Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: First, Kill All The Speculators

Weekly Market Pulse: First, Kill All The Speculators31 Jan 2023

Peak Policy Error1 Jun 2022

Collateral Shortage…From *A* Fed Perspective7 May 2022

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’21 Apr 2022

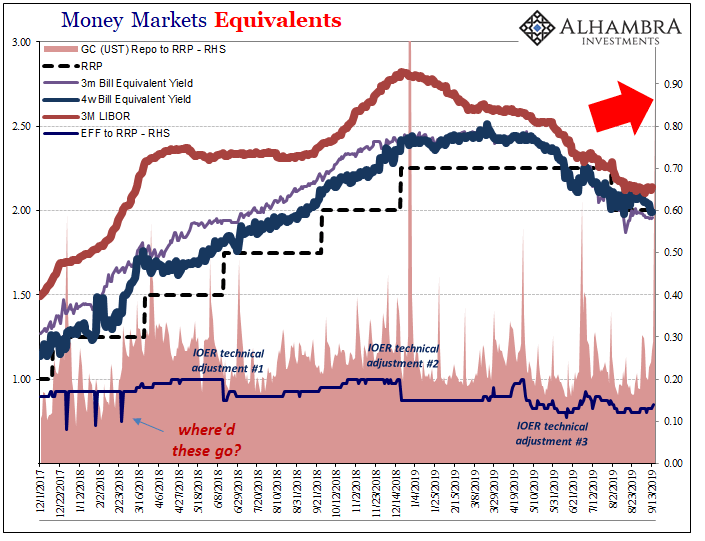

2019: The Year of Repo4 Jan 2020

Head Faking In The Empty Zoo: Powell Expands The Balance Sheet (Again)9 Oct 2019

Stuck at A: Repo Chaos Isn’t Something New, It’s The Same Baseline17 Sep 2019

FX Daily, February 13: QT is not the Opposite of QE13 Feb 2019