Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

“It’s A Perfect Storm Of Negativity” – Veteran Trader Rejoins The Dark Side

“It’s A Perfect Storm Of Negativity” – Veteran Trader Rejoins The Dark Side16 Jun 2017

25 Nov 2016

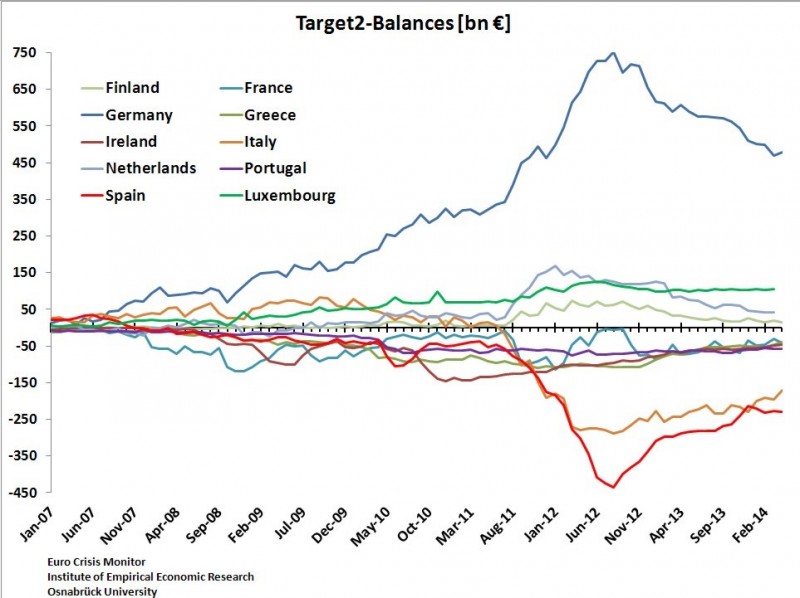

Negative Rates for Bundesbank TARGET2 Surplus?

Negative Rates for Bundesbank TARGET2 Surplus?13 Jun 2014

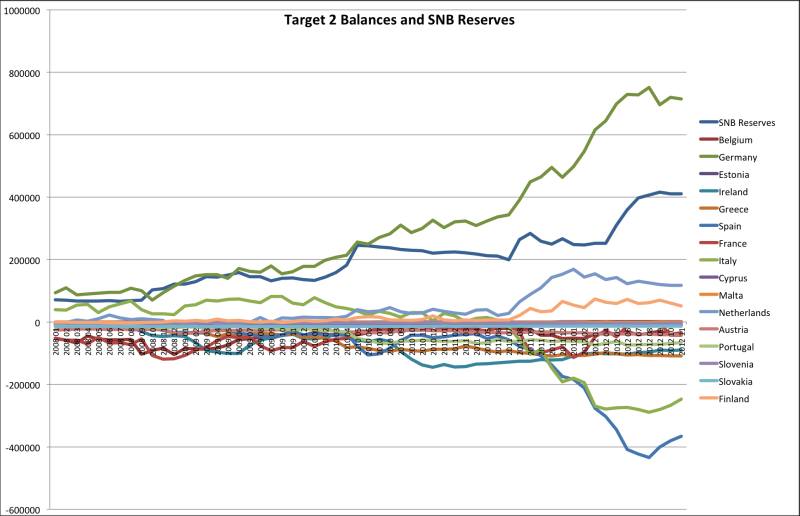

Target2 Balances and SNB Currency Reserves: Same Concept, Update February 20139 Feb 2013

Bad News for SNB: While Target2 Imbalances Diminish, SNB Reserves Remain the Same9 Feb 2013

German Currency and Gold Reserves and the German Trade Surplus17 Jan 2013

The Big Swiss Faustian Bargain: Differences between SNB, ECB and Fed Money Printing Explained3 Sep 2012

German constitutional court needs 3 months to decide about the injunction11 Jul 2012

The Northern Euro introduction: A retrospective from the year 203020 May 2012