Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

The Biggest Risk, No Surprise, Collateral

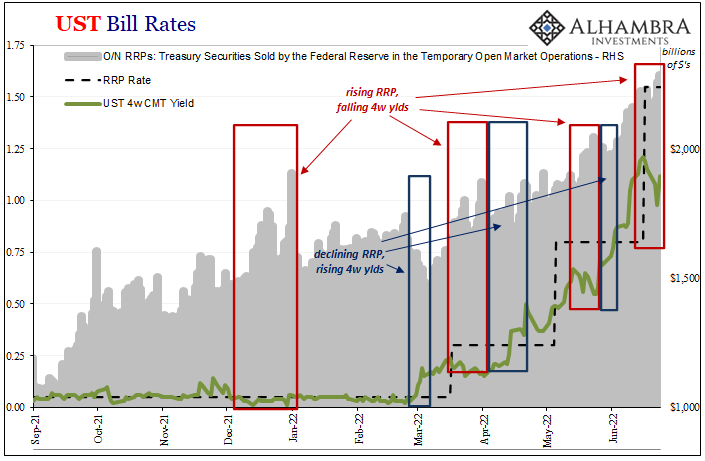

The Biggest Risk, No Surprise, Collateral28 Jun 2022

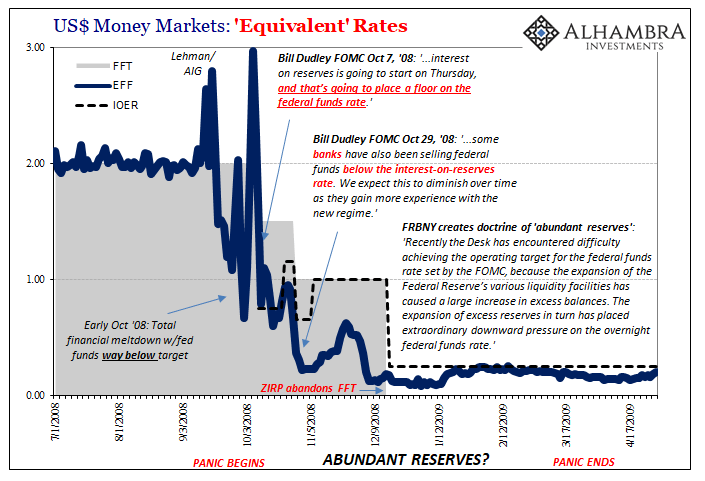

Collateral Shortage…From *A* Fed Perspective7 May 2022

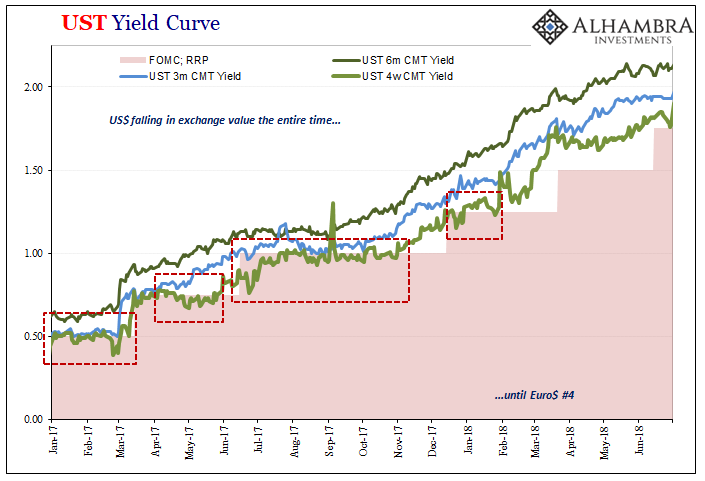

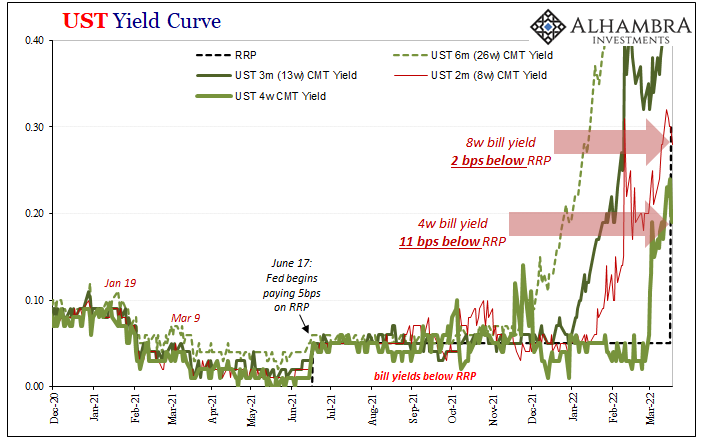

The Fed Inadvertently Adds To Our Ironclad Collateral Case Which Does Seem To Have Already Included A ‘Collateral Day’ (or days)21 Mar 2022

CPI’s At Fives Yet Treasury Auctions12 Aug 2021

Tidbits Of Further Warnings: Houston, We (Still) Have A (Repo) Problem18 Oct 2019

