Jake Huneycutt

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

Originally written and commented on February,19 2014 in Seeking Alpha Italy: The New ‘Powder Keg’ Of Europe In the article fully cited further below by

The executive summary of his article:

- Italian growth issues could ignite broader eurozone crisis.

- Falling Italian bond yields deceiving due to ECB intervention.

- Italian GDP improvement partly driven by falling imports rather than fundamental improvement in trade.

- ECB’s Long-Term Refinancing Operation may have simply increased risks of an Italian banking crisis

- Italian government bonds are one of the worst investments in the world on risk-adjusted basis.

The response by George Dorgan:

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

(Contrarian, hedge fund manager, macro)

George Dorgan: The New Widow-Maker Trade: Short Italian Government Bonds

Thank you, Jake, for the collection of good information and charts. However, your analysis that Italian government bonds and stocks would be overvalued is DEEPLY FLAWED. You are missing some basic understanding of global macro, bond pricing theory and mentalities.

Some reasons are:

1) Shorting Italian government bonds, as you might suggest, could be another widow-maker trade, similar to shorting JGBs. Both Japan in the early 2000 and Italy or Spain today have in common that they have current account surpluses and very low (Italy) or negative (Spain) wage increases in 2013.

Italian Government Bond Yields Since 2011 (yields are inversely related to price)

The main driver for government bonds is local demand from risk-averse investors, e.g. banks, insurances or pension funds. Behind that the driver of bond yields is and remains inflation that those conservative investors have to account for. European austerity and slow growth has destroyed the expectation that wages or inflation rise in the mid-term future, similarly as the bust of the Japanese bubble did.

Investors remember that Italian workers wanted wage increases that were higher than inflation (so-called “Scala Mobile”). At the time, the scala mobile often caused an “inflationary spiral”: weaker lira, higher inflation, higher wages, weaker lira…

But … the lira is gone …

Why have U.S. treasuries fallen in price? The main reason is that investors expect U.S. wages and inflation to rise again.

More about inflation expectation as main driver of bond yields can be found here.

You claim to be a contrarian. For a real contrarian like we are, Italian bonds and Italian banks are still cheap.

2) Similarly as JGBs, the risk for Italian government bonds is very limited. The reason is that Italians, similarly as Japanese, have relatively high private wealth.

I suggest this graph from Credit Suisse or our chapter on the ECB wealth reports, “Why median Italians are richer than Germans“. In these surveys, Italians could give information about their wealth without disclosing data to tax authorities.

I suggest this graph from Credit Suisse or our chapter on the ECB wealth reports, “Why median Italians are richer than Germans“. In these surveys, Italians could give information about their wealth without disclosing data to tax authorities.

Since 1999, wage earners have profited more than entrepreneurs. Salaries have risen too much, they are 15%-20% too high. Most of this inflation was initiated during the euro introduction period when many businesses, e.g. restaurants increased prices. Salaries followed with time.

This is the problem Italian companies face today. But on the other side, rising salaries combined with higher home prices are reflected in the 3rd world position for Italy in median wealth.

Your graph of 1980-2011 GDP growth, where Italy is weak: How much is this GDP data reliable in the case of Italy?

How much black wealth have Italians accumulated which is not reflected in your GDP figures?

Similarly as one of the ministers, many Italians have one home which is declared to tax authorities, one other not declared.

3) Coming to debt: Many Italians have accumulated their wealth thanks to high-yielding government bonds. If you look at sector balances, then you will grasp that private spending is often reversely related to government spending. Wealth is so, too: If the government is poor, like the Italian one, then people are rich, like Italians. No wonder Italians received high yield on government bonds over years and protected themselves against inflation with homes.

4) Coming to stock valuations, you will not deny that Italian stocks are still historically undervalued:

The FTSE MIB has risen from 14000 to 20000, but it is still under the low of 2002 with 21700 and far lower than in 1997, when it was at 24000.

The FTSE MIB has risen from 14000 to 20000, but it is still under the low of 2002 with 21700 and far lower than in 1997, when it was at 24000.

5) Coming to P/E ratios: You are saying that the Italian PE ratio is 29. You probably know why Shiller uses the 10 years average and not a single year. Due to the austerity measures, households savings rate has rapidly risen from 4% to over 10%. Italian companies are quite focused on local and European consumers. Austerity in 2012/2013 has severely hit, the 29 is hence an out-layer that over the years will get better.

For the U.S. it is different: The Fed forced American households to spend with the wealth illusion that Quantitative Easing created. The American P/E ratio of 18 is relatively high. I would rather short U.S. stocks than Italian ones.

6) You may have remarked that Germans started spending more than previously. As opposed to Italians, Germans do not need to do austerity, they have high savings and rising salaries. Italian exports to Germany are increasing now, but in 2012/2013 Germans did not spend, the Italian P/E ratio was 29. Italy builds up now a strong current account surplus, similar to Japan until 2008. Falling imports are not only an indication of low spending and the necessary adjustment of wages but also that local products are getting more competitive.

7) Wage expectations are far more important for stock valuations than P/E ratios. For years Emerg. Markets stocks have not risen for years. They have low P/E ratios and seem to be interesting, but high pay rises and the expectation of further pay rises destroys their future profits and their share prices. More here.

8) Another point are Italian banks. With the LTRO they were able to pick up Italian governmenent bonds at yields of 5-6%. They have made an enormous profit on it and continue to earn the interest each year. On their balance sheets, bonds are probably not valued Mark to Market (MTM), but held to maturity and valued at purchasing price. This weakens current earnings but improves future earnings.

One of the biggest banks, Unicredit, has huge income from its German subsidiary “Hypo Vereinsbank” that profits from the German savings boom.

9) Another flaw: Saying German house prices are in a bubble. Please compare price to income ratios since the 1990s, e.g. in the Economist and you will understand that the U.S. and the UK see overvalued house prices, but not Germany.

I admit that everything depends if Italian employees are ready to renounce on wage increases. But thanks to high unemployment and to the impossibility to devalue the currency compared to the strong German competition, I think that the “Scala Mobile” will not come back any time soon. A second condition is that the Italian housing market does not contract too much, this could lead to general deflation and lower spending. But as opposed to other countries (like Spain), there was no big housing bubble in Italy.

_________________________________

In following the rest of Jake’s article

Jake Huneycutt: Italy, The New ‘Powder Keg’ Of Europe

In the decades leading up to World War I, the Balkans gained a reputation as the “powder keg” of Europe. Nationalist movements in Southeast Europe were often pitted against the imperialism of the major European powers. The assassination of Austrian Archduke Franz Ferdinand by Serbian nationalists in 1914 would eventually set off a chain of events that would culminate in one of the most violent, miserable, and pointless conflicts in world history.

100 years later, it’s not virulent nationalism or imperialistic expansion that threatens continental Europe; it’s the Euro. By combining the currencies of 17 different sovereign nations into one giant dysfunctional system; trade imbalances, fiscal crises, and asset bubbles have become the norm.

While the markets believe that the situation is improving due to higher GDP growth and falling bond yields, if we dig beneath the surface, we can see that things are still deteriorating rapidly. All it might take is one small triggering event and the eurozone could spiral back into crisis mode.

In 2014, there are several sources of problems, including a housing bubble in Germany, increasing growth struggles in France, and a still problematic Greece. Yet, Italy is the nation that could probably be most accurately identified as Europe’s new powder keg.

The 2011 – 2012 Policy Response to the Eurozone Crisis

We might consider late 2009 to be the official start of the eurozone crisis. Around that time, markets grew concerned about a Greek default creating cascading series of problems across all of Europe. The situation deteriorated until late 2011 and early 2012, with bond prices for many of the weaker Southern states rapidly plunging. Yields on 10-year sovereign bonds rose as high as 48% in Greece, 17% in Portugal, 7.5% in Spain, and 7% in Italy. The Eurozone nations and the European Central Bank [“ECB”] took definitive actions to rein in the crisis, including a Greek bailout package with a 50% haircut on sovereign debt, and the Long-Term Refinancing Operation [“LTRO”] initiated by the ECB.

The LTRO is of particular importance here. Under the program, the ECB extended $1.02 trillion in loans with low interest rates (typically around 1%) to a group of over 800 Eurozone banks, primarily situated in Spain, Italy, Greece, France, and Ireland. These loans had a term period of 36 months, which means many will expire around early 2015. With the influx of cash from the LTRO, the eurozone banks bought up massive quantities of their own sovereign debt (and often, the debt of other distressed eurozone nations), which caused bond prices to soar and yields to plunge. The LTRO also boosted bank profits in distressed eurozone nations.

While the LTRO temporarily alleviated financing concerns, it did little to fix the larger problems driving the Eurozone Crisis. It was the ultimate “band-aid” solution, providing an artificial stimulus, but no solution to large trade imbalances or growth troubles. Indeed, austerity measures (which mostly consisted of large tax increases on the distressed nations, not significant spending reforms) have likely exacerbated problems further.

In spite of a sanguine market environment, the situation in the eurozone has become significantly worse since early 2012. Italy’s debt has grown and economic growth has still been poor. Meanwhile, on the north side of Europe, Germany is running a massive current account surplus at 8% of GDP, and appears to be in the midst of an asset bubble, primarily fueled by easy money policies, and trade advantages provided by the euro.

