Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Peak Policy Error

Peak Policy Error1 Jun 2022

Some ‘Core’ ‘Inflation’ Difference(s)6 May 2022

A Clear Balance of Global Inflation Factors30 Jun 2021

Inflation Isn’t Just The Outlier, The Inflation In It Is, Too29 Jun 2021

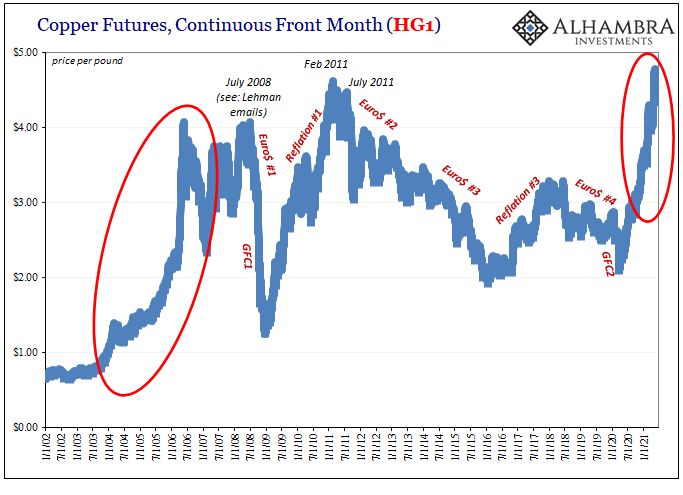

Copper Corroding PPI17 Jun 2021

All Signs Of More Slack7 Dec 2019

Big Difference Which Kind of Hedge It Truly Is3 Sep 2019

Globally Synchronized What?31 Jan 2018

Durable Goods Only About Halfway To Real Reflation25 Nov 2017

Can’t Hide From The CPI19 Nov 2017

Global Inflation Continues To Underwhelm19 Oct 2017

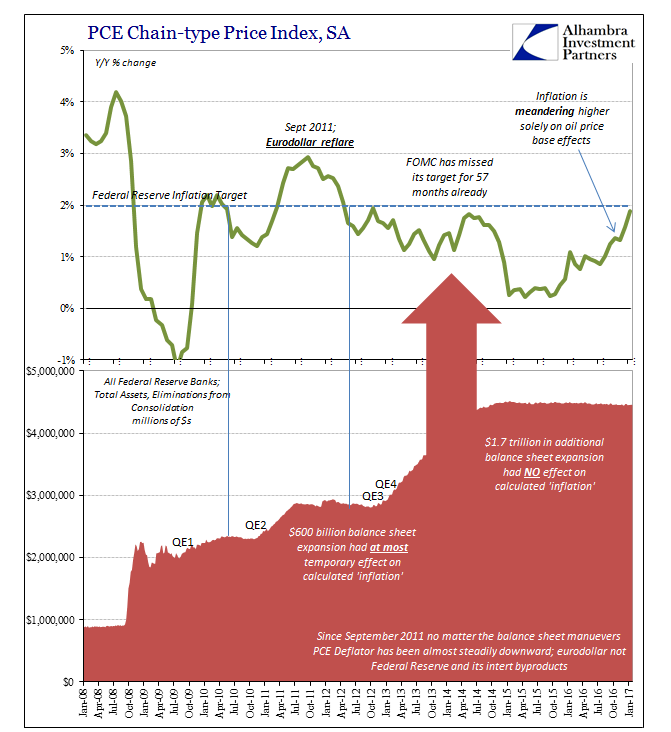

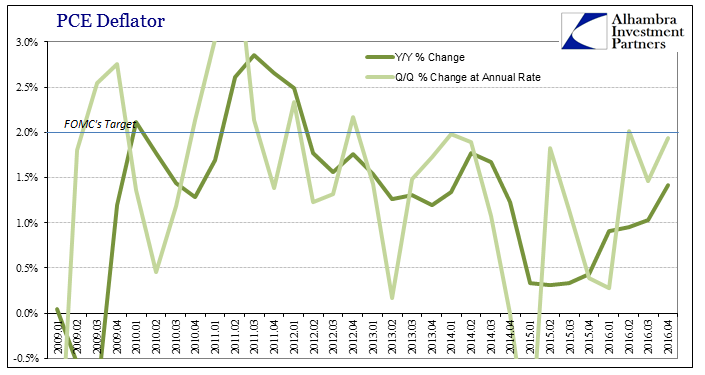

Non-Transitory Meandering12 Oct 2017

Toward The Housing Bubble, Or Great Depression?8 Sep 2017

Inflation Is Not About Consumer Prices4 Aug 2017

Global Manufacturing PMI’s, Inflation and CPI: Some Global Odd & Ends9 Jul 2017

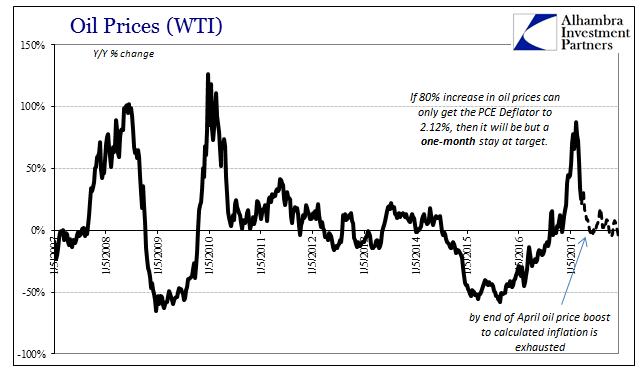

The Power of Oil2 Apr 2017

Real Disposable Income: Headwinds of the Negative3 Mar 2017

Some Notes On GDP Past And Present1 Mar 2017