Stock MarketsEM FX gained some limited traction Friday but still capped off another awful week. So far this quarter, the worst EM performers are TRY (-6%), MXN (-5%), ZAR (-4%), COP, and BRL (both -2.5%). We expect these currencies to remain under pressure as political concerns are unlikely to dissipate anytime soon. |

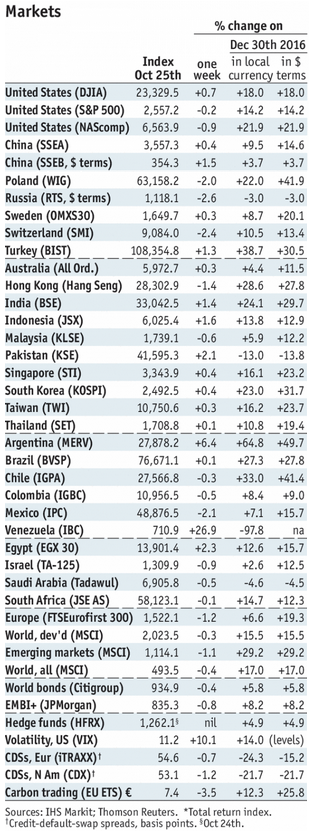

Stock Markets Emerging Markets, October 30 Source: economist.com - Click to enlarge |

South AfricaSouth Africa reports September budget, money, and loan data Monday. We expect the budget numbers to continue worsening, as Finance Minister Gigaba did not set forth any serious measures to control the deficit in his mid-term budget speech last week. Q3 unemployment and September trade will be reported Tuesday. The weak rand may prevent the SARB from cutting rates at the next policy meeting November 23. ChileChile reports September IP Monday, which is expected to rise 2.0% y/y vs. 5.1% in August. It then reports September retail sales Friday, which are expected to rise 4.3% y/y vs. 6.0% in August. The recovery continues, which should support the central bank’s view that the easing cycle is over. However, with inflation at 1.5% and below the 2-4% target range, rate hikes are unlikely until we are well into 2018. BrazilBrazil reports September consolidated budget data Monday. The central government deficit came in as expected last week, and showed a narrowing of the 12-month total as tax revenues strengthened. Brazil then reports September IP (3.1% y/y expected) and October trade Wednesday. With the economy picking up, the fiscal numbers should improve marginally. KoreaKorea reports September IP Tuesday, which is expected to rise 4.8% y/y vs. 2.7% in August. It then reports October CPI and trade Wednesday. Inflation is seen at 1.9% y/y vs. 2.1% in September. It remains near the 2% target, but the growth outlook is uncertain and should keep the BOK on hold well into 2018. Next policy meeting is November 30, no change is expected. September current account data will be reportedFriday. ChinaChina reports official October manufacturing PMI Tuesday, which is expected at 52.1 vs. 52.4 in September. Caixin reports its manufacturing PMI Wednesday, which is expected to remain steady at 51.0. For now, the mainland economic outlook remains solid and that is helping the regional economies perform better. TurkeyTurkey reports September trade Tuesday. The central bank releases its quarterly inflation report Wednesday. October CPI will be reported Friday, which is expected to rise 11.5% y/y vs. 11.2% in September. Despite the worsening inflation outlook, the central bank just left policy unchanged last week. The weaker lira will likely feed into even higher inflation, and so we think the decision to stand pat was wrong. TaiwanTaiwan reports Q3 GDP Tuesday, which is expected to grow 2.0% y/y vs. 2.1% in Q2. The stabilizing mainland economy should continue to help Taiwan. However, low inflation should allow the central bank to keep rates steady through most of 2018. PolandPoland reports October CPI Tuesday, which is expected to rise 2.1% y/y vs. 2.2% in September. If so, inflation would still be in the bottom half of the 1.5-3.5% target range. Still, we disagree with the central bank’s stated intent to keep rates steady through 2018. Some on the MPC are starting to dissent too. Next policy meeting is November 8, no change is expected. MexicoMexico reports Q3 GDP Tuesday, which is expected to grow 1.6% y/y vs. 1.8% in Q3. We think monthly data suggest a growth rate around 1.7% y/y. The economy remains sluggish, but Banxico may be forced into restarting the tightening cycle if peso weakness persists. Next policy meeting is November 9, no action is likely then. The December 14 meeting will be very interesting, especially if the Fed hikes the day before. ThailandThailand reports October CPI Wednesday, which is expected to rise 0.82% y/y vs. 0.86% in September. If so, this would still be below the 1.0-4.0% target range. The economy is recovering, but low price pressures should allow the BOT to remain on hold well into 2018. Next policy meeting is November 8, no change is expected. IndonesiaIndonesia reports October CPI Wednesday, which is expected to rise 3.67% y/y vs. 3.72% in September. If so, this would be in the bottom half of the 3-5% target range. Here too, the economy is recovering, but low price pressures should allow Bank Indonesia to remain on hold well into 2018. Next policy meeting is November 16, no change is expected. PeruPeru reports October CPI Wednesday, which is expected to rise 2.6% y/y vs. 2.9% in September. Inflation has been hovering near the top of the 1-3% target range for several months, which has kept the central bank cautious and cutting rates at every other meeting. Next policy meeting is November 9, and if the pattern holds, a 25 bp cut will likely be delivered then now that inflation has fallen a bit. Czech RepublicCzech National Bank meets Thursday and is expected to hike rates 25 bp to 0.5%. It has been on hold since the initial 20 bp hike to 0.25% back in August. Since that move, EUR/CZK has fallen about 1.5%. The central bank’s model suggests a 1% move in the currency is equivalent to a 25 bp hike. September trade will be reported Friday. ColombiaColombia reports October CPI Saturday, which is expected to rise 4.13% y/y vs. 3.97% in September. If so, inflation would move above the 2-4% target band for the first time since May. Rising inflation kept the bank on hold in September for the first time since February, but it surprised the markets with a 25 bp cut to 5.0% on Friday. The sluggish economy will likely lead to further easing even before the inflation trajectory improves. |

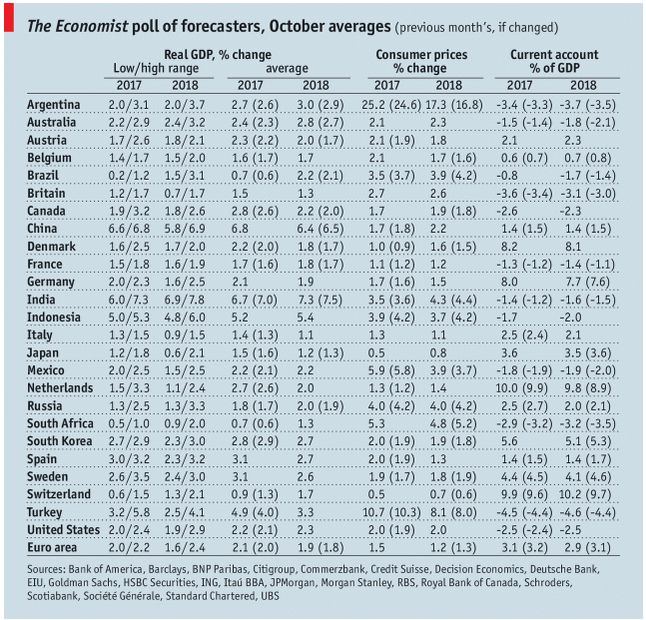

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, October 2017 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent,win-thin