Eurozone Markets and Economy

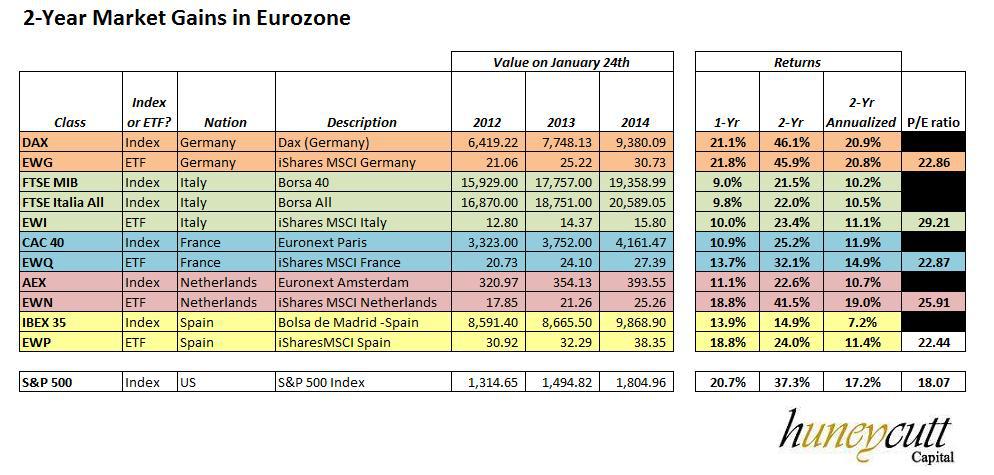

If Italy and many eurozone nations are struggling, it’s difficult to tell from the markets’ reactions over the past 18 months. As of late January, The German DAX was up 21.1% over the prior 12 months, and 46.1% over the previous two years. If we examine the iShares MSCI Germany ETF (EWG), we can see that it has similar metrics, and a P/E ratio of 22.2x. This suggests the market expects outstanding earnings growth to continue well into the future.

While the weaker eurozone states haven’t benefited nearly as much as Germany, they’ve nevertheless seen significant gains. The Italian Borsa is up 22.0% in two years, with the iShares MSCI Italy ETF (EWI) priced at 29 times earnings. Euronext Paris is up 25.2% and the iShares MSCI France ETF (EWQ) sells at a 23x P/E ratio. Spain (EWP) has seen the most modest gains with the Bolsa de Madrid up 13.9% in the past year.

(click to enlarge) With the exception of Germany, you can see that most of the stock market gains are more muted than returns here in the US (SPY) over the past two years. Nevertheless, these are impressive returns given the low growth environment.

With the exception of Germany, you can see that most of the stock market gains are more muted than returns here in the US (SPY) over the past two years. Nevertheless, these are impressive returns given the low growth environment.

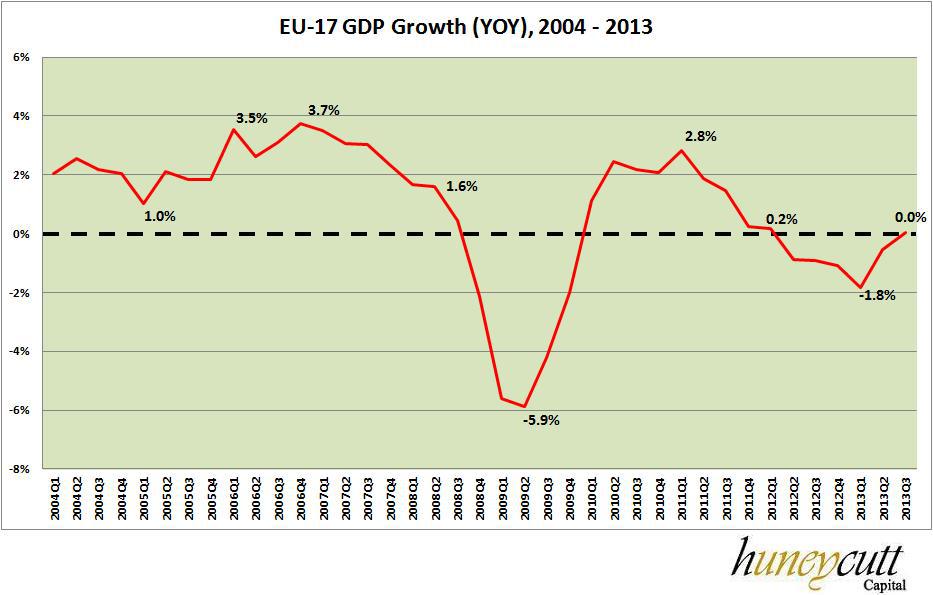

The gains seem to be fueled by a rapid decline in the trade deficits in the troubled nations. While the Eurozone is hardly back to impressive growth stage, the recession at least has appeared to be subsiding over the past few quarters. Looking at the broad Eurozone [“EU-17”], GDP growth was back to 0.0% by Q3 2013.

(click to enlarge)

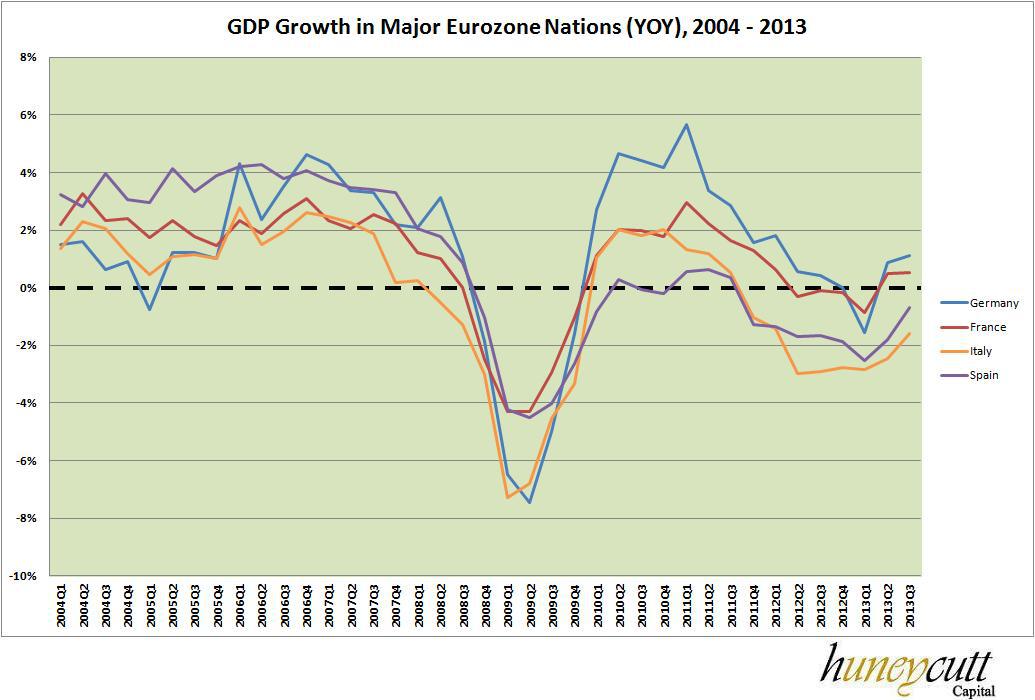

On a nation specific level, Q3 GDP was up 1.1% in Germany and 0.5% in France. GDP growth contracted 0.7% for Spain and 1.6% for Italy.

(click to enlarge)

