George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Week February 7 and 14, 2015: With more and more forecasts that the Swiss economy could slow, the inflows in sight deposits have stopped. The EUR/CHF has stabilized around 1.06. But we rather think that local spending thanks to lower prices and higher purchasing power could neutralize the negative effects of the stronger currency for exporters. Moreover, many exporters have started cutting costs, some even at board level (example story Straumann via WSJ). Strong gains of the SMI since January 15th, confirms this picture.

January 30, 2015: Another rise of 15 billion CHF. In particular deposits of local banks at the SNB rise, but not the ones of non-banks and foreign banks.

On the other side, the slow upwards movement of the franc from 1.00 suggests that the SNB is driving the franc lower and the euro higher.

The resistance and end point of SNB interventions should be exactly there where SNB seigniorage income can avoid a bankruptcy of the central bank The rumours about a “new floor” or trading band between 1.05 and 1.10 seem to be nonsense. We strongly question if the SNB is ready to absorb so much liquidity 1.05 or higher. Therefore we rather think that they intervene between 1.00 and 1.05.

January 23: That the sight deposits have increased implies that the SNB has intervened: Another rise of 26 bln. CHF despite a more expensive franc. The intervention amount could have been the equivalent of 40-70 bln. if CHF costed less, for example with a EUR/CHF peg of 1.20. At this weekly pace the balance sheet could have doubled its size quickly. The verdict would have been to join the euro zone, otherwise the central bank would have been bankrupt.

January 16 data: End of peg: negative interest increase to minus 0.75%. Sight deposits rose by a total of 14 billion. It reaches the same weekly values as April-August 2012. During that period the SNB was obliged to massively blow up its balance sheet, by a total of 250 billion. In 2012 it doubled the size of its balance sheet. Any balance sheet expansion (with positive interest rates on sight deposits) increases the risks of a asset prices bubble and the financial risks. It also exacerbates the risk of price inflation in later stadium that would require a stronger franc so that the SNB can fight inflation.

Why New Keynesians or Market Monetarists cannot understand that the SNB intervention is not needed any more in times of strong optimism in United States? Moreover they ignore that in the US asset price inflation already translates into price inflation, so it will in Switzerland.

Should the SNB adopt the EUR, file for bankruptcy or remain in negative equity for many many years?

Jordan has given the response in a crystal clear speech in September 2011, see more on my recent Twitter messages

January 02, 2015 and January 09: Slight increase of 2 billion CHF.

December 26: Another rise of 12 billion CHF. In our “SNB Negative Rates, a Toothless Measure?” we explained that paying 0.25% interest rates is nothing compared to holding assets in Rouble or other currencies of Emerging Markets. Investors prefer wealth preservation and not yield on investments. We judge that EUR/USD at 1.22 or lower is not sustainable for the SNB. It might be possible that rich Germans are already inflation-hedging against higher German wages and ECB QE using Swiss franc investments.

December 19: SNB admits that it has intervened. The euro had fallen again under 1.24$, this made the intervention necessary: Swiss stocks are becoming increasingly cheap for American investors, in particular given that 25% of the turnover of Swiss blue-chips goes to the US. Swiss chemicals take advantage of cheap oil, the Swiss pharmaceuticals profit on Obamacare.

Banks must pay negative interest rates for this increase, more costs for them. Any rise against the threshold, as of mid November implies paying 0.25% from January 22, 2015 on. Moreover, about 5% of existing sight deposits are subject to this fine.

December 12: Once again total sight deposits decreased, but the franc gained in value against both USD and EUR.

Once again Swiss banks reduced sight deposits, while other sight deposits (incl. foreign banks) are increasing.

Falling Swiss bank deposits suggests that lending to the Swiss private sector is rising, this is a CHF against CHF switch, hence FX neutral.

The Swiss banks are slowly finding a better place for their liquidity.

Readers should be aware that interventions are not 1:1 against sight deposits: Deposits of Swiss banks might even decline when interventions take place. In 2010-2011 this regularly happened, Swiss banks increased lending, reduced sight deposits while the SNB intervened, in particular in April 2010.

We judge that the SNB has intervened, reasons are:

- Price action, the EUR is stuck at 1.2011 CHF, the dollar depreciated last week.

- Rising foreign inflows visible in other sight deposits

Astute readers could ask: how can sight deposits fall, they are SNB’s firepower, the means of financing interventions?

The answer is simpler than you would think: Valuation effect.

Falling USD and EUR means falling assets/reserves on one side of the balance sheet; hence the other side – the sight deposits – must fall, too. This leaves some room for “unobserved” or “stealth” SNB interventions.

