Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Is the West repeating India’s mistakes?

Is the West repeating India’s mistakes?26 Jul 2020

Reject the “Next Generation EU Plan”

Reject the “Next Generation EU Plan”13 Jun 2020

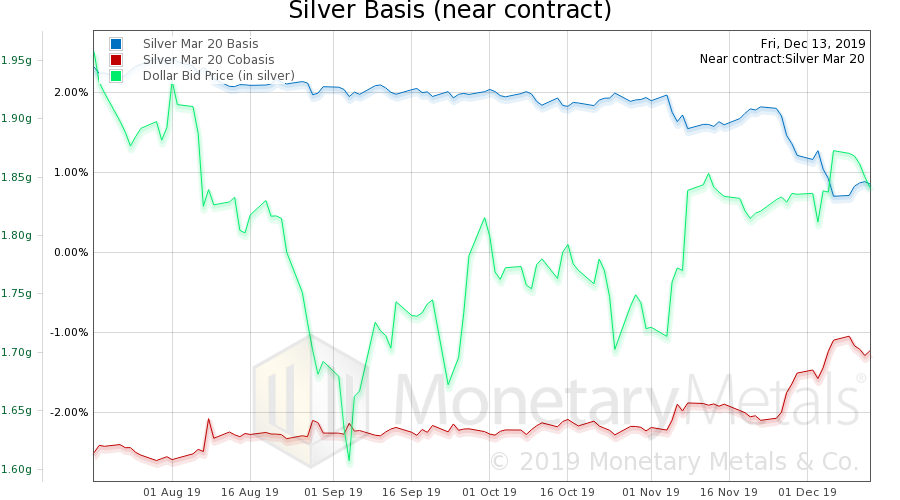

Open Letter to John Taft, Report 17 Dec

Open Letter to John Taft, Report 17 Dec18 Dec 2019

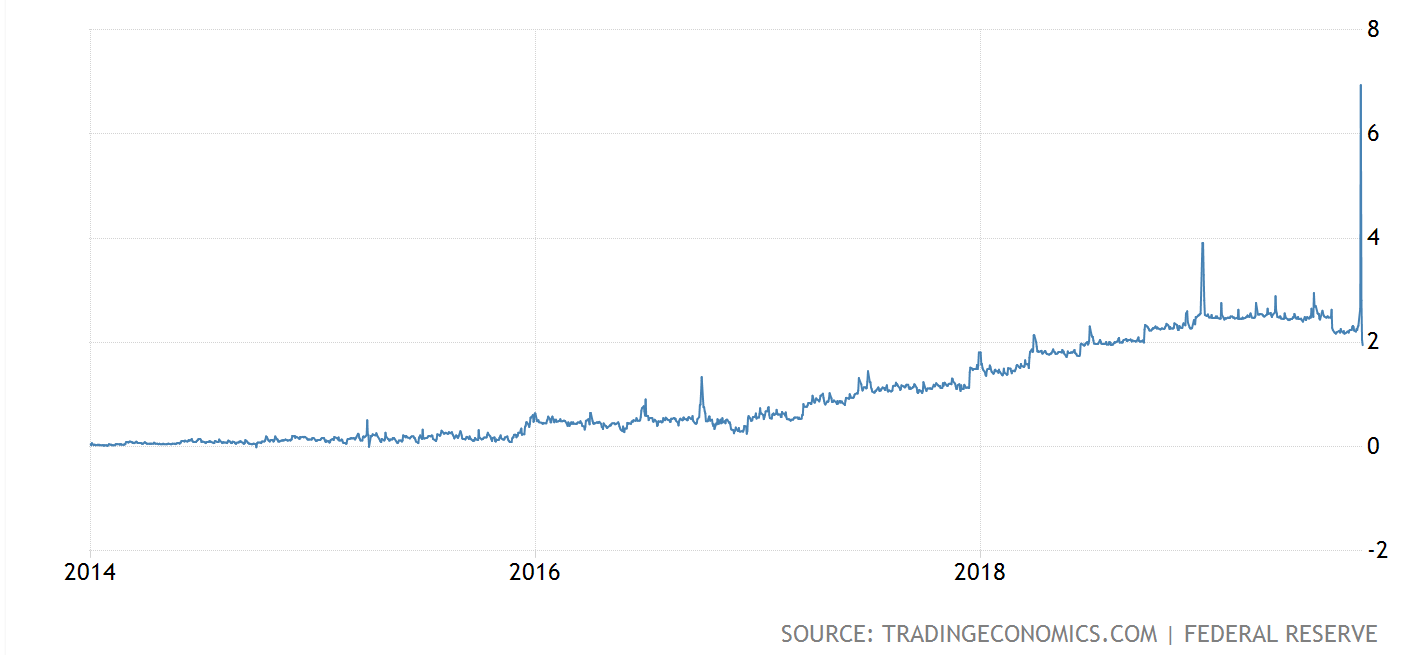

Targeting nGDP Targeting, Report 3 Nov

Targeting nGDP Targeting, Report 3 Nov5 Nov 2019

Treasury Bond Backwardation, Report 22 Sep

Treasury Bond Backwardation, Report 22 Sep24 Sep 2019

