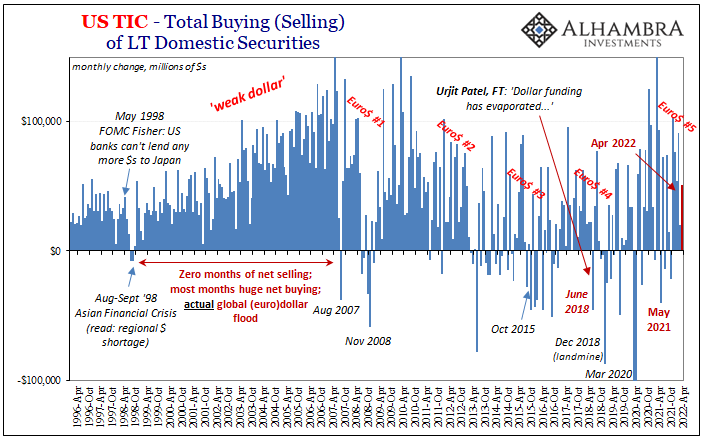

Angry April TIC Zeroed In On China’s CNY and Japan’s JPY

Angry April TIC Zeroed In On China’s CNY and Japan’s JPY21 Jun 2022

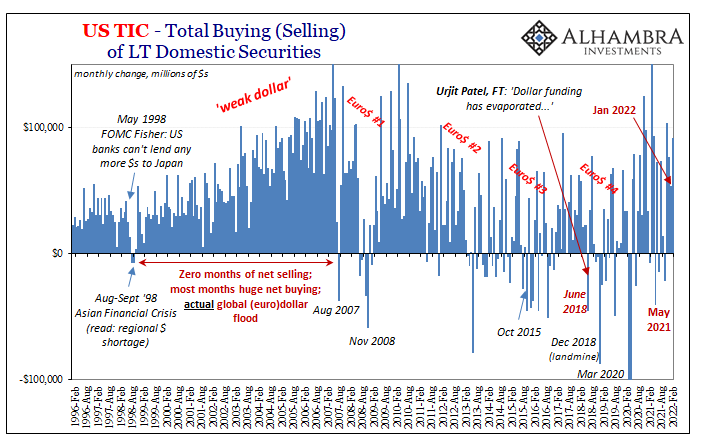

Looking Back At Chaotic March Through TIC20 May 2022

China, Japan, And The Relative Pre-March Euro$ Calm In February22 Apr 2022

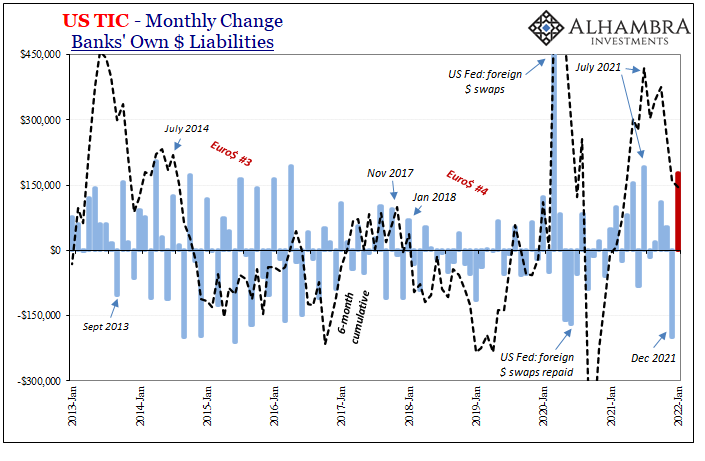

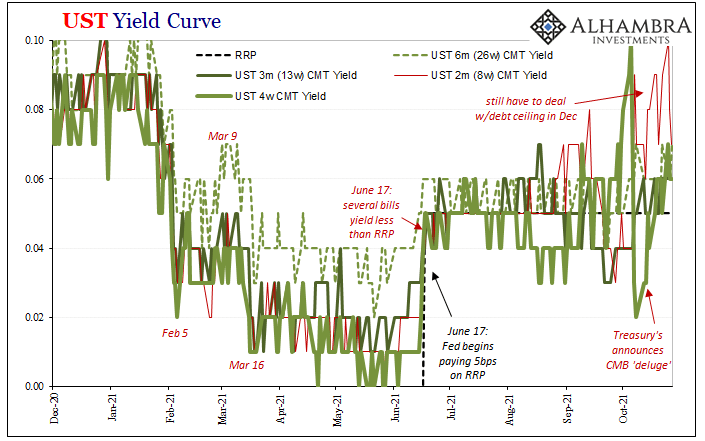

It Wouldn’t Be TIC Without So Much Other23 Mar 2022

Short Run TIPS, LT Flat, Basically Awful Real(ity)28 Oct 2021

Just Who Is, And Who Is Not, Selling T-Bills29 Nov 2020

If Dollar Is Fixed By Jay’s Flood, Why So Many TIC-ked At Corporates in July?21 Sep 2020

Part 2 of June TIC: The Dollar Why21 Aug 2020

So Much Dollar Bull27 May 2020

