Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

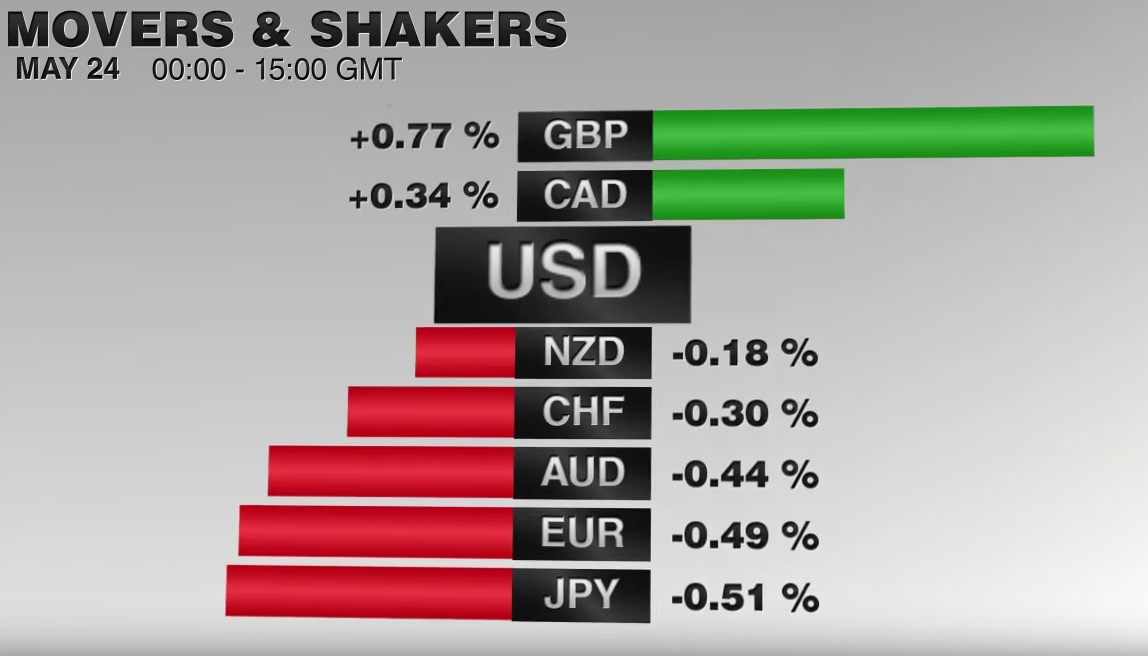

The US dollar is firmer but largely confined to the ranges seen before the weekend against most of the major currencies. The yen is also firmer as dollar sellers reemerged near JPY114.00. The dollar is gaining against most emerging market currencies, though Asian currencies, notably the Korean Won, are firmer.

Although emerging market currencies and commodities are heavier, global equities are continuing their advance since bottoming February 11-12. Even disappointing industrial output and retail sales figures from China over the weekend did not hold back Chinese shares. The Shanghai Composite rose 1.75% to bring the month-to-date gain to 6.4%. The MSCI Asia-Pacific index rose 1.25% to reach its best level since January 6.

European markets are higher as well. The DAX is straddling the 10,000 level for the first time since the middle of January. The three German state elections saw the anti-EU/anti-immigrant AfD surpass the threshold to serve in local parliaments. However, the lead party in state coalition was returned, suggested that the Bundesrat, the upper chamber of parliament where the states are represented, will not change.

The Dow Jones Stoxx 600 is up about 0.65%, led by materials and information technology. Profit-taking appears to be weighing on the energy sector and utilities. European bond markets are also firm. Benchmark 10-year yields are off 2-4 bp. Fitch took away Finland's AAA rating before the weekend to AA+, matching S&P, leaving only Moody's, of the big three rating agencies with the highest rating. Finnish bonds seem unperturbed and are among participating fully in today's advance.

Japan reported a surprising 15% rise in January machine order. The Bloomberg consensus was for a 1.9% rise. The December series was revised to 1.0% from 4.2%. However, the year-over-year pace jumps to 8.4%. This is a forward-looking data point and is a proxy for capex.

Separately, Reuters reported that the Investment Trusts Association was requesting an exemption from the BOJ's negative rates policy. In some ways, the liquidity has become a hot potato of sorts with the introduction of negative rates. The association warned that if it is not given an exemption, its funds (~$90 bln) would be brought into the banking system the form of deposits.

The BOJ began its two-day meeting. It is not expected to cut rates or add to its asset purchase operations. It is expected to confirm the JPY80 trillion expansion target of the monetary base. Many expect the BOJ to ease as early as next month. Its recent adoption of negative interest rates was supposed to compliment the asset purchase program. The asset purchases were mostly adjusted once a year, while the interest rate tool, with the zero barrier broken, could be used more frequently, as the ECB demonstrates. However, given the push back at the G20 meeting, some think the BOJ would add to QQE rather than cut rates again.

The light North American news stream will likely facilitate continued consolidation in the foreign exchange market. The week's key events, including the FOMC meeting, lie ahead. There is no US economic data today. Retail sales, PPI, the Empire State Manufacturing survey and business inventories will be reported tomorrow.

The euro is an about a 2/3 cent range. Provided it holds above the $1.1040-$1.1060 area, the euro can move higher on technical considerations. The $1.1300 area is our projection though the high from February 11 is near $1.1375. The dollar has poked above JPY114 numerous times over the past month but has not closed above it since February 17. Initial support is seen near JPY112.80.

Sterling activity has changed over the past couple of weeks. It has gone from selling into bounces to buying dips. The pullback below $1.4350 in the European morning was snapped up. It is poised to challenge $1.4400 and then the pre-weekend high near $1.4435. The dollar-bloc is consolidating the strong gains seen at the end of last week.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: AfD