Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Rick Rule – Gold Helps Me Sleep at Night

Rick Rule – Gold Helps Me Sleep at Night14 Oct 2022

A Volcker Pan Recession10 Jun 2022

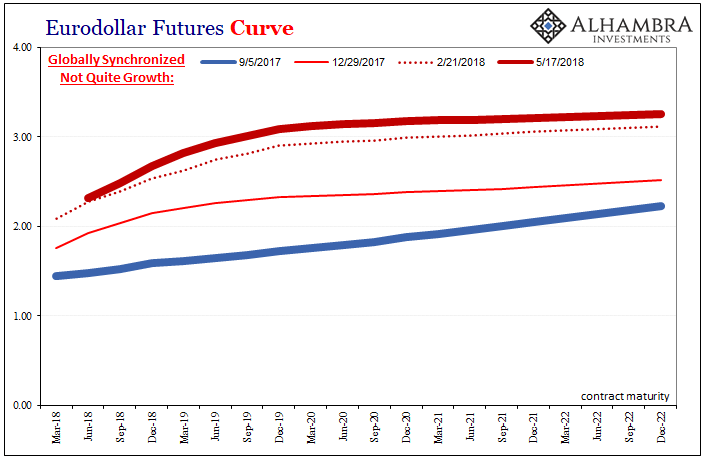

Hong Kong Stocks Pivot Euro$ #528 May 2022

RRP (use) Hits $2T, SOFR Like T-bills Below RRP (rate), What Is (really) Going On?27 May 2022

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?25 May 2022

Inversion Is The Real March Madness, Just Don’t Take It Literally22 Mar 2022

The Fed Inadvertently Adds To Our Ironclad Collateral Case Which Does Seem To Have Already Included A ‘Collateral Day’ (or days)21 Mar 2022

Consumer Prices And The Historical Pain(s)12 Mar 2022

So Much Fragile *Cannot* Be Random Deflationary Coincidences

So Much Fragile *Cannot* Be Random Deflationary Coincidences10 Mar 2022

The Red Warning24 Feb 2022

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**28 Jan 2022

Good Time To Go Fish(er)ing Around The Yield Curve21 Jan 2022

US CPI Reaches Seven On US Goods Prices, With Disinflation Setting In Everywhere Else (incl. US Services)16 Jan 2022

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)25 Dec 2021

Start Long With The (long ago) End of Inflation24 Dec 2021

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century22 Dec 2021

Playing Dominoes19 Dec 2021

Testing The Supply Chain Inflation Hypothesis The Real Money Way18 Dec 2021

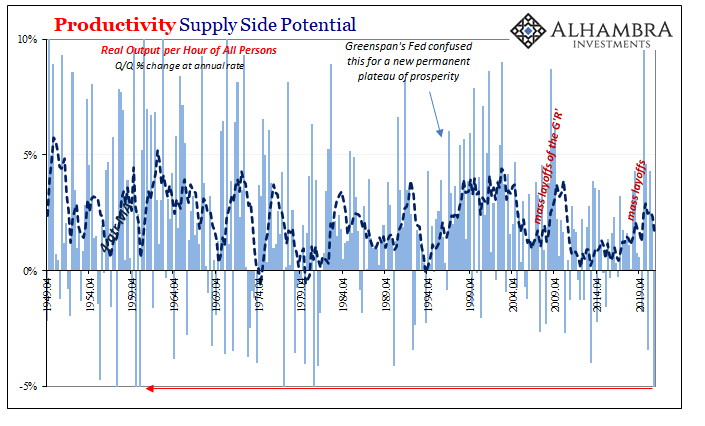

The Productive Use Of Awful Q3 Productivity Estimates Highlights Even More ‘Growth Scare’ Potential8 Dec 2021

This Is A Big One (no, it’s not clickbait)2 Dec 2021

Rick Rule – Gold Helps Me Sleep at Night

2022-10-14

by Stephen Flood

2022-10-14

Read More »