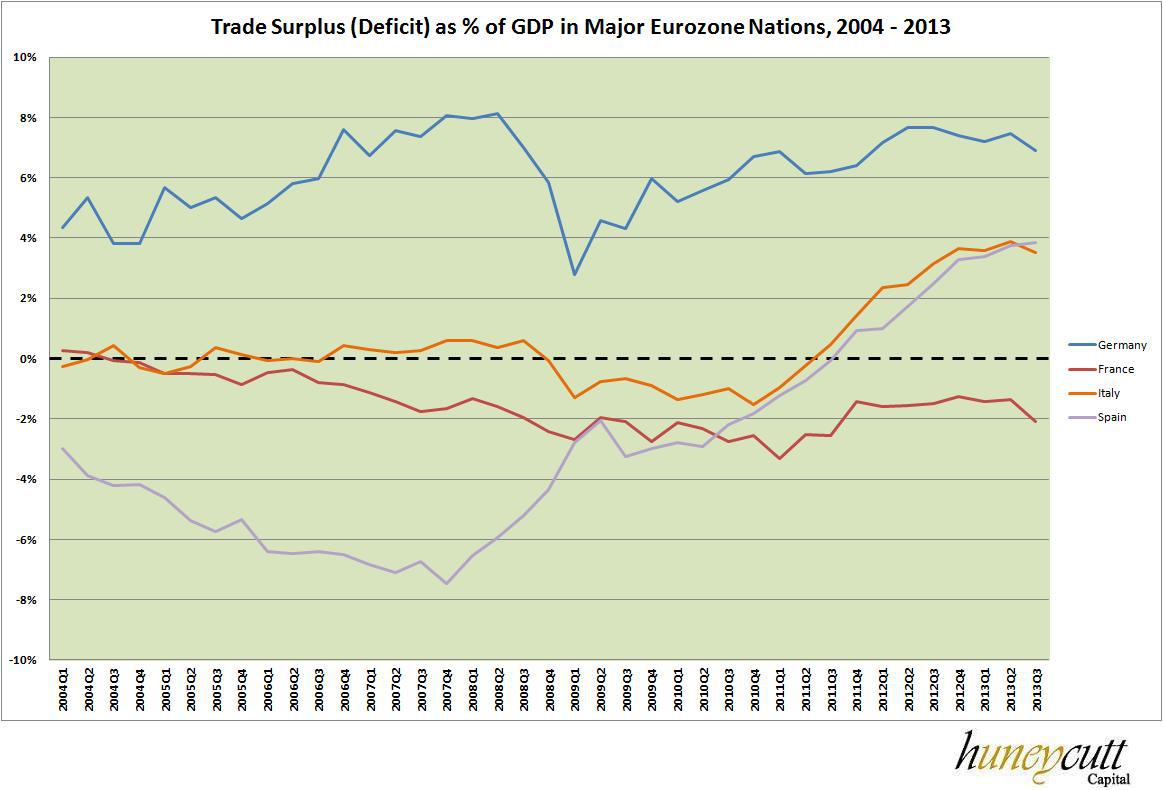

The most notable change has been in trade deficits across the Eurozone. Most prominently, Spain and Italy’s large trade deficits have shifted to large trade surpluses. This seems like good news on the face of it, but one needs to dig a bit deeper to understand the trends.

(click to enlarge)

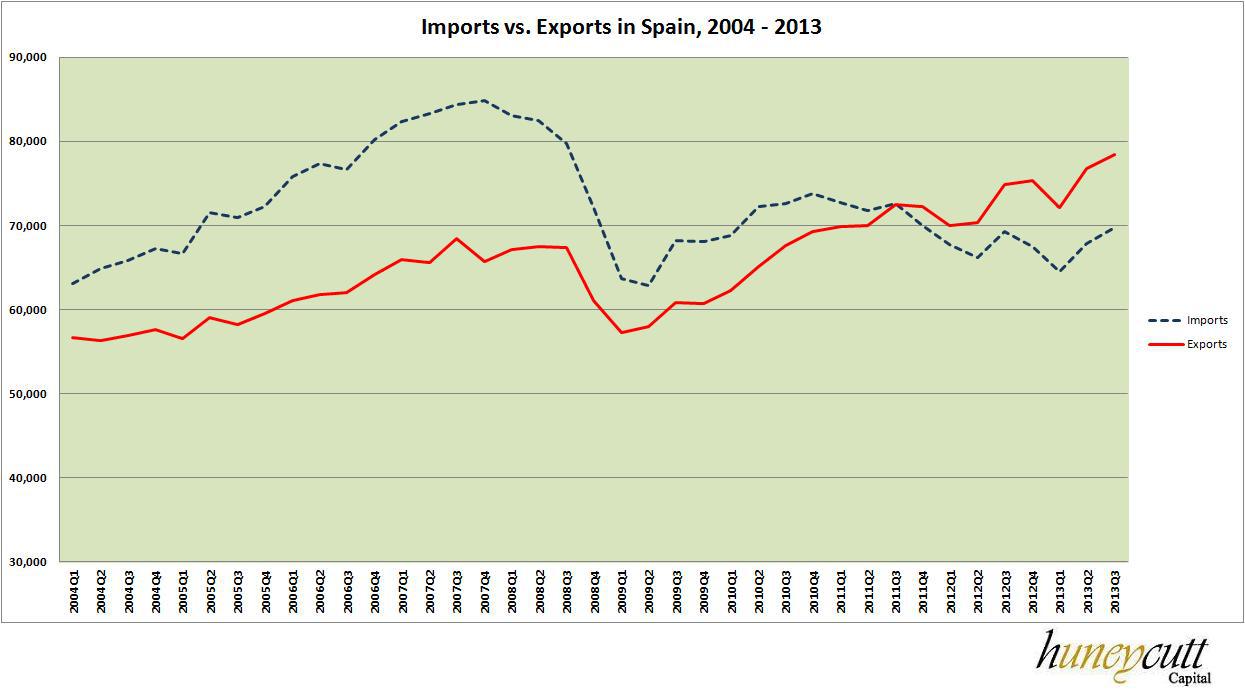

In the case of Spain, there is some good news. While imports have fallen by about 4% over the past eight quarters, exports have risen 8%. This is still somewhat of a mixed bag, but it’s at least good news that the exports have been rising, faster than imports have been falling.

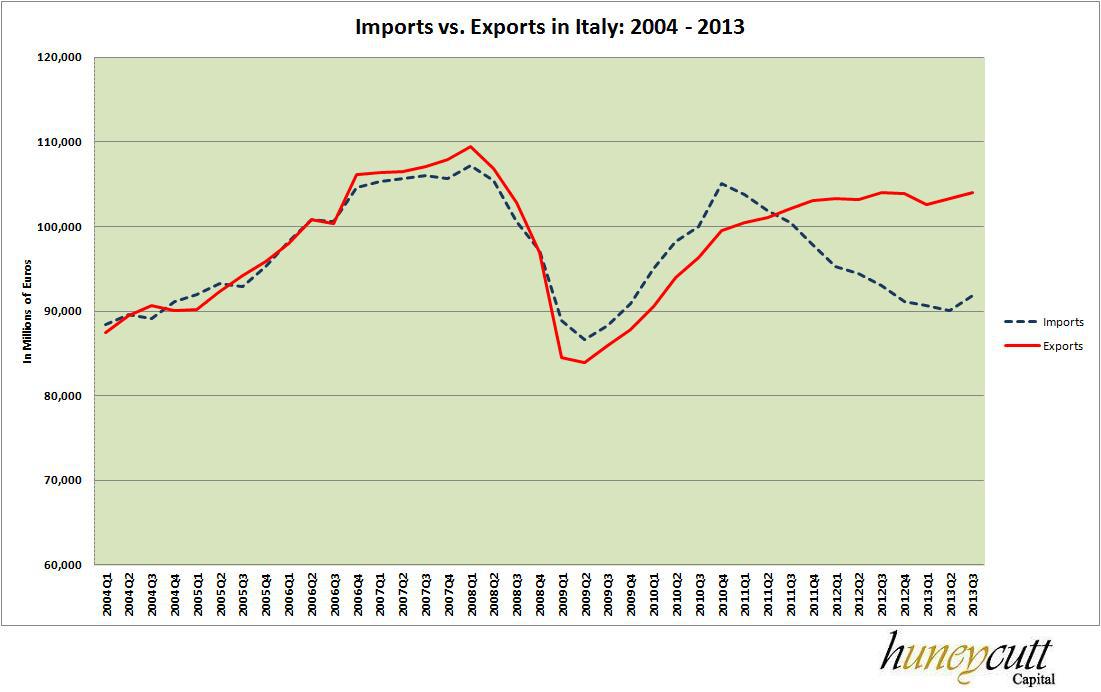

(click to enlarge) Italy on the other hand, is an outright disaster. As it turns out, Italy’s amazing shrinking trade deficit is mostly the result of imports plunging, rather than exports growing. Over the past two years, imports have fallen by 8.6%, while exports have grown a paltry 1.7%.

Italy on the other hand, is an outright disaster. As it turns out, Italy’s amazing shrinking trade deficit is mostly the result of imports plunging, rather than exports growing. Over the past two years, imports have fallen by 8.6%, while exports have grown a paltry 1.7%.

(click to enlarge)

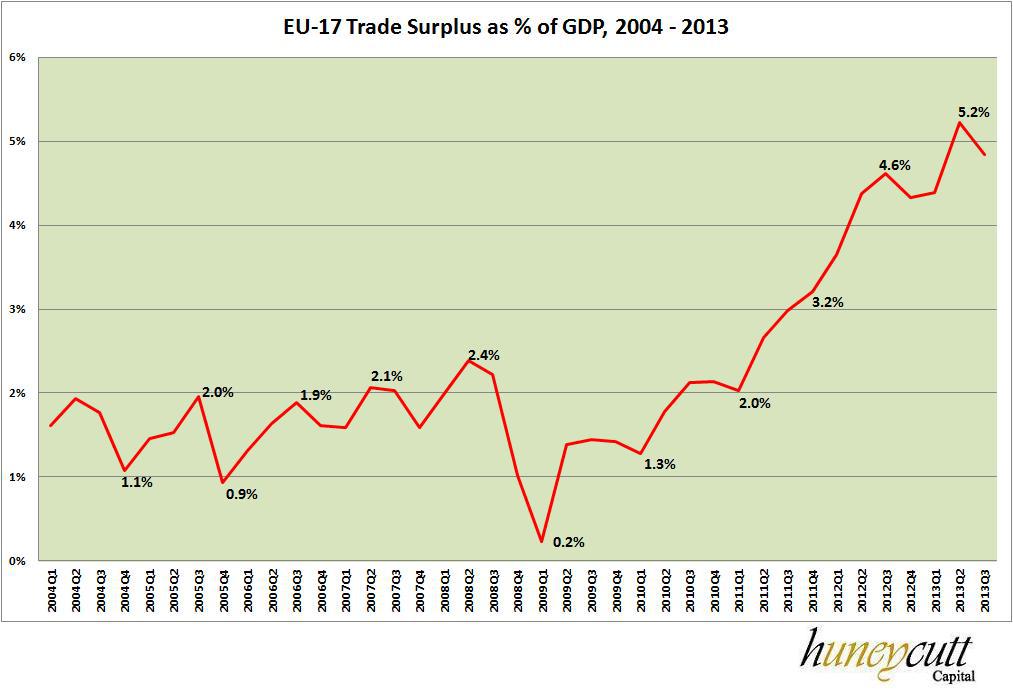

We start to see even deeper problems when we examine the Eurozone-wide [“EU-17”] balance of trade. The shift to stability over the past few years seems to neatly coincide with a skyrocketing trade surplus, which may suggest flawed policies are fueling an artificial recovery. As we’ve seen, even with this massive surplus, the “recovery” (at 0.0% GDP growth as of Q3 2013) is not very impressive either. If this is what Eurozone growth looks like with a 5% trade surplus, imagine what it would look like with balanced trade.

