Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

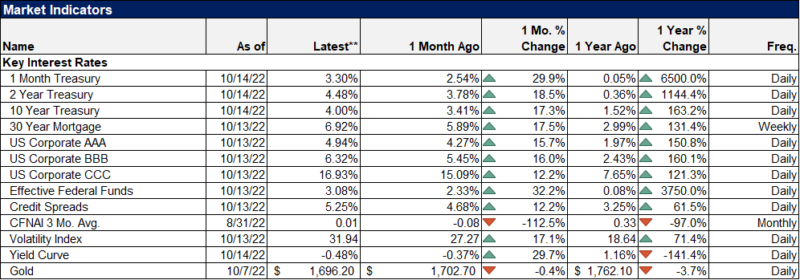

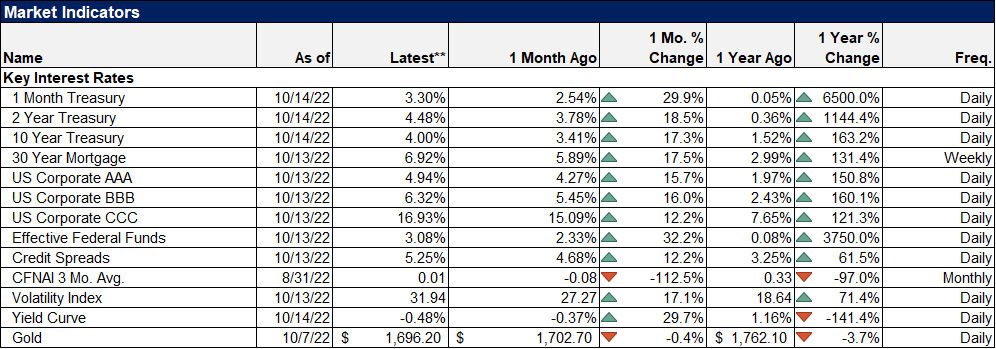

Weekly Market Pulse: Just A Little Volatility

Weekly Market Pulse: Just A Little Volatility17 Oct 2022

The Russians (Propaganda) Are Coming!