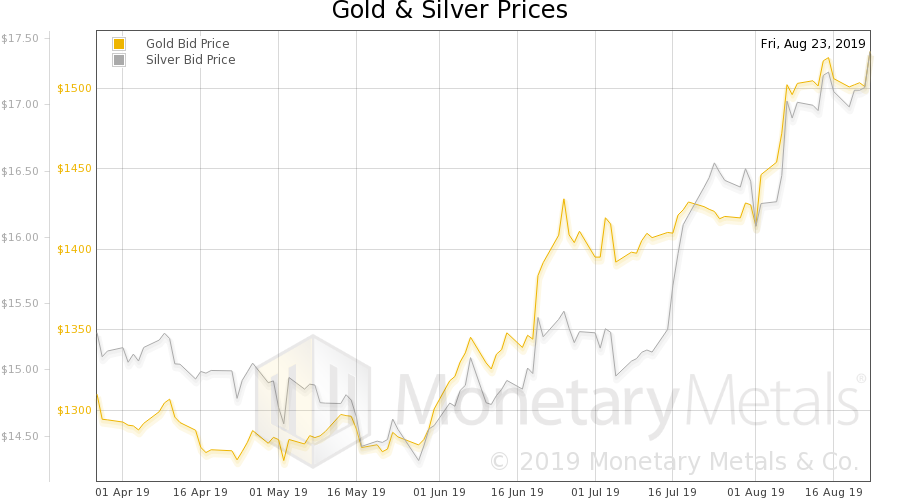

Directive 10-289, Report 25 Aug

Directive 10-289, Report 25 Aug26 Aug 2019

GDP Begets More GDP (Positive Feedback), Report 30 June

GDP Begets More GDP (Positive Feedback), Report 30 June2 Jul 2019

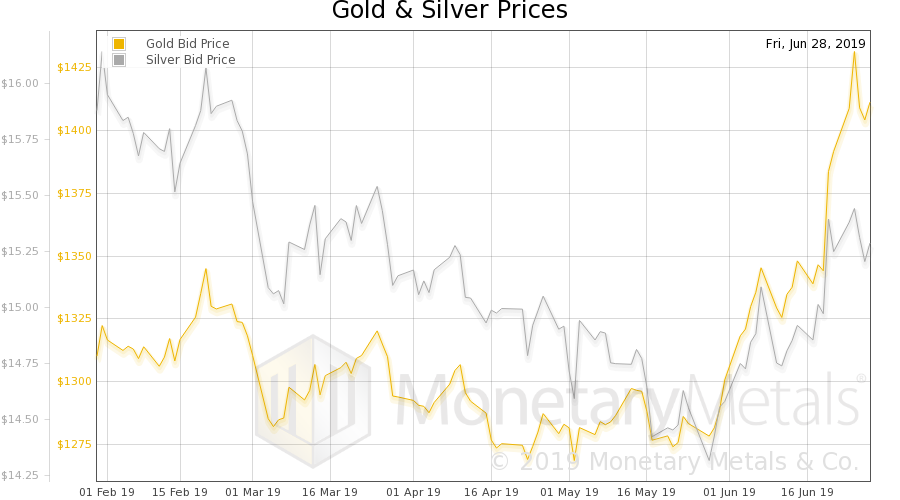

What Gets Measures Gets Improved, Report 23 June

What Gets Measures Gets Improved, Report 23 June25 Jun 2019

Is Capital Creation Beating Capital Consumption? Report 3 Mar4 Mar 2019

Central Planning Is More than Just Friction, Report 17 February19 Feb 2019