(click to enlarge) All in all, the “improving situation” in the Eurozone is worse than meets the eye and no country (aside from perhaps Greece) looks uglier than Italy.

All in all, the “improving situation” in the Eurozone is worse than meets the eye and no country (aside from perhaps Greece) looks uglier than Italy.

The Italian Fiscal Crisis

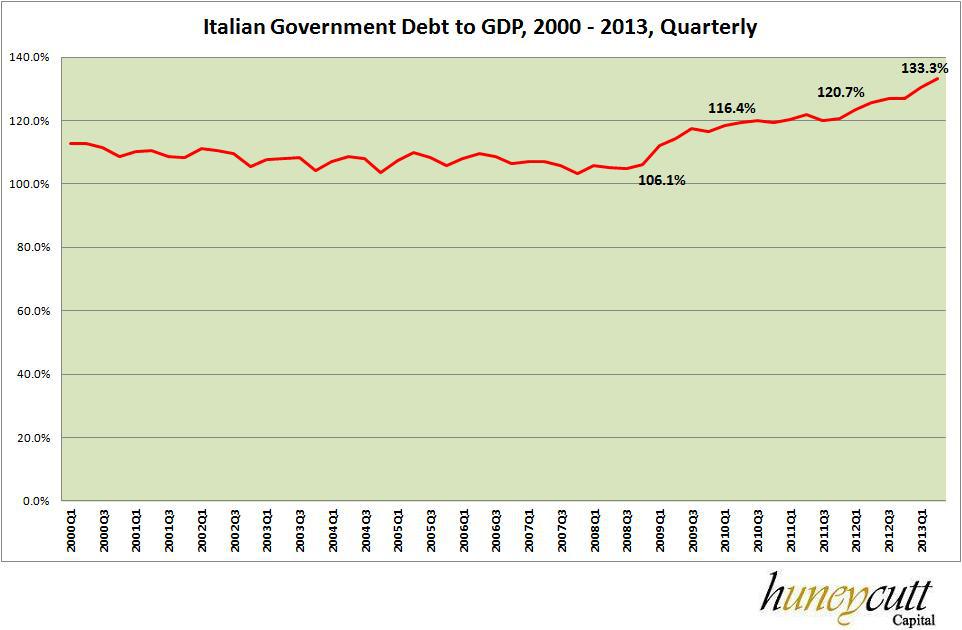

At the end of 2008, Italy’s debt to GDP ratio was 106%. As of Q2 2013, that number had jumped to 133%.

(click to enlarge) On the face of it, this seems comparable to the United States, which has a debt of about 100% of GDP, but the obvious difference is that the US is a sovereign issuer of its own currency, whereas Italy is not. I’ve argued in the past that the US debt, in some ways, is more similar to equity. When the US runs large budget deficits, it results in inflation, which is similar to equity dilution.

On the face of it, this seems comparable to the United States, which has a debt of about 100% of GDP, but the obvious difference is that the US is a sovereign issuer of its own currency, whereas Italy is not. I’ve argued in the past that the US debt, in some ways, is more similar to equity. When the US runs large budget deficits, it results in inflation, which is similar to equity dilution.

The same cannot be said for Italy. When Italy runs a budget deficit, it is essentially attempting to create growth today, and the expense of growth tomorrow. This is quite a depressing thought once you realize how terrible Italy’s growth has been over the past several decades (we’ll get to that in the next section).

The other key difference between Italy and the US is that Italy can default on its debt. While the US could technically default as well, it’s unlikely since Congress would have to intentionally decide to do so. Italy, on the other hand, may be faced with a decision of either defaulting or exiting the eurozone, returning to the lira, and devaluing.

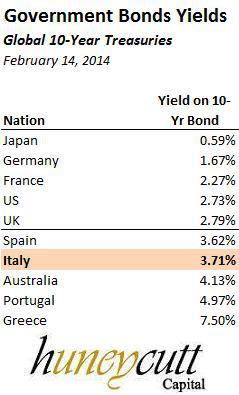

In spite of Italy’s rising debt load, interest rates on Italian debt have fallen significantly in the past two years, with the yield on the 10-year bond dropping from over 7% in late 2011, down to 3.71% currently. Contrast this with the US 10-year yield at 2.73%.

The bond yields are completely shocking to me. Not only does the Italian 10-year bond yield only 98 bps more than the US 10-year, but the French 10-year bond is actually priced with a yield 46 bps less than the US 10-year. This is particularly insane when you start to consider default risks, where the US has virtually none, and both Italian and French bonds have significant risks.

It’s almost as if investors are doing a straightforward compare-and-contrast, rather than recognizing that eurozone bonds and the US treasuries are radically different investment products. Of course, as we’ll soon see, the surge in eurozone bonds has more to do with ECB intervention into the markets, rather than private investors bidding prices up based on fundamentals.

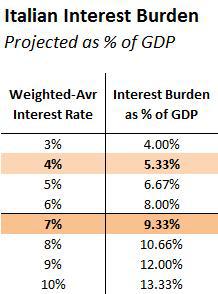

Let’s step back a moment, however, and contemplate how the Italian interest burden may be shifting. The chart below examines Italian interest burden as a percentage of GDP, assuming a leveling off of Italian debt (i.e. a steady-state of 133% debt to GDP).

As you can see, there’s a pretty huge difference between a weighted-average interest rate of 4% and 7%, with the former producing interest payments at 5.33% of GDP, and the latter at 9.33%. Undoubtedly, this was what the ECB was concerned about when they launched the Long-Term Refinancing Operation. While the LTRO was a success in reducing Italy’s interest burden (at least in the near term), unfortunately, it doesn’t solve the myriad other problems driving the crisis. Nor, as we’ll soon see, is it likely to keep the bond vigilantes at bay forever.

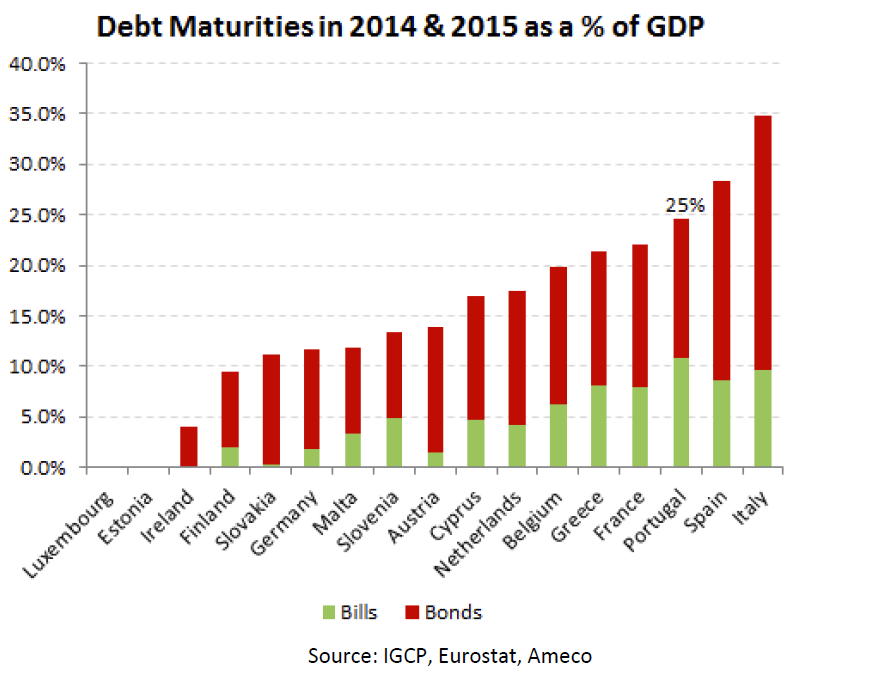

Indeed, in spite of the near-term improvements on interest outlook, Italy is far from out of the woods. Italian debt maturities are equal to about 35% of GDP for the next two years; higher than any other eurozone nation.

(click to enlarge)

For what it’s worth, Italy has taken some privatization measures to try to lower debt, but to call these measures “small and virtually insignificant” would be a dramatic understatement. For instance, in January, Italy moved to sell 40% of its stake in the Italian postal service (Poste Italiane). The sale is expected to bring in somewhere from $5.5 – $6.5 billion. In comparison, Italy’s debt load is about $2.68 trillion; this means the partial postal privatization will reduce Italy’s debt by about 0.2%.

