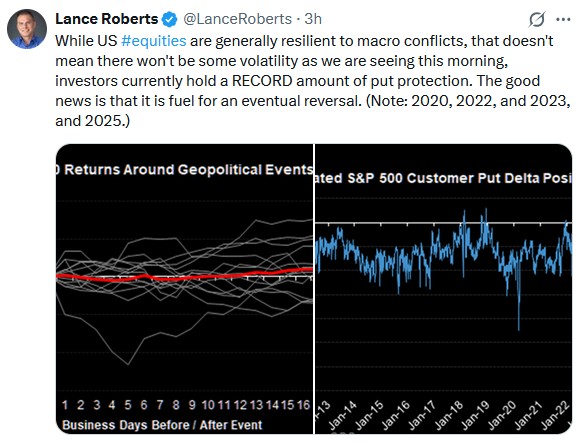

The question for investors is how the Iranian conflict will affect the stock market. The markets' initial reaction on Sunday was concern as the S&P 500 fell by over 1%, crude oil rose nearly 10%, and precious metals rallied. Within 12 hours, many of the substantial gains or losses, except oil, were reversed. However, stocks, after closing positively on Monday, opened sharply lower on Tuesday. Such volatility should be expected, especially at the onset of this conflict. We must accept this temporary regime, stay alert to our technical indicators, but not forget longer-term fundamentals. To wit, ask yourself how this Middle East conflict will impact earnings for the stocks I own. The likely answer, assuming the war doesn't escalate significantly, is not much.

A recent history of Middle East conflicts (with large oil producers) shows that stocks tend to be unaffected after the initial jolt. The graphs below show how the S&P 500 and crude oil prices behaved on a monthly basis during the Gulf Crisis in 1991, the Iraq War in 1993, and the 2025 US bombing of Iran’s nuclear facilities. The S&P 500 posted gains one month after all three events started and held them for at least a year. In all three instances, crude oil prices spiked; however, over the next three months, the gains during the Gulf and Iraq Wars were somewhat limited.

The markets will be trading from headline to headline over the coming days. Positive headlines, foretelling a quick end to hostilities, should benefit stock prices. Conversely, intensifying actions and damage to Iran’s oil complex could unsettle markets. But, as we show below, investors are generally not afraid of conflicts or even war once they have time to digest the news.

We continue with the Middle East topic below regarding the dollar and precious metals.

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, we touched on the historical relationship between oil prices and military operations and conflicts. Another area to watch, and as we have discussed previously, is the US Dollar.

"A good example of that lately has been the “weak dollar” narrative, which has pushed investors to chase foreign assets. The negative correlation between a weak dollar and rising international stock exposure appears to be a free return. Unsurprisingly, the story spreads fast because performance charts look clean during a dollar slide."

As we noted in that discussion, a dollar rally was becoming more likely.

"First, positioning and technicals matter. From a long-term technical perspective, the U.S. Dollar Index is attempting to stabilize after a 2025 downside move. As shown, using a 3-year price momentum measure, the dollar is as oversold now as it was at previous dollar bottoms. The current move lower is becoming increasingly stretched, reducing the catalyst needed to trigger a sharp reversal. A weak dollar trend also encourages leverage through unhedged international stock exposure. As shown, investors have piled into global sector funds (excluding technology) over the past year to boost returns. However, the last time we saw that kind of exposure shift was in 2021, just before the counter-trend rally in the dollar that hit returns fast."

When you have a lot of positioning that becomes offside due to a momentum chase, all it takes is an "event" of some kind to cause a reversal. Military operations in Iran certainly qualify as a reason to seek the safety of the US Dollar.

With asset managers pushing record shorts against the US Dollar, if the military conflict in Iran continues, short-covering as the dollar rises could further fuel that rise.

The risk for investors is that if the dollar rally gains traction and breaks above 100, the negative impact on non-dollar trades, such as emerging markets, international stocks, and precious metals, could intensify. As such, investors should consider managing potential risk until the situation in Iran begins to cool.

- Start with position sizing. Set a strategic range for international stock exposure based on your risk tolerance and drawdown limits. Critically, keep that range stable and don’t allow the recent weakness in the dollar to dictate long-term weights.

- Use rules-based rebalancing. When foreign equities run above target due to a weak dollar surge, trim toward policy weight. When foreign equities lag, add slowly. Rebalancing reduces the damage of an unexpected reversal.

- Add currency awareness. Consider a split allocation between hedged and unhedged developed exposure. Hedged exposure reduces the impact of a dollar rally, while unhedged exposure keeps diversification benefits when the weak dollar resumes. MSCI publishes a 100% hedged EAFE benchmark that helps investors compare results across hedged and unhedged frameworks.

