In the case of Italy, it will take a whole lot more – Part I of II

When the collapse of the Italian government was officially announced, on July 21, many political observers both in Europe and across the rest of the West, were aghast. If Mario Draghi, the central banking messiah of the entire Old World, the man, the legend, the hero who rescued the Eurozone and its precious made up currency from the brink of complete annihilation, failed to...

Read More »

Tag Archive: Mario Draghi

Even The People ‘Printing’ The ‘Money’ Aren’t Seeing It

Read More »

The global economy doesn’t care about the ECB (nor any central bank)

Read More »

The Greenspan Bell

Read More »

Christine Lagarde’s New Vision for the ECB

Read More »

Schaetze To That

Read More »

Germany, Maybe Europe: No Signs Of The Bottom

Read More »

Latest European Sentiment Echoes Draghi’s Last Take On Global Economic Risks

Read More »

The Consequences Of ‘Transitory’

Read More »

Big Trouble In QE Paradise

Read More »

No Longer Hanging In, Europe May Have (Been) Broken Down

Read More »

Your Unofficial Europe QE Preview

Read More »

The Obligatory Europe QE Review

Read More »

What’s Germany’s GDP Without Factories

Read More »

Not Buying The New Stimulus

Read More »

No Surprise, Hysteria Wasn’t a Sound Basis For Interpretation

Read More »

Fear Or Reflation Gold?

Read More »

It’s Not That There Might Be One, It’s That There Might Be Another One

Read More »

That’s A Big Minus

Read More »

Spreading Sour Not Soar

Read More »

On Swiss National Bank

On Swiss National Bank

-

Heads up for NZD and CHF traders, RBNZ Gov Breman and SNB Chair Schlegel to speak

-

Swiss franc appreciation has led to tighter monetary conditions – SNB minutes

-

SNB Sight Deposits: decreased by 3.1 billion francs compared to the previous week

-

SNB’s Chairman Schlegel: A few months of negative inflation wouldn’t be a problem

-

2025-07-31 – Interim results of the Swiss National Bank as at 30 June 2025

Main SNB Background Info

Featured and recent

-

Mittelschicht? Ist warten auf den Sarg!

Mittelschicht? Ist warten auf den Sarg! -

Steuergeld & Sprache Die geheimen Kontrollmechaniken aufgedeckt!

Steuergeld & Sprache Die geheimen Kontrollmechaniken aufgedeckt! -

Hochbrisant: Regierung KAPITULIERT vor AfD-Anfrage! Sie wissen nicht welche NGOs Geld erhalten!

Hochbrisant: Regierung KAPITULIERT vor AfD-Anfrage! Sie wissen nicht welche NGOs Geld erhalten! -

Maximale Performance? Wie die Kombi aus Bitcoin und Gold laut Citi den Unterschied macht

Maximale Performance? Wie die Kombi aus Bitcoin und Gold laut Citi den Unterschied macht -

Achtung: “Offene Feldschlacht” zwischen Union und SPD!

Achtung: “Offene Feldschlacht” zwischen Union und SPD! -

Aktienanlagen nach Netto-Einkommensgruppe

Aktienanlagen nach Netto-Einkommensgruppe -

Israeli settler violence in the West Bank is rising | The Economist

Israeli settler violence in the West Bank is rising | The Economist -

Dieses Event bringt sie alle zusammen – bist du dabei?

Dieses Event bringt sie alle zusammen – bist du dabei? -

Das wird dir keiner im Fernsehen sagen – Frank Pöpsel spricht Klartext

Das wird dir keiner im Fernsehen sagen – Frank Pöpsel spricht Klartext -

Kalkofes TOTAL-Schaden gegen AfD! Massive Blamage geht steil!

Kalkofes TOTAL-Schaden gegen AfD! Massive Blamage geht steil!

More from this category

- “Whatever it takes”:

2 Aug 2022

- Even The People ‘Printing’ The ‘Money’ Aren’t Seeing It

7 Feb 2021

- The global economy doesn’t care about the ECB (nor any central bank)

14 May 2020

- The Greenspan Bell

22 Apr 2020

Christine Lagarde’s New Vision for the ECB

Christine Lagarde’s New Vision for the ECB5 Mar 2020

- Schaetze To That

26 Feb 2020

- Germany, Maybe Europe: No Signs Of The Bottom

19 Jan 2020

- Latest European Sentiment Echoes Draghi’s Last Take On Global Economic Risks

19 Dec 2019

- The Consequences Of ‘Transitory’

8 Oct 2019

- Big Trouble In QE Paradise

7 Oct 2019

- No Longer Hanging In, Europe May Have (Been) Broken Down

24 Sep 2019

- Your Unofficial Europe QE Preview

14 Sep 2019

- The Obligatory Europe QE Review

13 Sep 2019

- What’s Germany’s GDP Without Factories

9 May 2019

- Not Buying The New Stimulus

8 Mar 2019

- No Surprise, Hysteria Wasn’t a Sound Basis For Interpretation

28 Feb 2019

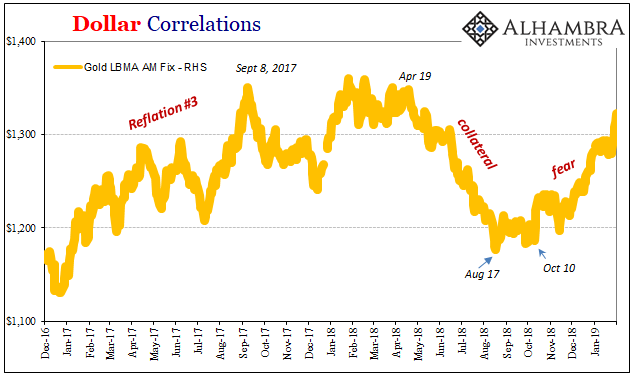

- Fear Or Reflation Gold?

4 Feb 2019

- It’s Not That There Might Be One, It’s That There Might Be Another One

1 Feb 2019

- That’s A Big Minus

19 Jan 2019

Spreading Sour Not Soar

Spreading Sour Not Soar18 Jan 2019