George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

We examine how long the U.S. Dollar will remain the unique world reserve currency. The most important criterion for being a reserve currency is wealth. While China has recently overtaken the U.S. as for GDP, in the next 10 years it will overtake the U.S. as for wealth.

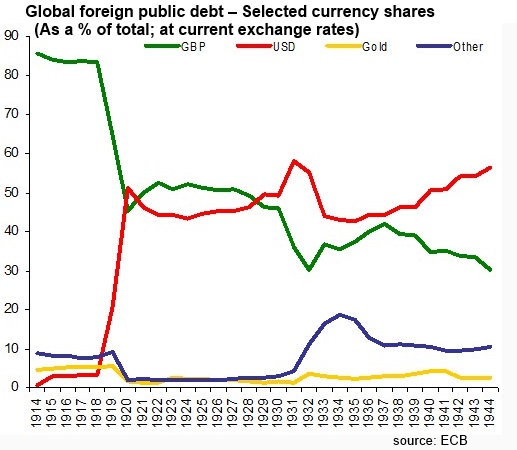

After WWI the British pound lost its status as world reserve currency, the United States became by far the richest nation in the world as for wealth. In the graph a ECB researcher shows how with the ending WWI a big part of the world’s public debt for foreign bond holders got denominated in dollar. Until the start of the war, 86% of global foreign debt was still in British pound.

After WWI the British pound lost its status as world reserve currency, the United States became by far the richest nation in the world as for wealth. In the graph a ECB researcher shows how with the ending WWI a big part of the world’s public debt for foreign bond holders got denominated in dollar. Until the start of the war, 86% of global foreign debt was still in British pound.

The U.S. Dollar became the major and nearly unique world reserve currency. With the abolishment of the gold standard in the early 1930s and the creation of the dollar-centric Bretton Woods system in 1945, its status became even more important.

To know how long the dollar will remain the major world reserve currency, one important criterion to look at is wealth and to see how long the United States remains the richest nation in the world. The best indicator is the world bank’s gross savings rate. Gross savings is the gross national income minus consumption + transfer payments like pensions. Accumulated savings over years give wealth. China has a gross savings rate of 51% of GDP and the U.S. has one of 17%, while for comparison Germany is 24% and the rest of the euro zone is around 19%. These values have been pretty stable for China and Germany for years. Since the 2008 crisis, Americans are saving a bit more.

US household net worth 1952-2012 - Click to enlarge

Wealth consists of assets, either in the form of fixed (machines, homes, state investments, infrastructure) or financial investments, either the ones of the private sector or the ones of the state, like state pensions.

Recently China’s GDP has achieved the same level as U.S. GDP as for purchasing power (things are cheaper in China); but on the other side, China’s GDP is rising far more quickly.

We ignore these subtleties and assume that:

China GDP = US GDP

Chinese wealth increases each year by 34% of US GDP more than US wealth. These 34% of GDP are about 40% of US disposable income. Disposable income is typically a bit less than GDP due to depreciation and tax.

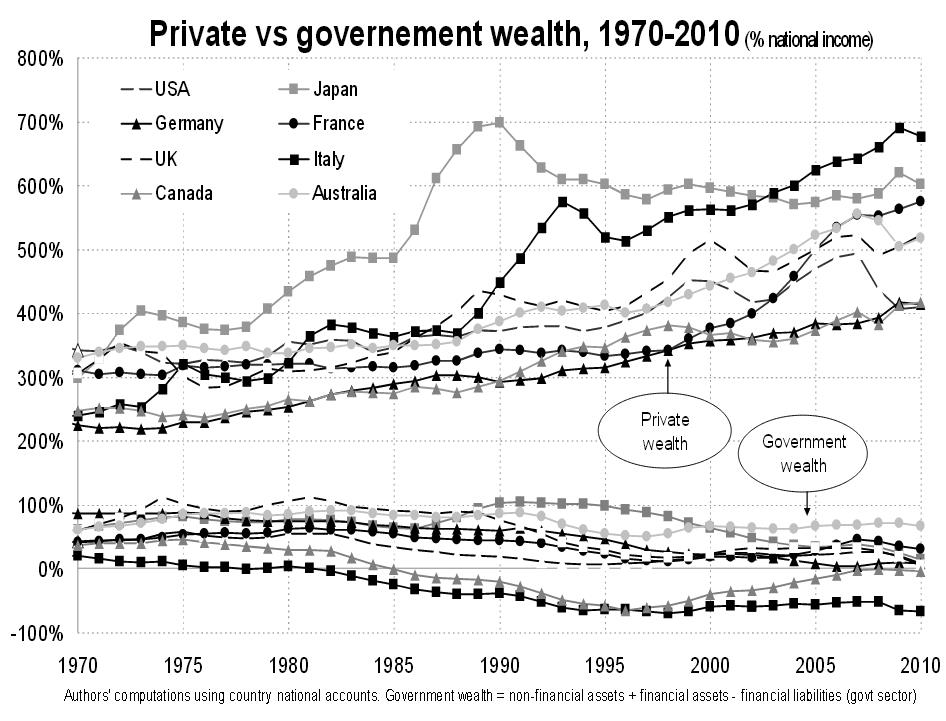

click on image to expand , source Prof. Picketty, University of Paris

Currently, US private net wealth is about 500% or 550% of disposable income, depending on stock market and home price fluctuations (and the Fed). This number does not include wealth in the form of state investments and infrastructure.

But Piketty shows that for the public sector:

Net wealth = investment + infrastructure minus debt and for Western states it is around zero

China had a very weak GDP and low wealth when it started the recovery against the US in the 1990s; therefore, it makes sense to say that Chinese wealth is currently around 200% of US GDP.

Hence it appears that in less than ten years time, China will have overtaken the U.S. not only as for GDP but also for wealth.

Still important things like convertibility of the Yuan and a big choice of investment vehicles are missing in China, but this could be achieved in the following ten years.

In the following paper, Eichengreen, Chitu and Mehl show that “financial deepening” and wealth is the most important driver of a reserve currency.

Chiţu, L, B Eichengreen and A Mehl, “When Did the US Dollar Overtake Sterling as the Leading International Currency? Evidence from the Bond Markets”, Journal of Development Economics, forthcoming and VoxEU, Online Link

Read also:

The following post also examines different criteria than wealth: When Will the Renminbi Become a Reserve Currency?

B. Eichengreen, Mehl, A., Chitu, L: “One or multiple international currencies? Evidence from the history of the oil market”, VoxEU, Online link