No Flight To Recognize Shortage

No Flight To Recognize Shortage22 May 2020

August TIC: Trying To Get Collateral Out of the Shadows23 Oct 2019

FX Daily, June 18: Draghi Ends Calm Ahead of FOMC, Sending the Euro and Yields Down18 Jun 2019

FX Daily, May 16: US Struggles to Strike a Less Strident Tone16 May 2019

FOMC Minutes: The New Narrative Takes Shape22 Feb 2019

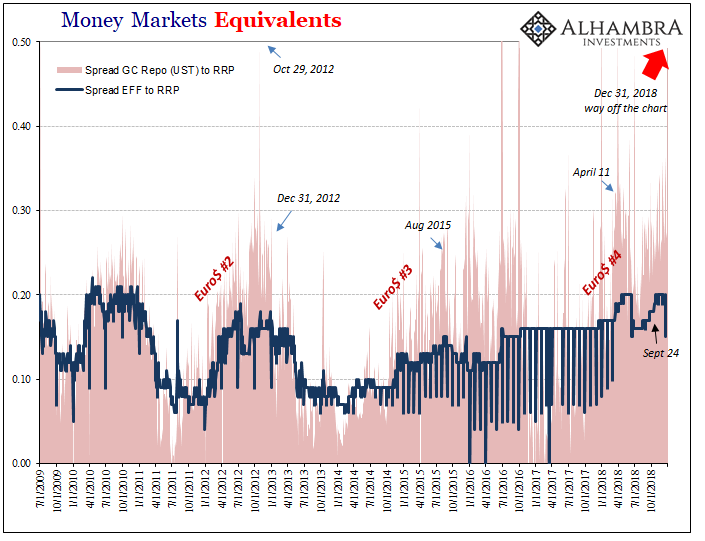

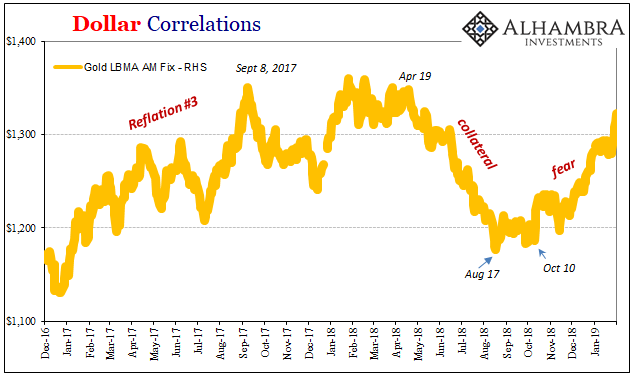

Fear Or Reflation Gold?4 Feb 2019

Capital Flocks to the US

Capital Flocks to the US19 Aug 2018

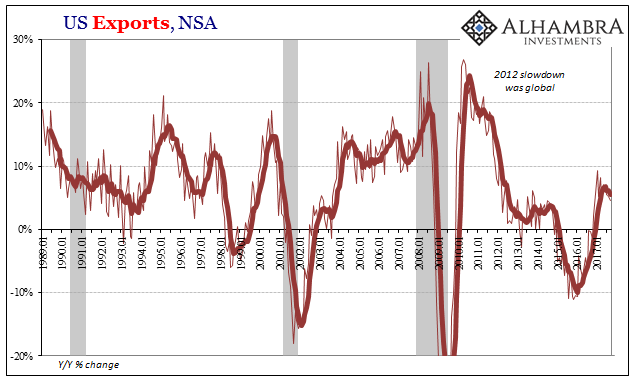

Synchronized Global Not Quite Growth10 Nov 2017

Swimming The ‘Dollar’ Current (And Getting Nowhere)26 Sep 2017

Moscow Rules (for ‘dollars’)

