Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Are Risk Appetites Recovering?

Are Risk Appetites Recovering?13 Aug 2024

Narrow Ranges for the Dollar Prevail Ahead of Tomorrow’s US CPI10 Jul 2024

Capital Markets are Calm though Anxiety Continues to Run High16 Oct 2023

The Dollar Consolidates after Powell Sapped its Mojo22 May 2023

Limited Follow-Through Dollar Buying After Yesterday’s Gains12 May 2023

Banking Stress Eases

Banking Stress Eases21 Mar 2023

Swiss National Bank Support Steadies Market as ECB Faces Difficult Choice16 Mar 2023

Upside Surprise in UK’s Flash PMI and Better-than-Expected January Public Finances Lift Sterling21 Feb 2023

Poor US Data Cast Doubts on New Found Hopes of a Soft-Landing

Poor US Data Cast Doubts on New Found Hopes of a Soft-Landing19 Jan 2023

Macro and Prices: Data and Psychology in the Week Ahead19 Nov 2022

Turn Around Tuesday Aside, is the Dollar Topping?18 Oct 2022

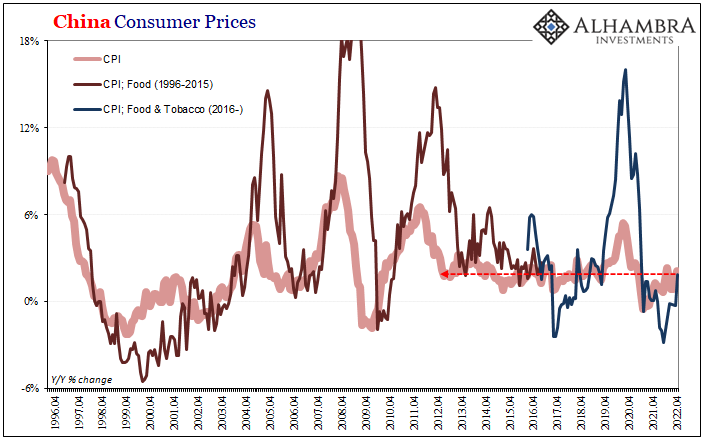

Synchronizing Chinese Prices (and consequences)14 May 2022

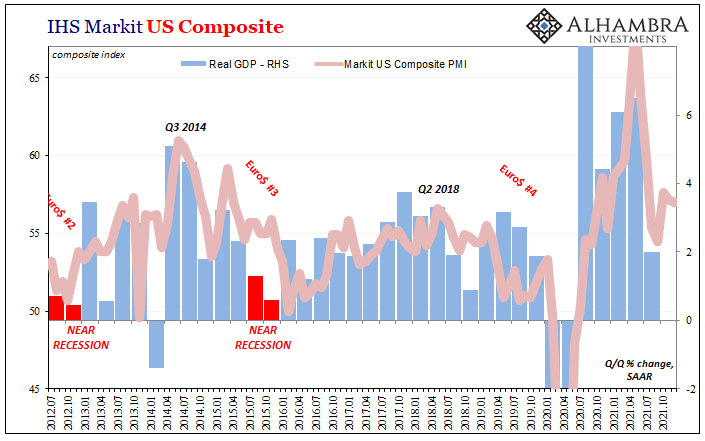

As The Fed Seeks To Justify Raising Rates, Global Growth Rates Have Been Falling Off Uniformly Around The World8 Jan 2022

Flash PMIs Play Second Fiddle to US PCE Deflator and Accelerating Inflation20 Nov 2021

Euro Bounces Back, but the Turkish Lira Remains Unloved18 Nov 2021

FX Daily, August 17: Antipodeans and Sterling Bear Brunt of Greenback’s Gains17 Aug 2021

FX Daily, February 26: Fed Hike Ideas Give the Beleaguered Greenback Support26 Feb 2021

FX Daily, February 24: Equities Try to Stabilize and Low Short-Term Rates Help Keep the Dollar on the Defensive24 Feb 2021

FX Daily, February 22: Stocks Wilt under Pressure from Rising Yields22 Feb 2021

FX Daily, November 11: Reduced Risk of Negative Policy Rates Lifts Sterling and the Kiwi11 Nov 2020