- Focus on earnings quality as fundamentals will always matter in the end. Continue to favor markets and sectors with stable cash flows, strong balance sheets, and pricing power, as those traits matter when currencies swing and financial conditions tighten.

- Avoid valuation shortcuts. Do not rely on “cheaper than the U.S.” Use local history and earnings trends. If international multiples rise while earnings lag, reduce exposure, even if the weak-dollar story remains popular.

- Finally, stress test the portfolio. Model a 5 percent to 10 percent dollar rally and a 10 percent drawdown in foreign equities at the same time. If the model shows unacceptable damage, reduce unhedged international stock exposure before the market enforces the change.

Trade accordingly.

The Dollar Soars: Gold And Silver Falter

It's a widely held opinion that precious metals are a safe-haven asset in times of geopolitical stress. However, as we share below, that is not the case today. The explanation lies in the dollar. When investors become risk-averse, global investors instinctively move into US dollar-denominated assets, resulting in a surge in dollar demand. Accordingly, a stronger dollar makes gold more expensive for foreign buyers, directly suppressing demand and pushing prices lower even as headlines suggest the opposite should be happening.

When the dollar surges, it effectively absorbs the fear trade that would otherwise flow into precious metals. Silver tends to be worse off than gold because it has a significant industrial demand component. To wit, if the conflict raises fears of slowing global growth or trade disruption, expectations of industrial demand fall.

Simply put, and as shown below, the dollar, not gold or silver, is thus far the preferred panic button in this conflict.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post Middle East Military Conflicts And Stocks appeared first on RIA.

Full story here Are you the author?You Might Also Like

2026-02-20

Money – everybody wants it, but few actually have it. As shown in recent financial statistics, the “wealth gap” in America continues to grow between the “haves” and the “have-nots.” That gap has led to a bombardment of narratives explaining why younger generations are financially oppressed. As shown, the top 10% of income earners own …

Software Or Staples?

Software Or Staples?

2026-02-09

As we wrote in yesterday’s Commentary, efficiently rotating between overbought and oversold sectors, factors, or stocks is a well-established method for outperforming markets. Like any strategy, the hard part is timing, or properly estimating when a pair of sectors, factors, or stocks is about to reverse their respective trends. Currently, there is a massive divergence …

Fannie And Freddie Add Billions To The Bond Market

Fannie And Freddie Add Billions To The Bond Market

2025-12-18

According to Bloomberg, Fannie Mae and Freddie Mac have been increasing the mortgages and mortgage-backed securities they hold on their own balance sheets. At their peak, before the financial crisis, Fannie and Freddie held a combined total of $1.6 trillion in mortgages. As we share below, courtesy of Bloomberg, their portfolio sizes are well below …

OpenAI Seeks Government Support

OpenAI Seeks Government Support

2025-11-07

Sarah Friar, OpenAI’s CFO, spoke at a Wall Street Journal technology conference to update the audience on the potential of AI. While her comments were very optimistic, she noted that OpenAI seeks continued capital inflows, highlighting the lynchpin for AI development. Her quote below, courtesy of Bloomberg, takes traditional bank and industry financing a step …

Investor Dilemma: Pavlov Rings The Bell – Draft

Investor Dilemma: Pavlov Rings The Bell – Draft

2025-11-03

Classical conditioning teaches us a valuable lesson regarding the current investor dilemma. Pavlov’s research discovered a basic psychological rule: when a neutral stimulus is repeatedly paired with a reward‑stimulus, eventually it will trigger the same response even when the reward is absent. The famed experiment by Ivan Pavlov illustrated that dogs would salivate at the …

Dow Theory: A Concerning Divergence Or Artifact?

Dow Theory: A Concerning Divergence Or Artifact?

2025-10-31

Dow Theory is a market tool developed by Charles Dow in the very early 1900s. Dow also created the Dow Jones Industrial Average. The basic gist of Dow theory is that market trends are confirmed when gains or record highs are established in the broader market indexes, and then confirmed by similar trends and/or record …

Leveraged ETFs: Yet Another Sign Of Rampant Speculation

Leveraged ETFs: Yet Another Sign Of Rampant Speculation

2025-10-22

Not only is the market chasing the most speculative of assets, but it is employing record amounts of leverage to do so. Traditionally, investors use margin loans to gain leverage. More recently, however, leveraged ETFs allow investors to get leverage in one package. To wit, the graph below, courtesy of BofA, shows that there are …

Tags: Featured,newsletter