The Italian Growth Crisis

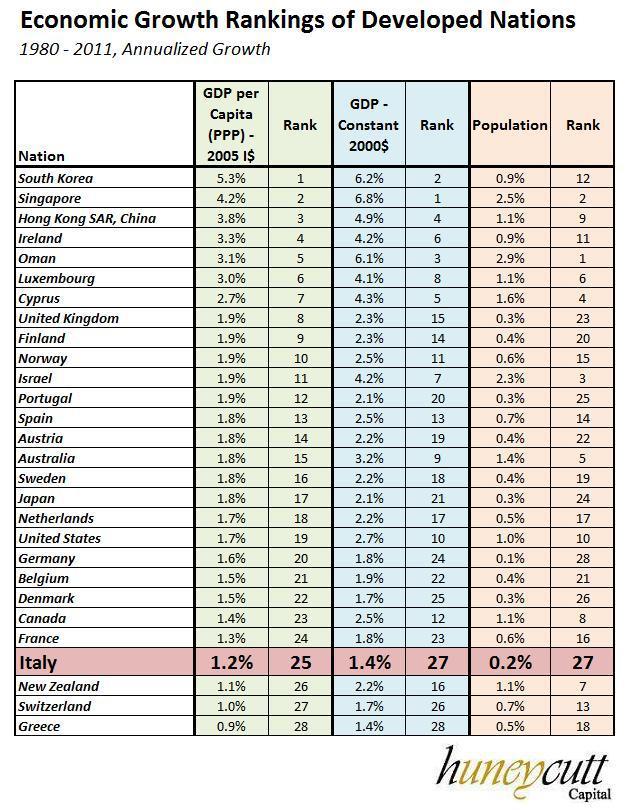

While we’ve examined some of Italy’s fiscal problems and the trade imbalances created by the Euro, what makes Italy a particularly strong candidate to ignite a broader crisis are growth struggles. From 1980 to 2011, Italy had the second worst GDP growth rate amongst developed nations at 1.4% annually; only Greece fared (ever-so-slightly) more poorly.

Likewise, per capita income growth was ranked 25th out of 28th. Even that is a bit misleading, because two of the nations below Italy (Switzerland and New Zealand) had significantly higher population growth rates (immigration tends to depress per capita income growth).

Likewise, per capita income growth was ranked 25th out of 28th. Even that is a bit misleading, because two of the nations below Italy (Switzerland and New Zealand) had significantly higher population growth rates (immigration tends to depress per capita income growth).

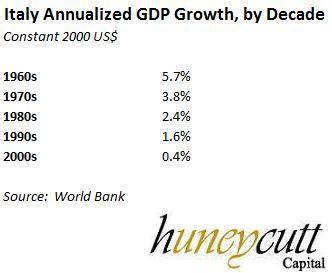

The numbers only get worse when we analyze them in further detail. If we view Italy’s GDP growth by decade, we see a rather marked downward trend. Italy experienced significant growth in the 60s and 70s. By the 1980s, it has more modest 2.4% annual GDP growth. That fell to 1.6% in the booming 90s and 0.4% in the last decade.

Thus far in the 2010s, things are looking even worse. Italy’s GDP has fallen 7.3% over the past five years, suggesting that Italy could potentially be in negative territory for the 2010s. It’s bad enough that a recent Wall Street Journal headline exclaimed, “Italian Economy Stops Contracting,” almost as if that were a cause worth celebrating. Unfortunately, Italy needs more than 0% or 1% long-term growth to get out of the woods.

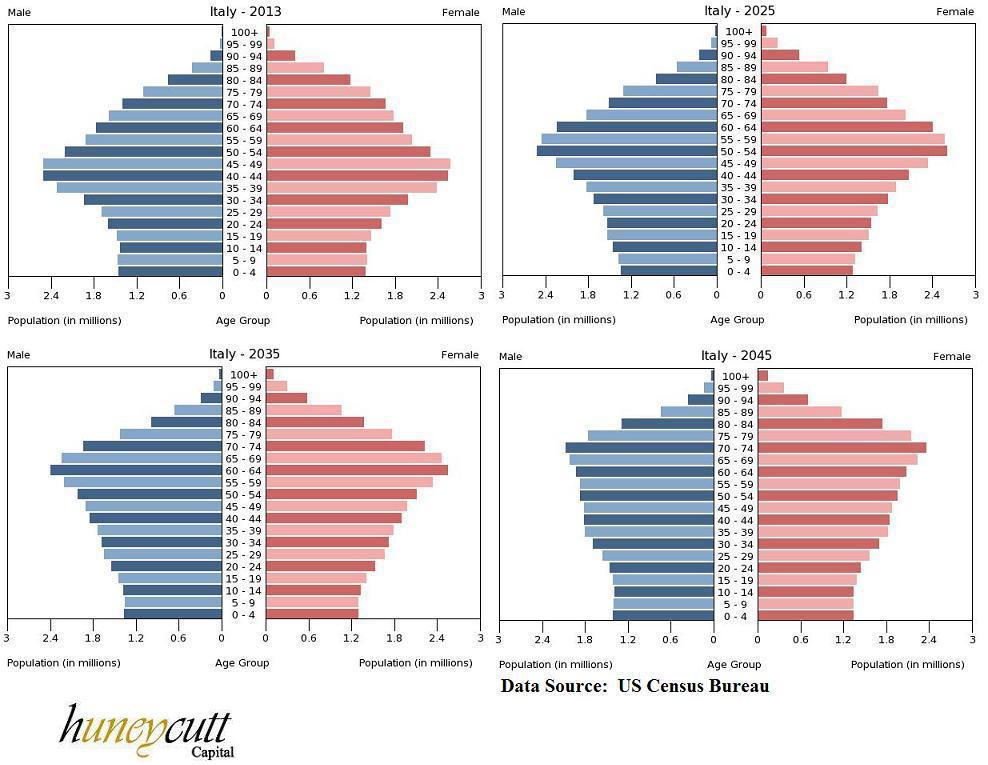

Italy’s demographics make future growth an even trickier proposition. Italy has the 2nd lowest population growth rate amongst developed nations. It has, quite possibly, the ugliest population “pyramid” in the developed world, as well. Indeed, it doesn’t look much like a “pyramid” all; it more closely resembles a spinning top or perhaps the upper half of the Seattle Center (famously known for its space needle!)

(click to enlarge) If you’re a young Italian examining this, the most obvious conclusion is that you are likely to be taxed exorbitantly in order to pay for the past promises by the Italian state. Naturally, this will lead many young Italians to leave for greener pastures, further exacerbating the problems. I’m not sure if there’s a formal name for this, but perhaps “demographic death spiral” is apt; very similar to what has happened in Detroit, only on a much grander scale.

If you’re a young Italian examining this, the most obvious conclusion is that you are likely to be taxed exorbitantly in order to pay for the past promises by the Italian state. Naturally, this will lead many young Italians to leave for greener pastures, further exacerbating the problems. I’m not sure if there’s a formal name for this, but perhaps “demographic death spiral” is apt; very similar to what has happened in Detroit, only on a much grander scale.

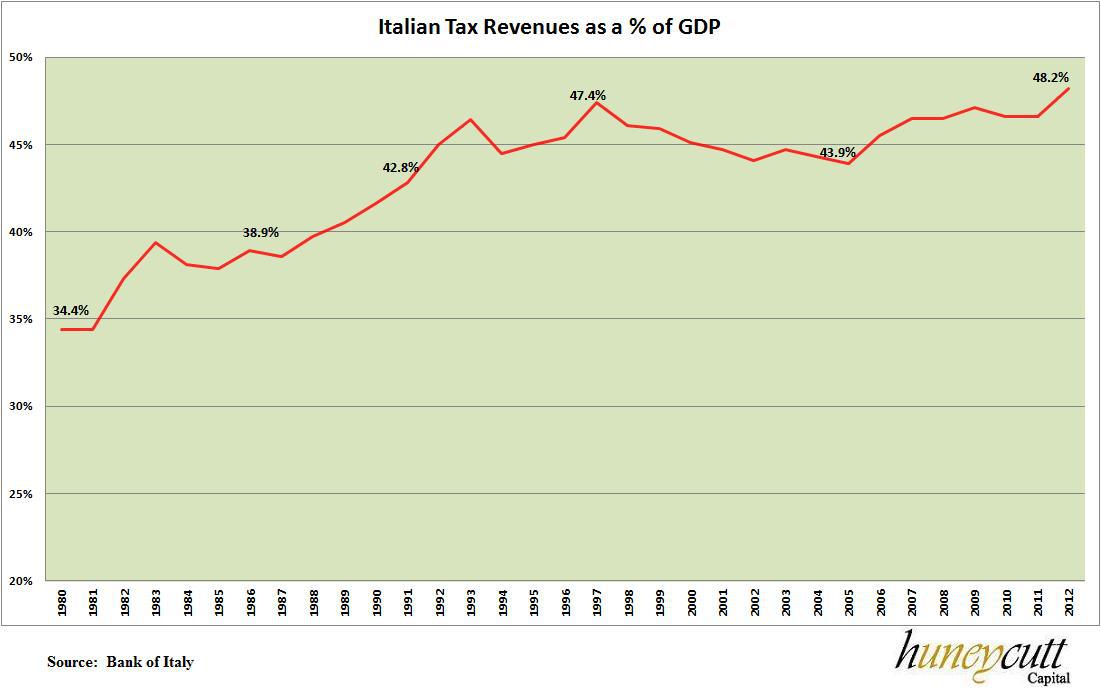

The Italian tax burden has increased significantly already over the past few decades. In 1980, total Italian tax revenues as a percentage of GDP amounted to 34.4% of GDP, based on data from the Bank of Italy. By 2012, that number had shot up to 48.2% of GDP.