One will also understand why the SNB has not introduce negative rates yet, because they are fully aware that lending to Switzerland is rising, but lending to foreign from Switzerland, e.g. for Emerging Markets is collapsing. If this tendency continues for some years then inflation will finally come. Negative rates will fuel lending to Switzerland even more.

November 24: Before the gold referendum, the SNB had to intervene again: 2.7 billion CHF, SNB’s sight deposits came out at 370.8 bn, this is up from 368.2 bn the previous week

Earlier data data shows that the SNB has not intervened until mid November 2014. Sight deposits plus currency in circulation have remained stable for months. Between November 2012 and December 2013, the SNB managed to reduce sight deposits by 9 bln. francs.

It should also be mentioned that investors exited CHF investments between September 2011 and March 2012, in fear of a higher minimum rate. The SNB decided to buy the francs investors were selling and not to raise the minimum rate. See the author’s post “SNB Buys Swiss Francs And Sells Euro: Welcome To The EUR/CHF Peg” on Zerohedge)

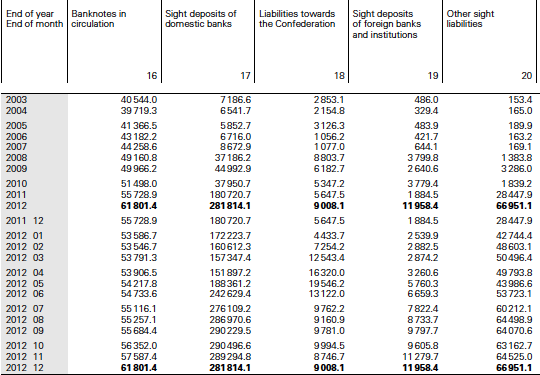

Thompson-Reuters provided a nice overview graph on weekly changes in sight deposits. We added some missing explanations. The data contains only the deposits of Swiss banks. In June 2013, Swiss Postfinance obtained a banking license. This was a move of 25 bln. CHF from “other sight deposits” into “sight deposits of Swiss banks”, but no SNB intervention.

On the next page some historical headlines and more historic data.

Some Selected Headlines from 2013

Update for the week ending July 19, 2013:

UBS: “We have been net sellers of CHF for 5 weeks in a row now – a pattern we have not seen since shortly after the SNB put in the floor.”

July 22, 2013

Despite UBS private clients selling CHF, there was no substantial change in SNB sight deposits. They are 1.5 bln. CHF under the record-high of 371.6 bln. CHF See full history below.

Update for the week ending July 5:

Total sight deposits down by 700 million CHF. Where is the money flowing?

Two possibilities:

- Out of the franc or

- Do Swiss banks increase lending and simply remove the funds from the central bank, because they have more profitable use for it?

Update for the week ending June 28: 25 million CHF will reclassified from “other” to “local sight deposits”.

Since PostFinance Ltd was granted a banking licence on 26 June 20 13, its sight deposit account is reported under the sight deposits of domestic banks item and no longer under the other deposits on sight in Swiss francs item. (source SNB)

Update for the week ending March29, 2013 Slight decrease of 300 million francs, driven by “other deposits” (companies, foreign banks) that showed 1 bln. CHF that moved out of the franc, while Swiss banks moved in franc investments. The weak ISM PMI of 51.2 on April 1, is an early warning of the typically harder times for the SNB from May on.

Update for the week ending March22: Despite the Cyprus crisis, only slight increase of 370 million francs. This time more local banks moved in the franc, but others (companies, Swiss state and foreign banks) are down.

Update February 22: Adding bank notes to the sight deposits, total SNB liabilities rise to a new record level.

Total sight deposits increased slowly to 370.9 billion francs, which is just 2.8 bln. under the record level of September. The ones of local banks, however, are higher by 3 billion francs and even 7 billion since the beginning of February. Bank notes, another type of central bank liabilities reached a high record high: The latest balance sheet shows that they are 6 billion francs or 10% higher than in September.

Update January 17: Since last week the SNB is buying reserves again, and increasing its liabilities in francs. In the first week of January we suspect a sterilization of 4 billion CHF from sight deposits to local banks into other deposits, possibly into liabilities to the Swiss confederation; a method used previously. Since the Swiss CPI was weaker than expected (-0.2% MoM on Friday, the SNB should get the data earlier), the SNB did not continue to sterilize last week.

Draghi’s talking up of the euro, the weak CPI and rumors about negative interest rates at ZKB, let the EUR/CHF rise to 1.24 via bullish FX traders. These FX traders may close their positions, take profit and the pair will fall again.

Still ZKB just changed general conditions to be ready for negative rates. Other banks are able to introduce them without changing conditions.