Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

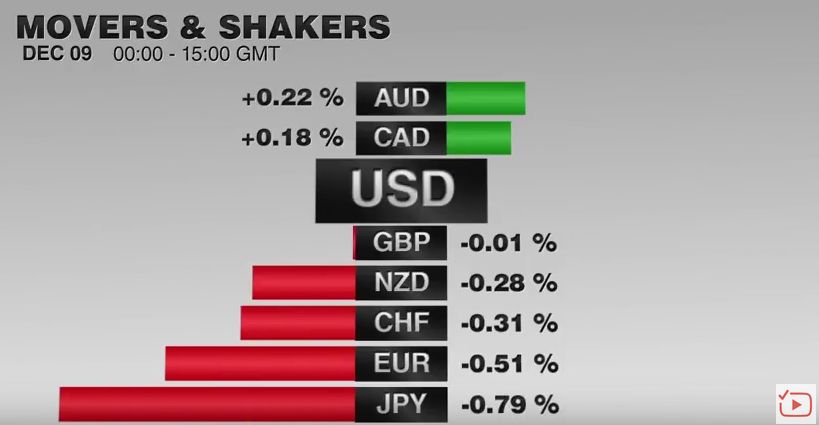

The US dollar is trading choppily but with a distinct softer bias. The economic news has been limited, and the apparent downing of a Russian plane by Turkey caused a flurry of activity, with Turkish assets coming under initial pressure which has abated somewhat.

The euro briefly dipped below $1.06 yesterday for new seven-month lows, but there was no follow through selling. As is often the case with such chart points, a snap back after the violation, the euro reached $1.0670 in early Europe.

Although the speculative market, judging from the positioning in the futures markets and the clear down trend since mind-October, is stretched bearish sentiment prevails. Euro bounces are shallow and greeted with fresh sales. Resistance is seen in the $1.0680-$1.0700 area. In the larger picture, we suspect aggressive market positioning will facilitate selling the rumor buying the fact type of activity around the significant events next month.

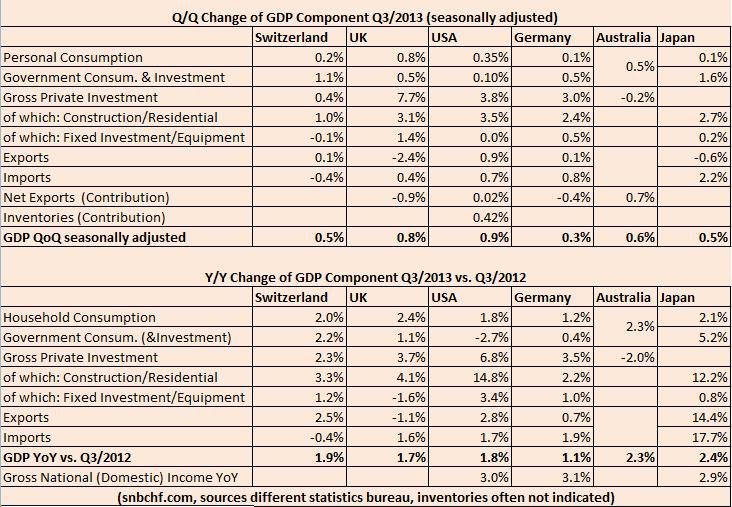

German Q3 GDP was confirmed at 0.3%. The details showed a 0.7% increase in domestic demand after a 0.2% decline in Q2. Private consumption rose 0.5%, while government spending increased 1.3%. Capital and construction investment each declined by 0.3%, weaker than expected. Export growth slowed to 0.2% from a revised 1.8% increase in Q2 (initially was 2.2%). German imports rose 1.1% on the quarter, twice the revised pace in Q2 (initially 0.8% and revised to 0.5%).

There had been some concern that the Germany economy was hitting a soft patch, the flash PMI data earlier this week helped ease such concerns, and today's IFO survey offers additional assurances. Both the current assessment and expectations rose by more than expected, lifting the overall climate measure to its best level in more than a year.

Japan's preliminary manufacturing PMI rose to 52.8 from 52.4. It is the highest level since March 2014, just before the sales tax increase. This is consistent with our argument against claims that Japan is in either a "technical" or "official" recession because of two consecutive quarters of negative growth. The characterization is supposed to imply the end of the business cycle. Our dispute is not a quibble over the word choice but of what it is to signify. Japan's business cycle has not ended. With trend growth a lowly 0.5%, the normal vagaries of a modern economy could see it contract without signifying very much.

The dollar has been trading between roughly JPY122 and last week's high near JPY123.75. The 20-day moving average (~JPY122.35) has not been broken since October 22. A break could spur a move toward JPY121.60. Two drivers of dollar-yen are warning that the risks of this are increasing. Equities are trading heavily. The US 10-year premium over Japan has been trending lower since peaking on November 10 just above 202 bp. It is now at 190 bp and falling though the 20-day average near 193 bp.

Sterling continues to trade heavily. It has lost more than two cents over the past five sessions since peaking near $1.5335 on November 19. Comments form BOE officials testifying before the Treasury Select Committee seemed not to have added much fresh color on the UK rate outlook. Sterling is trying to stabilize after approaching $1.5100. A move above $1.5160 is needed to take the downside pressure off.

The US has several economic reports on tap. The advanced look at October's merchandise trade balance (expected to worsen to -$61 bln from -$58.3 bln) probably is the most important as it will impact estimates for Q4 growth. However, it is the revision to Q3 GDP that might have the most market impact. It appears that the inventories and net exports were not as much of a drag. An upward revision is expected to 2.0% or a little above from 1.5%. It is important to remember that trend growth in the US has slowed from the 2.75%-3.25% prior to the crisis to around 2.0% now due to slower labor forces growth and productivity.

S&P/CaseShiller provide an upward of their house price indices. The gradual increase in prices is expected to continue. The Conference Board’s measure of consumer confidence will be released. It had fallen in October to 97.6 from the eight-month high in September and is expected to have rebounded back above 99.0 in November.

Turkish stocks suffered their biggest decline in three months, and the Turkish lira was among the weakest of the emerging market currencies following news that it had downed a Russian plane. The dispute is whether the plane was over Syrian or Turkish territory. Recently Turkey had shot down a drone. The domestic situation in Turkey is in flux. The announcement of a new cabinet is awaited. The central bank meets today but is not expected to change policy.

Separately, Turkey is negotiating with EU on handling the refugee/migrant issue. The EU is seeking tighter border controls and for Turkey to give worker visas to the estimated two million Syrians already in the country. Turkey wants the EU to unlock about 3 bln euros in aid and re-open accession negotiations. There is an EU-Turkey summit next week.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: German Imports