(click to enlarge) Even this is underestimated based on recent research from Confcommercio, a federation representing small and medium sized companies in Italy. The Italian underground economy now accounts for about 17.5% of GDP, the highest in the world. Confcommercio’s research shows that once you factor in the underground economy, the true tax burden in the “legal economy” (i.e. for those that pay taxes) is closer to 55% of GDP; the highest in the world.

Even this is underestimated based on recent research from Confcommercio, a federation representing small and medium sized companies in Italy. The Italian underground economy now accounts for about 17.5% of GDP, the highest in the world. Confcommercio’s research shows that once you factor in the underground economy, the true tax burden in the “legal economy” (i.e. for those that pay taxes) is closer to 55% of GDP; the highest in the world.

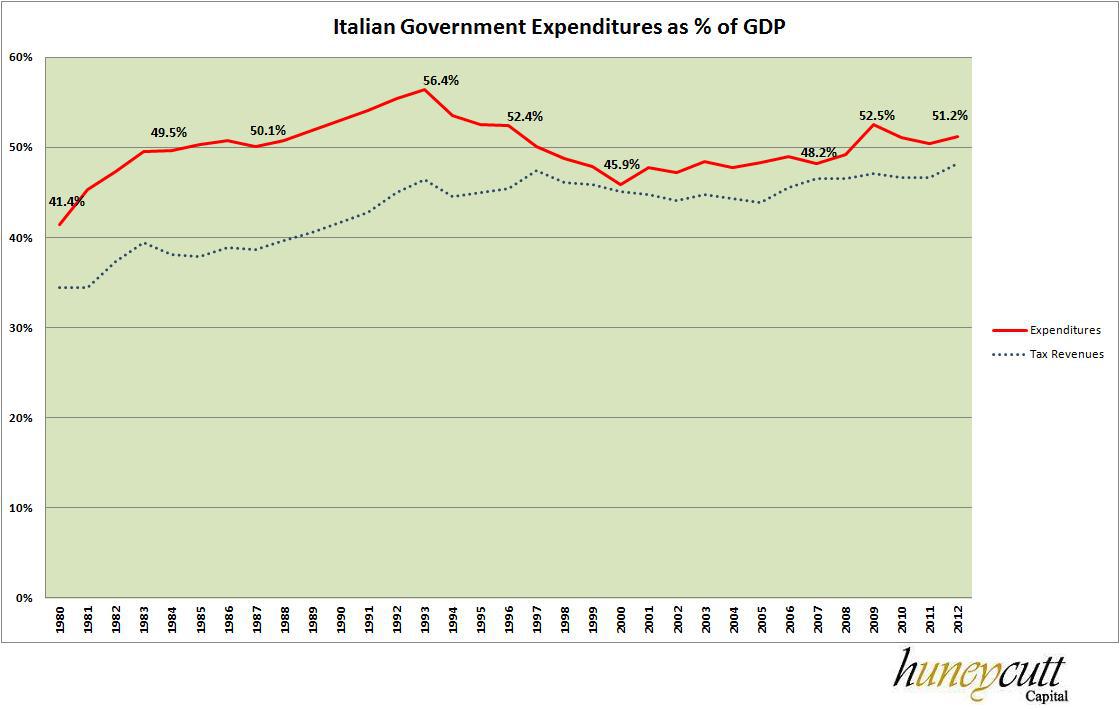

Government expenditures have also been stubbornly high in Italy. In 1980, total Italian expenditures accounted for 41.4% of GDP (creating a 7% budget deficit). Expenditures peaked at 56.4% of GDP in 1993, before falling down to 45.9% in 2000, and then pushing back above 50% from 2009 onwards.

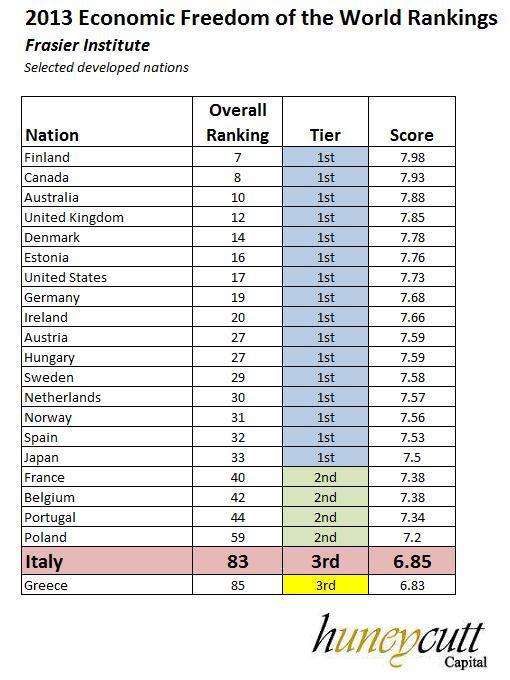

(click to enlarge) Italy’s structural problems are likewise significant. The Canadian-based Fraser Institute compiles an “Economic Freedom of the World” index every year, which is a good proxy for the health of a nation’s economic model. While ratings are always a bit subjective, Italy is well below nearly every other developed nation (aside from Greece.) For 2013, Italy ranked #83, one spot ahead of Kazakhstan, and in the same tier as Russia and China.

Italy’s structural problems are likewise significant. The Canadian-based Fraser Institute compiles an “Economic Freedom of the World” index every year, which is a good proxy for the health of a nation’s economic model. While ratings are always a bit subjective, Italy is well below nearly every other developed nation (aside from Greece.) For 2013, Italy ranked #83, one spot ahead of Kazakhstan, and in the same tier as Russia and China.

Italy didn’t fare much better in the Heritage Foundation / Wall Street Journal rankings, which placed it at #86, one spot below the Kyrgyz Republic; a former part of the Soviet Union. Most notable in that survey was Italy’s 38.5 score (out of 100) in the “freedom from corruption” category. In a sense, Italy has become a first world nation with a third world economy.

Taking all of this data as a whole, it paints a very grim picture for Italy’s economic future, without major reforms. The demographic troubles mean that expenditures are almost certain to increase (as a % of GDP) in future years, without intervention. Italy may already have the highest tax burden in the world, so raising taxes is a poor option. This hasn’t stopped Deutsche Bundesbank from floating the idea of a “wealth tax”; a terrible scheme mostly meant to benefit the German banks with significant exposure to Italian debt. In reality, for the Italian nation (as opposed to the German banks) to have any chance at significant future growth, it needs to streamline the tax system and significantly reduce the overall tax burden. Otherwise, the exodus outward will continue, further exacerbating its debt issues.

Major reforms are likewise needed to reduce spending in Italy, but it’s probable that any such reforms would be immensely unpopular. Italy’s corruption and large underground economy pose significant hurdles to escaping the current crisis, as well.

In sum, Italy is Detroit on a grand scale.

The Not-So-Coincidental Surge in Italian Bond Prices

Growth is terrible, debt is sky-high, trade figures look bad, and demographics are ugly. In spite of all of this, Italian bond prices have surged upwards since late 2011, when yields peaked at over 7%. As alluded to earlier, the bull market in Italian bonds is not being driven by a fundamental improvement in anything. Rather, the ECB’s Long-Term Refinancing Operation is the primary driver. To get a better sense of this, let’s look at the world through the eyes of the major Italian banks.

Private Italian banks now hold about €387.4 billion in Italian debt holdings, or roughly 20% of the total outstanding debt. This is a significant increase from about €200 billion in early 2012 near the beginning of the LTRO.

