Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Chart of the Week: The Dreaded Full Frown

Chart of the Week: The Dreaded Full Frown1 Jan 2019

And Now For Something Completely Different20 May 2018

The Science of Japanification28 Apr 2018

Good or Bad, But Surely Not Transitory19 Jan 2018

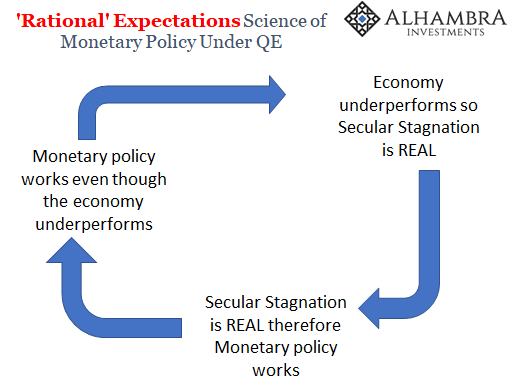

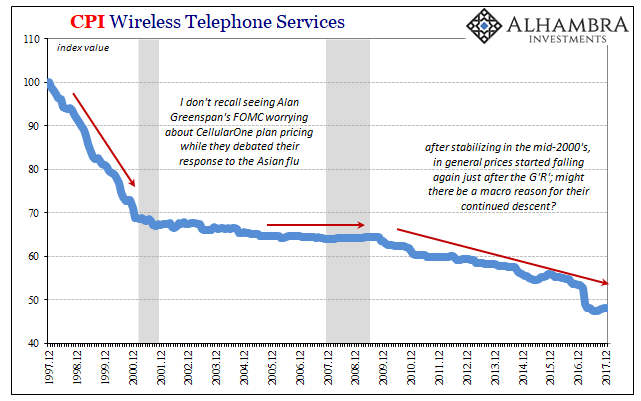

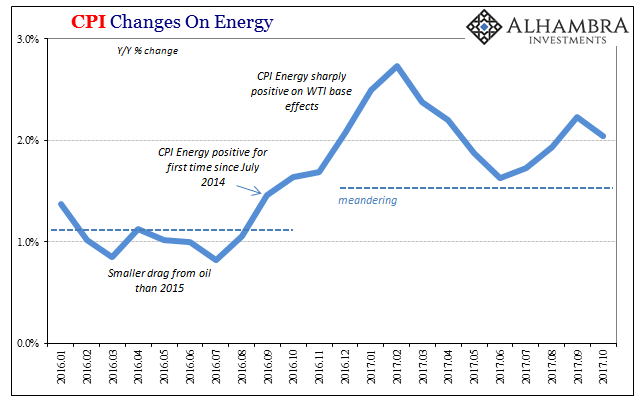

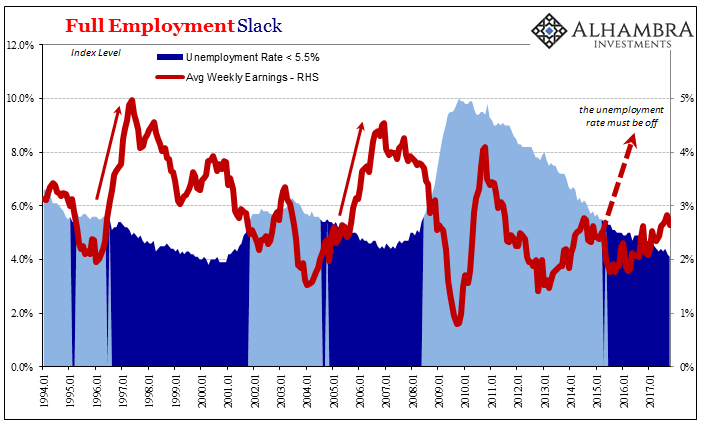

Can’t Hide From The CPI19 Nov 2017

What Central Banks Have Done Is What They’re Actually Good At18 Nov 2017

Oil Prices: The Center Of The Inflation Debate10 Aug 2017

US Federal Funds, Bond Market and WSJ Economic Survey: The Hidden State of Money13 Jul 2017

Maybe Deep Dissatisfaction Has A Point5 Jul 2017

Signs of Something, Just Not Wage Acceleration11 Jun 2017

Less Than Nothing25 May 2017

Further Unanchoring Is Not Strictly About Inflation

Further Unanchoring Is Not Strictly About Inflation18 Mar 2017

True Cognitive Dissonance4 Mar 2017