Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Drivers for the Week Ahead

Drivers for the Week Ahead2 Sep 2019

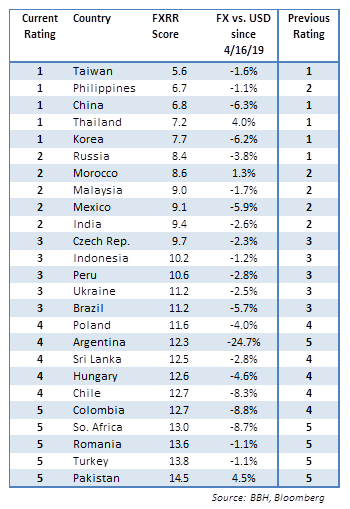

Emerging Markets: FX Model for Q3 2019

Emerging Markets: FX Model for Q3 201928 Aug 2019

Dollar Firm as Markets Calm

Dollar Firm as Markets Calm27 Aug 2019

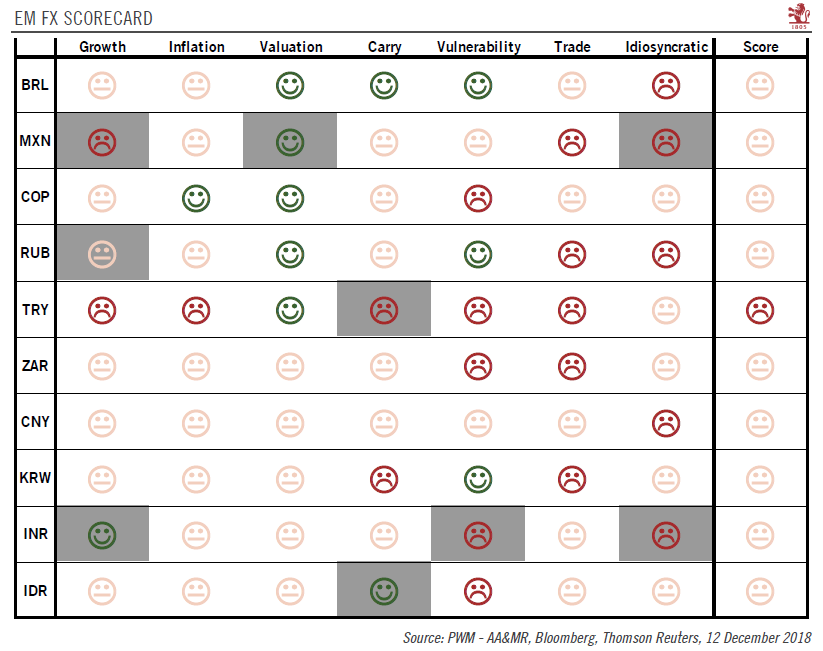

Emerging market currencies: idiosyncratic risks strike back

Emerging market currencies: idiosyncratic risks strike back15 Dec 2018

House View, December 2018

House View, December 20186 Dec 2018

Emerging Markets: Preview of the Week Ahead

Emerging Markets: Preview of the Week Ahead17 Sep 2018

Emerging Markets: What has Changed

Emerging Markets: What has Changed10 Sep 2018

Emerging Market Week Ahead Preview

Emerging Market Week Ahead Preview4 Sep 2018

Emerging Markets: What Changed

Emerging Markets: What Changed3 Sep 2018

Emerging Markets: Week Ahead Preview

Emerging Markets: Week Ahead Preview27 Aug 2018

Emerging Markets: Preview of the Week Ahead

Emerging Markets: Preview of the Week Ahead20 Aug 2018

Emerging Markets: Preview of the Week Ahead

Emerging Markets: Preview of the Week Ahead6 Aug 2018

Emerging Markets: Week Ahead Preview

Emerging Markets: Week Ahead Preview30 Jul 2018

Emerging Markets: Week Ahead Preview

Emerging Markets: Week Ahead Preview23 Jul 2018

Emerging Market Preview: Week Ahead

Emerging Market Preview: Week Ahead3 Jul 2018

Emerging Markets: What Changed

Emerging Markets: What Changed2 Jul 2018

Emerging Markets: Preview of the Week Ahead

Emerging Markets: Preview of the Week Ahead26 Jun 2018

Emerging Markets: What Changed

Emerging Markets: What Changed25 Jun 2018

Emerging Markets: Week Ahead Preview

Emerging Markets: Week Ahead Preview19 Jun 2018

Emerging Markets: What Changed

Emerging Markets: What Changed18 Jun 2018