Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: The Turkey Leg

Weekly Market Pulse: The Turkey Leg23 Jun 2025

Weekly Market Pulse: Questions

Weekly Market Pulse: Questions14 Oct 2024

Weekly Market Pulse: Did The Fed Just Make A Mistake?

Weekly Market Pulse: Did The Fed Just Make A Mistake?23 Sep 2024

Weekly Market Pulse: It’s An Uncertain World

Weekly Market Pulse: It’s An Uncertain World3 Sep 2024

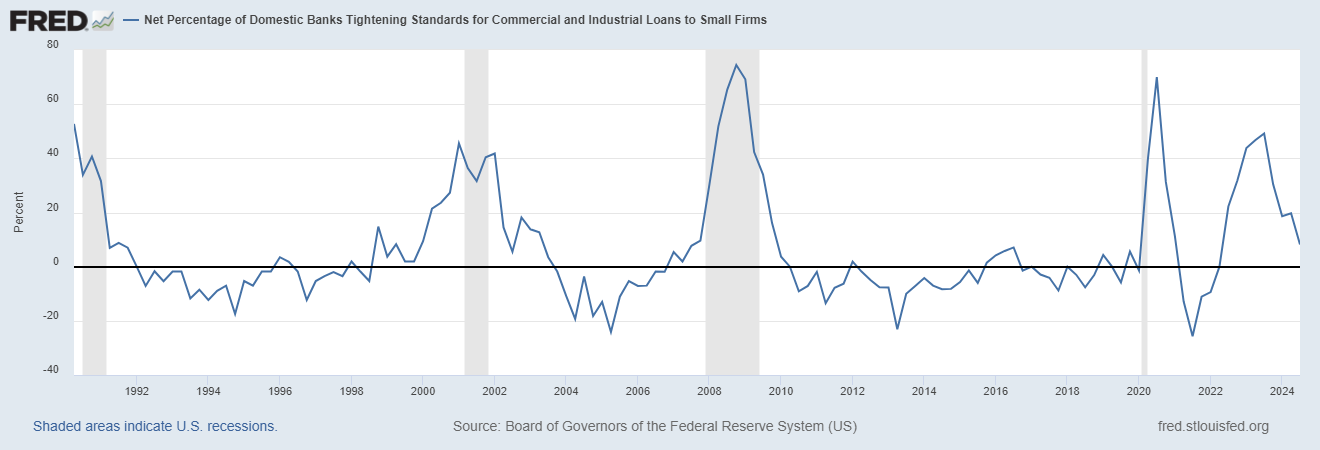

Market Morsel: SLOOSing

Market Morsel: SLOOSing6 Aug 2024

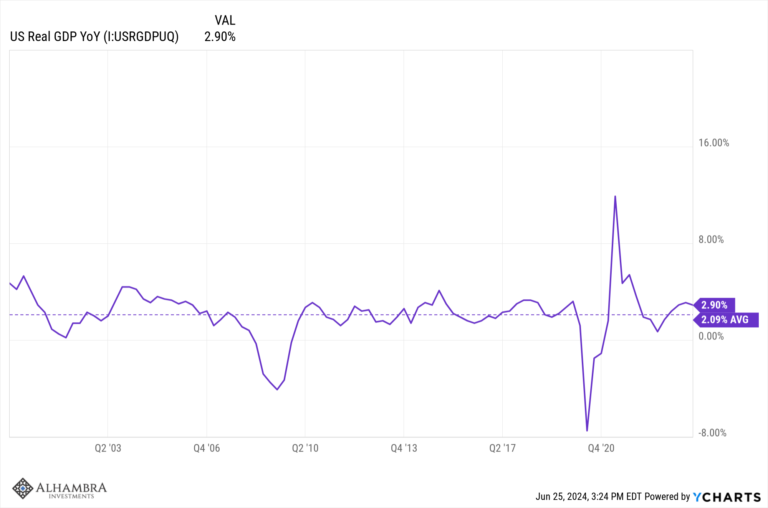

Q3 Cyclical Outlook

Q3 Cyclical Outlook25 Jun 2024

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?15 Apr 2024

Weekly Market Pulse: Happy Days Are Here Again!

Weekly Market Pulse: Happy Days Are Here Again!7 Feb 2023

Weekly Market Pulse: First, Kill All The Speculators

Weekly Market Pulse: First, Kill All The Speculators31 Jan 2023

Weekly Market Pulse: A Fatal Conceit

Weekly Market Pulse: A Fatal Conceit24 Jan 2023

Weekly Market Pulse: The Consensus Will Be Wrong

Weekly Market Pulse: The Consensus Will Be Wrong9 Jan 2023

Weekly Market Pulse: Happy Holidays

Weekly Market Pulse: Happy Holidays20 Dec 2022

Weekly Market Pulse: Good News, Bad News

Weekly Market Pulse: Good News, Bad News14 Nov 2022

Powell’s Epiphany: There is No Free Lunch p2 Neutralizing the Money is Inflationary

Powell’s Epiphany: There is No Free Lunch p2 Neutralizing the Money is Inflationary25 Oct 2022

25 Oct 2022

Weekly Market Pulse: Did Powell Just Blink?

Weekly Market Pulse: Did Powell Just Blink?24 Oct 2022

Market Currents: Fed Confusion

Market Currents: Fed Confusion20 Oct 2022

Weekly Market Pulse: Just A Little Volatility

Weekly Market Pulse: Just A Little Volatility17 Oct 2022

Weekly Market Pulse: The Real Reason The Fed Should Pause

Weekly Market Pulse: The Real Reason The Fed Should Pause11 Oct 2022

Weekly Market Pulse (VIDEO)

Weekly Market Pulse (VIDEO)4 Oct 2022