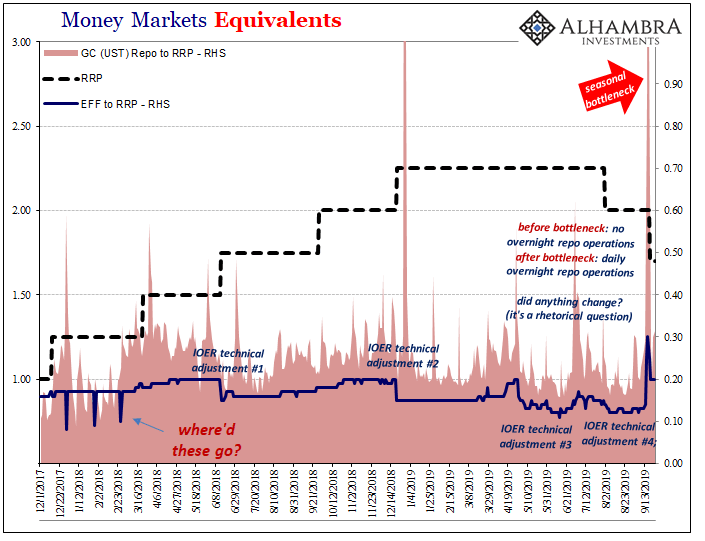

Money Markets: Sizing Up the Cavalry26 Sep 2019

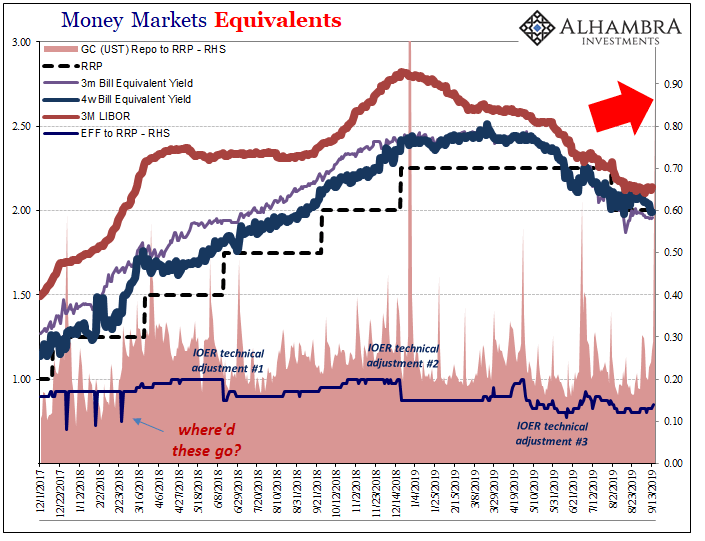

Stuck at A: Repo Chaos Isn’t Something New, It’s The Same Baseline17 Sep 2019

How To Properly Address The Unusual Window Dressing5 Jul 2019

Phugoid Dollar Funding4 Apr 2019

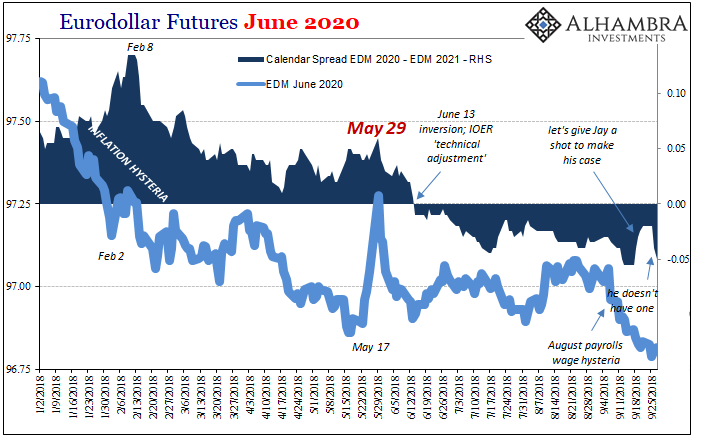

Make Your Case, Jay28 Sep 2018

Why The Fed’s Balance Sheet Reduction Is As Irrelevant As Its Expansion27 Sep 2017

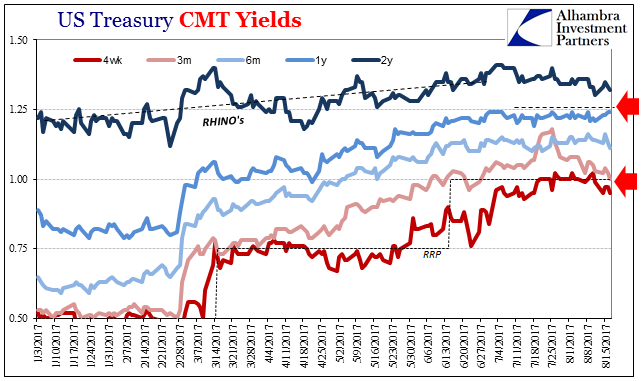

United States: The Fed Tries To Tighten By Rates, But The System Instead Tightens By Repo23 Aug 2017