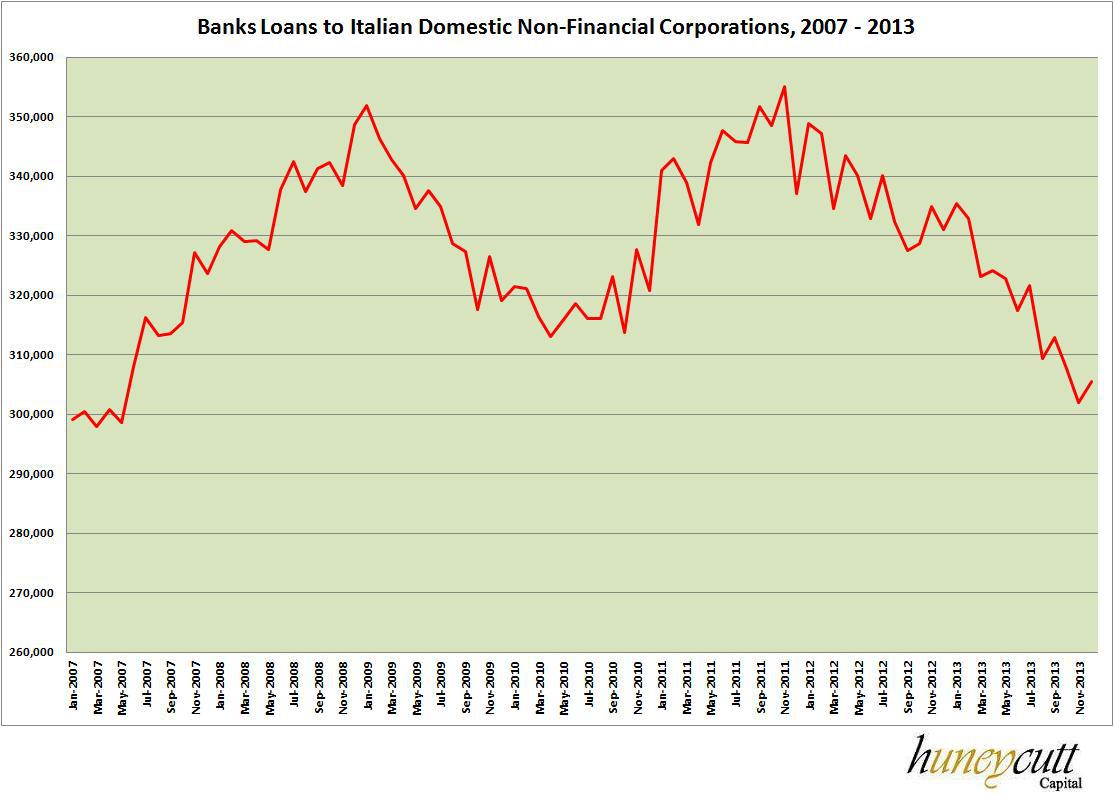

Now let’s contrast that with the decline in private loan growth. From June 2011 to December 2013, loans to Italian domestic corporations (non-financial) fell 12%.

(click to enlarge) This is likely due, in no small part, to surging bad debt in Italy. From 2010 to 2013, bad debts have grown from €59.9 billion in Jan 2010 to €155.9 billion in Dec 2013. That’s an increase of about 160%!

This is likely due, in no small part, to surging bad debt in Italy. From 2010 to 2013, bad debts have grown from €59.9 billion in Jan 2010 to €155.9 billion in Dec 2013. That’s an increase of about 160%!

(click to enlarge)

After reading about the surge in Italian debt holdings amongst the Italian banks, I decided to take a look at a few individual banks. Italy’s 3rd largest bank, Mediobanca (OTC:MDIBF)(OTCPK:MDIBY), provided some of the most detailed data I could find, so I’ll focus my efforts on it.

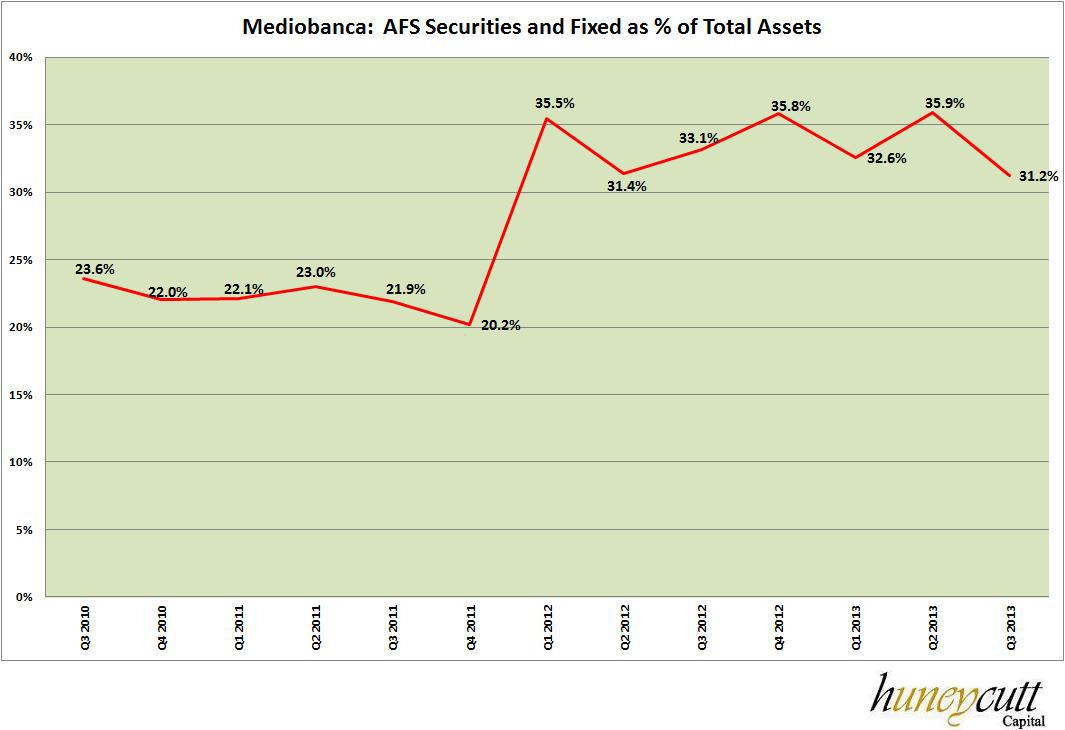

There was a surge in fixed income and available-for-sale (“AFS”) securities across all the banks I examined. Combining these two categories, Mediobanca’s AFS and Fixed Income holdings grew 85% from Q4 2011 to Q1 2012.

(click to enlarge)

Total assets have remained fairly steady since 2011, meaning that this represented a huge jump in the AFS and Fixed Income portions of Mediobanca’s balance sheet. These two categories combined for 20.2% of the balance sheet in Q4 2011 and 35.5% in Q1 2012. The figure has bounced around a bit since then, but has generally remained above 31% of total assets.

(click to enlarge)

We can also compare loan growth with the growth in AFS and fixed income securities. Total loans on the balance sheet have declined about 12% for Mediobanca.

(click to enlarge)

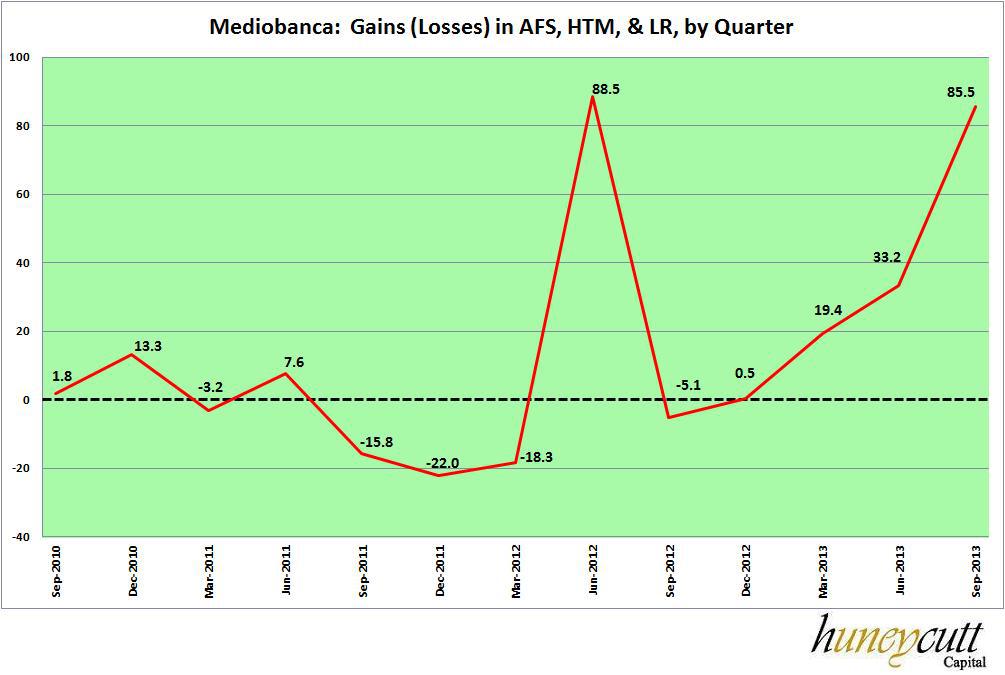

How did all of this impact the bottom line at Mediobanca? Admittedly, the profit picture was poor even with the boost from the LTRO, but around 2012, there were large gains in certain quarters, from Mediobanca’s investment portfolio, with a €88.5 million boost in the quarter ending June 30, 2012, and €85.5 million boost in the most recent quarter.

(click to enlarge) While Mediobanca was still in the red in many quarters, its losses were lessened by the LTRO program. In the most recent quarter, Mediobanca turned a €171 million profit, half of which came from the AFS, HTM, and LR portfolios.

While Mediobanca was still in the red in many quarters, its losses were lessened by the LTRO program. In the most recent quarter, Mediobanca turned a €171 million profit, half of which came from the AFS, HTM, and LR portfolios.