The Russians (Propaganda) Are Coming!15 Sep 2022

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay2 Oct 2020

Powell Would Ask For His Money Back, If The Fed Did Money5 Sep 2020

Wait A Minute, What’s This Inversion?28 Jun 2020

Not COVID-19, Watch For The Second Wave of GFC227 Jun 2020

18 Jun 2020

Cool Video: A Quick Review of the the FOMC and a Look to Next Week13 Jun 2020

Cool Video: The Liquidity Hypothesis6 Jun 2020

So Much Bond Bull21 May 2020

COT Black: No Love For Super-Secret Models

COT Black: No Love For Super-Secret Models1 May 2020

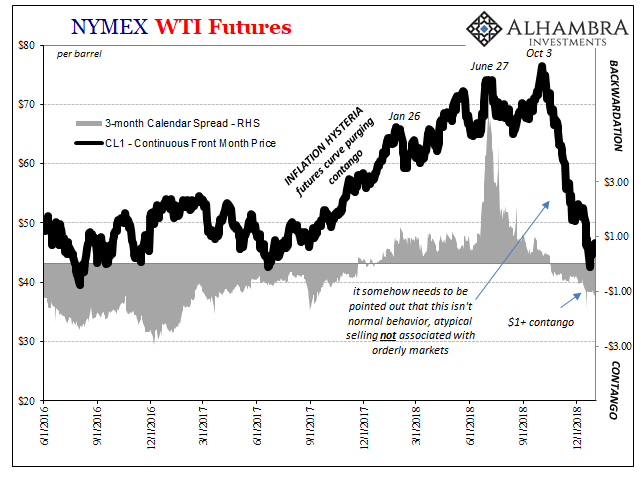

Three Short Run Factors Don’t Make A Long Run Difference25 Mar 2020

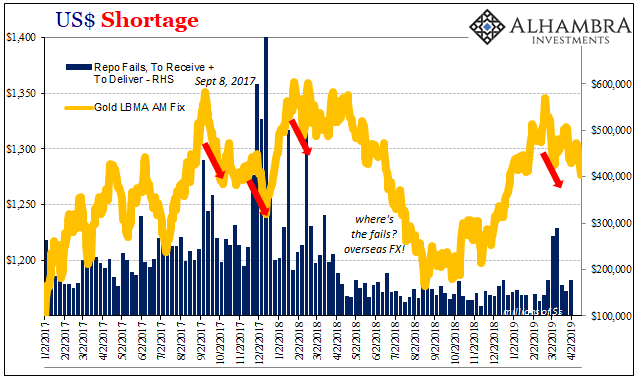

Is Now a Good Time to Buy Gold? Market Report 16 March16 Mar 2020

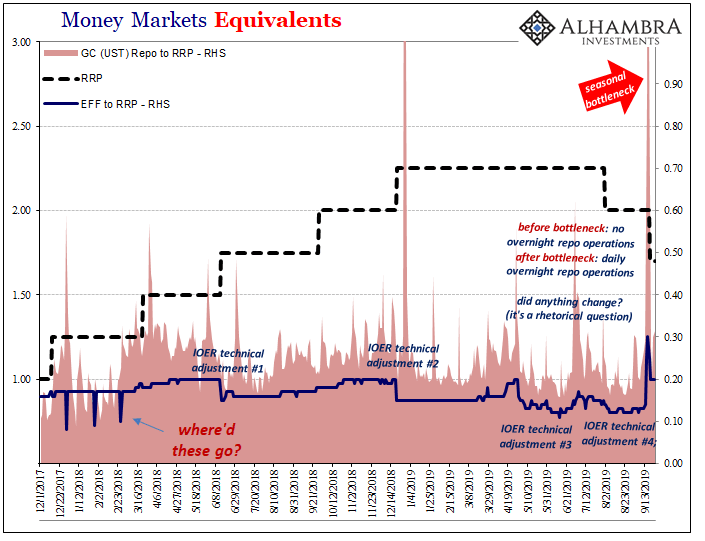

2019: The Year of Repo4 Jan 2020

Tidbits Of Further Warnings: Houston, We (Still) Have A (Repo) Problem18 Oct 2019

Head Faking In The Empty Zoo: Powell Expands The Balance Sheet (Again)9 Oct 2019

Money Markets: Sizing Up the Cavalry26 Sep 2019

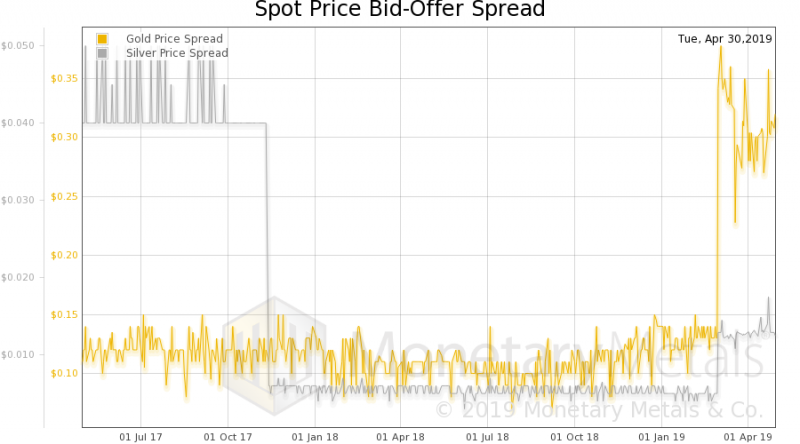

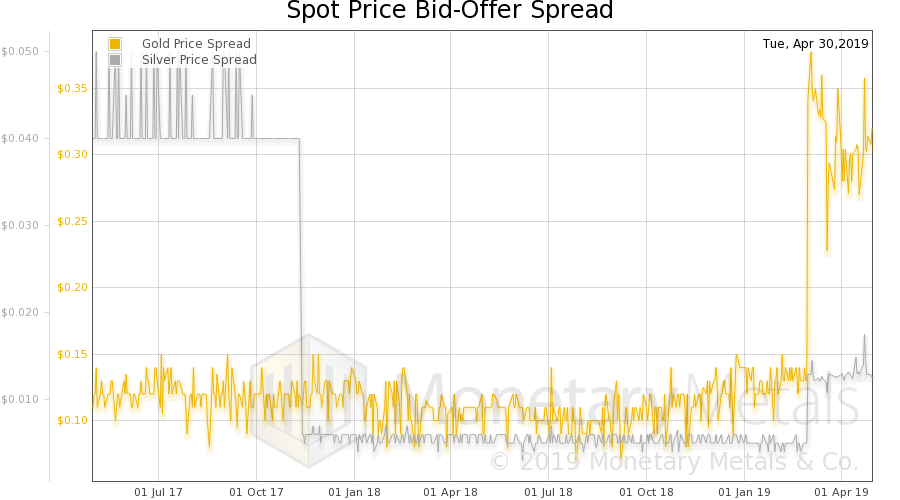

The Spreads Blow Out, Update 1 May

The Spreads Blow Out, Update 1 May2 May 2019

COT Blue: Distinct Lack of Green But A Lot That’s Gold24 Apr 2019

Nothing To See Here, It’s Just Everything4 Jan 2019