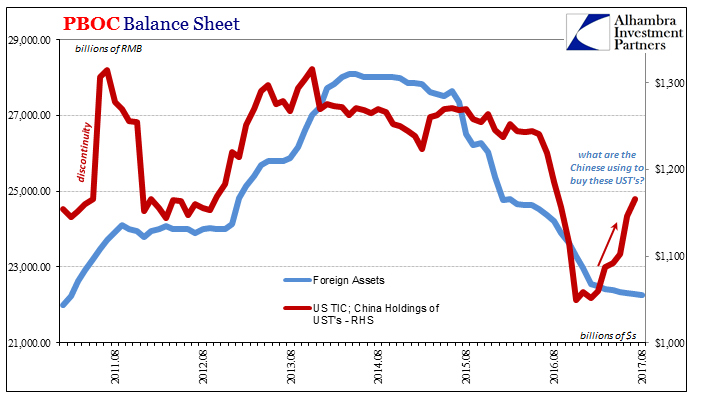

Moscow Rules (for ‘dollars’)2 Sep 2017

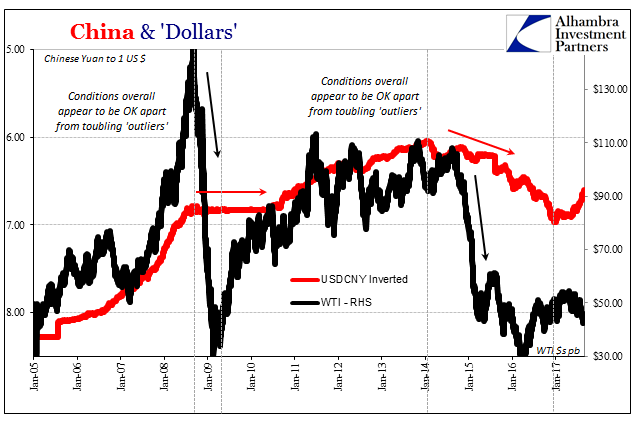

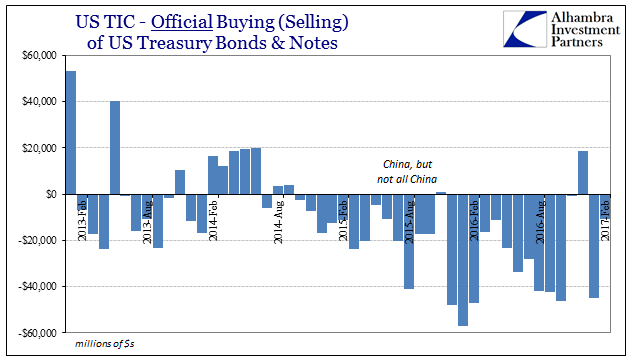

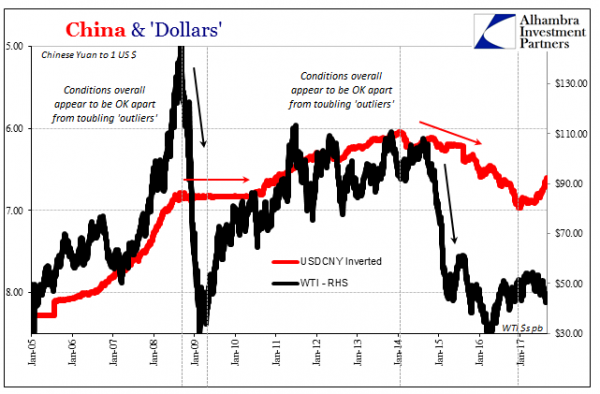

‘Dollar’ ‘Improvement’29 Apr 2017