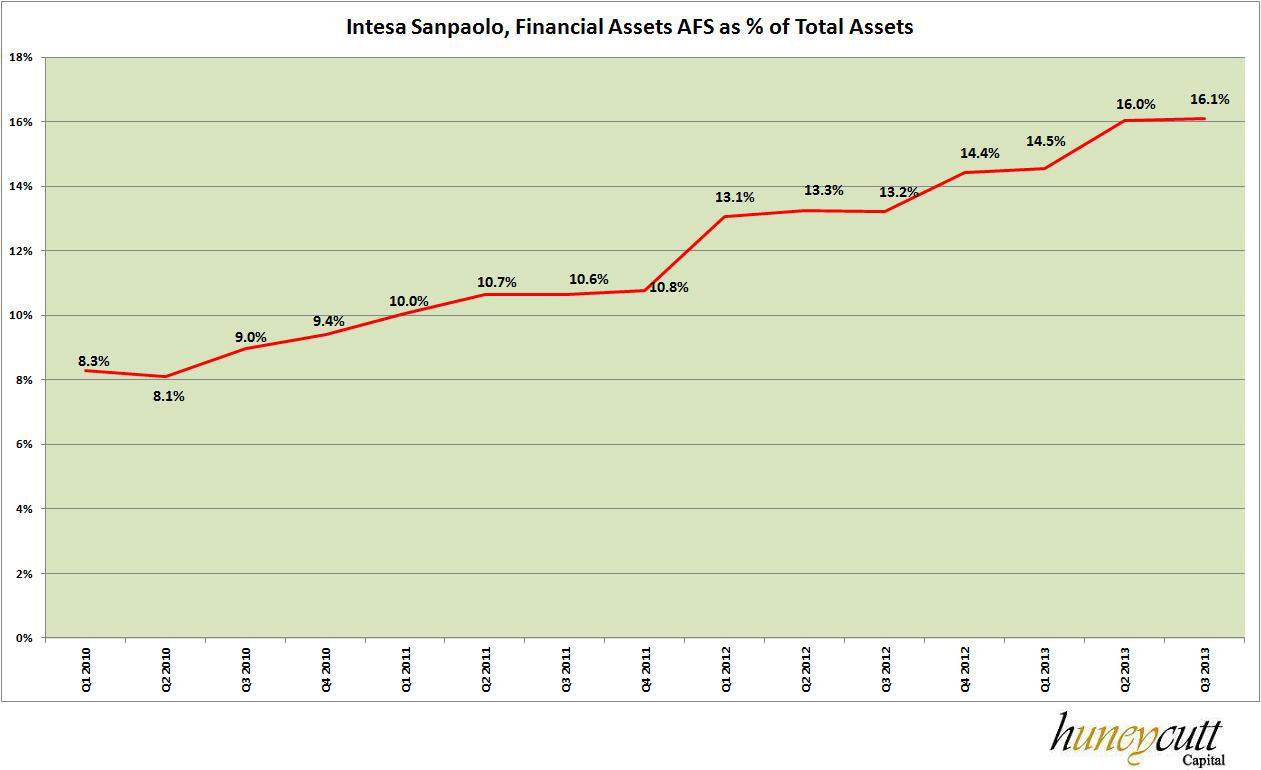

(click to enlarge) Let’s take a quick look at another bank, Intesa Sanpaolo, Italy’s 2nd largest bank (OTC:IITOF)(OTCPK:IITSF). Unlike with Mediobanca, Intesa seemed to take things a bit slower with the launch of LTRO. However, the overall trend has been the same. In Q1 2010, “Financial Assets AFS” accounted for 8.3% of Intesa’s total assets; by Q3 2013, that figure had surged to 16.1%.

Let’s take a quick look at another bank, Intesa Sanpaolo, Italy’s 2nd largest bank (OTC:IITOF)(OTCPK:IITSF). Unlike with Mediobanca, Intesa seemed to take things a bit slower with the launch of LTRO. However, the overall trend has been the same. In Q1 2010, “Financial Assets AFS” accounted for 8.3% of Intesa’s total assets; by Q3 2013, that figure had surged to 16.1%.

(click to enlarge) As with Mediobanca, loans have also declined, falling about 8% over the past two years.

As with Mediobanca, loans have also declined, falling about 8% over the past two years.

(click to enlarge) Unfortunately, it was more difficult to determine how much of Intesa’s profits can be attributed to the LTRO program. However, there was a surge in “profits from trading” in Intesa’s income statement. In FY 2010 and 2011, Intesa recorded a €243 million profit and €204 million loss respectively. Comparatively, for the first three quarters of 2012 and 2013, Intesa recorded trading profits of $1.5 billion and $1.1 billion; a very significant jump.

Unfortunately, it was more difficult to determine how much of Intesa’s profits can be attributed to the LTRO program. However, there was a surge in “profits from trading” in Intesa’s income statement. In FY 2010 and 2011, Intesa recorded a €243 million profit and €204 million loss respectively. Comparatively, for the first three quarters of 2012 and 2013, Intesa recorded trading profits of $1.5 billion and $1.1 billion; a very significant jump.

The trading profits constituted 88.9% of Intesa’s profitability for the 1st three quarters of 2012. For FY ’13, the trading profit of $1.1 billion is larger than Intesa’s overall profit of $640 million. This suggests that, as with Mediobanca, the LTRO program has been a significant contributor to Intesa’s profitability in the past two years.

The question now becomes, what happens as the Italian banks are required to repay their LTR obligations in 2015? At the very least, the banks will lose a source of easy profitability over the past two years. At worst, Italian bond yields could begin to creep back upwards and represent a significant headwind.

Investment Ramifications

The markets continue to adopt a shallow examination of eurozone economies, pushing stock prices upwards. While some optimism in regards to a Spanish recovery may be warranted, the situation in Italy continues to get uglier in spite of the improving stock market. One should be very cautious about investing in the eurozone; nevertheless, there might be some great deals to be found in places like Spain or amongst large multi-nationals.

The absolute worst investment in the world right now might be Italian government bonds (ITLY)(ITLT). With a yield that is now within 100 bps of significantly less risky US bonds, it seems absolutely insane to buy in. A pair trade going long on US 10-year treasuries (TLH) and going short on Italian bonds would be a good way to take advantage of this disparity. The primary risk, in my view, would be that the yields on US bonds increase, but over the long term, it’s difficult to imagine that the current pricing of US treasuries vs. Italian government bonds makes sense.

Moreover, with the LTRO coming to an end in 2015, it’s completely possible that the Italian banks began to sell off some of their sovereign debt holdings, pushing bond prices back downward. Then again, with private lending falling, perhaps they’d still prefer to hold the debt. Either way, it’s obvious that Italian banks hoarding Italian debt has not solved much of anything. It has simply created a greater likelihood of a future banking crisis in Italy.

Without significant structural reforms to the Italian economy or a eurozone exit, Italian equities do not look much better than Italian debt. There’s immense pressure from the German banks to impose even more harsh tax increases on the Italian public; likely further sapping long-term growth, and exacerbating the crisis.

Due to its significant size and eurozone bank exposure to Italian debt, it’s simple enough to see how an Italian debt scare could re-ignite the eurozone crisis. For this reason (and many others, as well), I’d view many other eurozone nation equities as very risky, as well. With an 8% trade surplus and what appears to be an asset bubble, the German economy may be more vulnerable than believed in the event that Italian problems flare up again.

That said, if one were to invest in the eurozone, the best places to look might be large multi-nationals that do a significant amount of business outside Europe. Likewise, while I still have some reservations about Spain, the Spanish economy certainly has a stronger structural foundation than Italy, and many big investors have started to look at Spanish assets and equities. If you’re into distressed investing, Spain is likely a much better place to search than Italy.

Conclusions

Italy is one of the eurozone’s weakest links and its sheer size has the potential to ignite a much broader eurozone crisis. The Italian economy accounts for about 16.5% of eurozone GDP and is the fourth largest economy in all of Europe (trailing only Germany, UK, and France). Compare that to Greece, which only accounts for 2.3% of eurozone GDP, or Cyprus at a paltry 0.2%, and it becomes obvious why an Italian economic crisis could be like lighting a giant “powder keg” that impacts the entire eurozone.

There’s a strong likelihood that Italy exits the eurozone within the next decade without significant reforms to the eurozone and / or the ECB. With fewer and fewer young taxpayers to support the Italian state’s obligations, and an uncompetitive labor market (partly due to the Euro), Italy needs something better than a zero-growth economy to service its growing debt burden. It needs significant structural reforms and an escape from the Euro’s stifling impact on the Italian labor market.

Italian bonds are one of the worst long-term investments in the world in 2014, now priced with yields lower than in 2009, prior to the onset of Greek debt crisis. Indeed, eurozone bonds in general seemed to be priced with an ignorance of risk, with US treasuries yielding more than French government debt. US bond also look very attractive on a risk-adjusted basis when compared to Italian treasuries.

Overall, Italy has the potential to create another eurozone-wide crisis, or even become a significant drag on the global economy. Still largely being ignored by many investors, Italy’s problems should be considered one of the greatest risk factors for the world economy in 2014 and beyond.

Some Other Readings

I recommend the similarly-themed Shareholders’ Unite article, “The Ticking Time Bomb Under the World Economy,” which provides an excellent analysis of many of Italy’s problems. Spiegel’s 2012 article, “Italy’s Lost Generation” is a good read on outward migration by young Italians.

{kind=link}

1 comments

BrianArthurFinn

2015-03-26 at 18:55 (UTC 2) Link to this comment

Ha wow this kid Jake is an idiot – this guy totally schooled him.