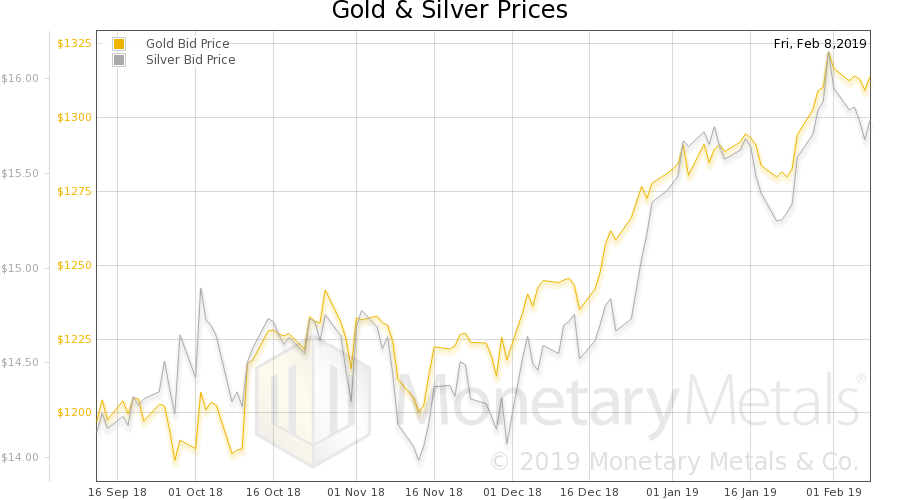

What They Don’t Want You to Know about Prices, Report 10 Feb

What They Don’t Want You to Know about Prices, Report 10 Feb11 Feb 2019

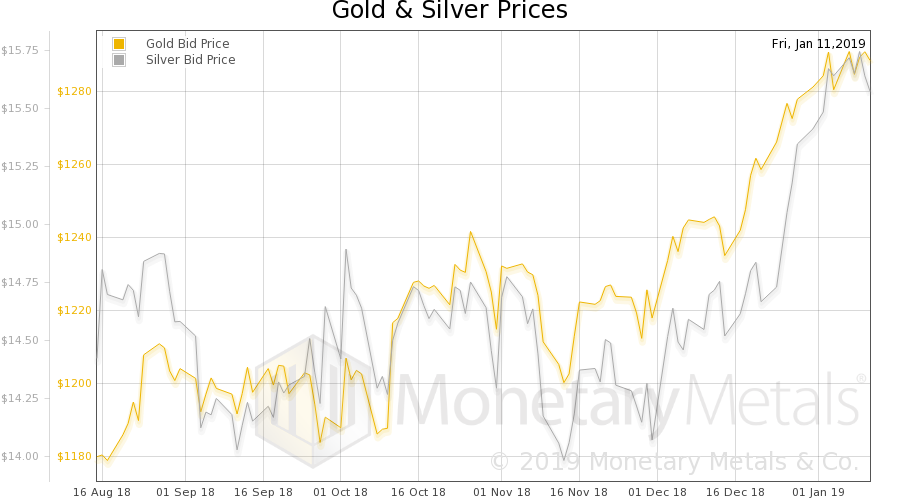

Rising Interest and Prices, Report 13 Jan 2019

Rising Interest and Prices, Report 13 Jan 201914 Jan 2019

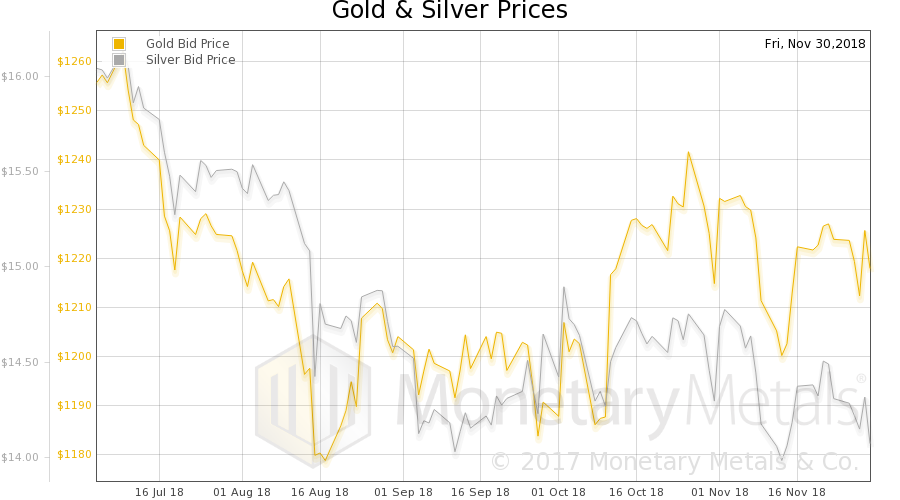

Inflation, Report 2 Dec 2018

Inflation, Report 2 Dec 20183 Dec 2018

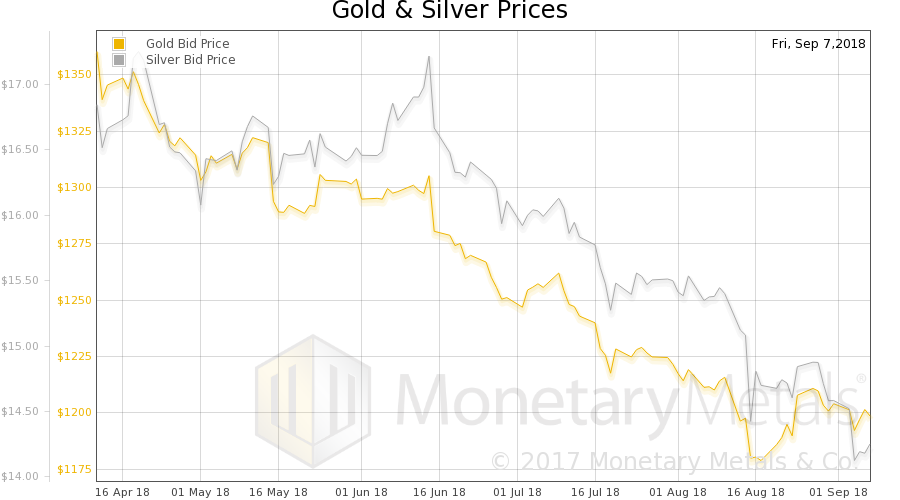

Why the Fed Denied the Narrow Bank, Report 9 Sep 2018

Why the Fed Denied the Narrow Bank, Report 9 Sep 201811 Sep 2018