Few Fed meetings in recent memory have presented the FOMC with a more uncomfortable set of competing signals than yesterday's. The Iranian conflict and its impact on oil and oil-dependent product prices have created the potential for an inflationary impulse, yet higher oil prices would likely slow economic activity, leading to higher unemployment. As if the balance between the Fed's two Congressional mandates, stable prices and maximum employment, wasn't challenging enough, they just learned that fourth-quarter GDP was revised lower to a mere 0.7% growth rate. Moreover, consumer spending is showing signs of fatigue, the labor market is slowly weakening, and financial conditions have tightened due to private credit stress and the dollar's recent appreciation.

Against that backdrop, the FOMC held rates steady as expected. Stephen Miran was the lone dissenter, voting for a 25 bps cut. The Fed left the prior statement largely unchanged. The only notable addition was the following sentence regarding the Iranian conflict:

The implications of developments in the Middle East for the US economy are uncertain.

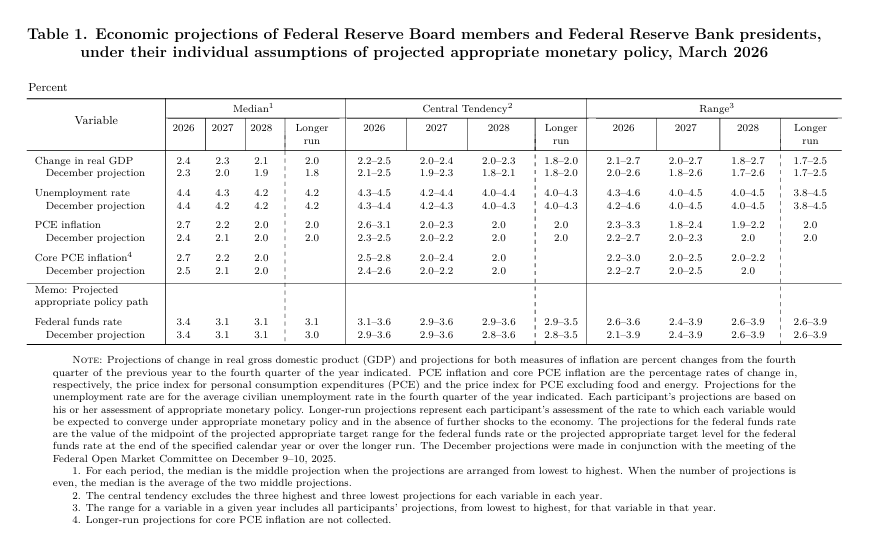

The Fed released its quarterly Summary of Economic Projections (SEP), shown below. The only notable change was an increase in their collective inflation forecast. Its PCE forecast was raised by 0.3% from the December SEP, while core PCE was raised by 0.2%. Per the projections, the Fed still expects to cut rates one time this year.

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, we discussed managing portfolio risks and the fallacy of "Missing The 10-Best Days" in the market. Adding on to that discussion is a warning from the credit markets. As we have discussed previously, if you are worried about a market correction, the only thing you need to watch is credit spreads. The reason is that credit is the lifeblood of the economy, and since yields are a function of fundamental factors, shifts in spreads have a very strong correlation with market outcomes.

For more discussion on this topic: Credit Spreads: The Market's Early Warning Indicators - RIA

"The “Junk to Treasury bond” spread provides signals of market stress or impending market corrections. The reason is that if you are buying bonds that have a high risk of default (aka “junk bonds”), you should be paid a premium for the risk that is undertaken relative to the “risk-free” rate offered by U.S. Treasury bonds. The spread identifies when investors are willing to speculate in the markets and forgo the “risk premium.”

As shown, this has typically not ended well, which is why understanding credit spreads is important to investing outcomes."

I bring this up because credit spreads are starting to widen. As noted by Senitmentrader.com yesterday:

"One of the main drivers of the rise in stock prices this year has been loose financial conditions. That's something of a tautology because stock prices are a portion of most financial condition models, but other inputs carry just as much, if not more, weight. One of those factors is bond spreads. As spreads widen, showing distress, it feeds into tighter financial conditions. Many of those models show tightening conditions, which have preceded more challenging environments for stocks."

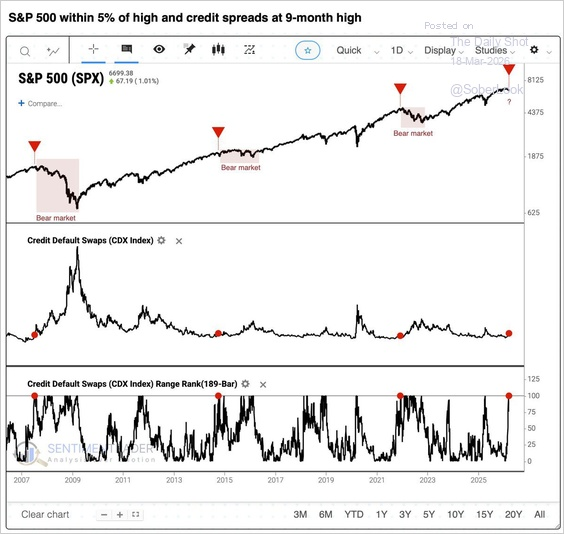

As shown, over the past 20 years, whenever credit spreads reached 9-month highs while the S&P remained within 5% of its high, a bear market followed.

While there is no guarantee that it will happen this time, the track record is at least worth paying attention to. The rise in credit spreads is notable and suggests there are "cracks" in the market's foundation. As such, our suggestions for tighter risk controls and rebalancing remain key until things begin to correct themselves.

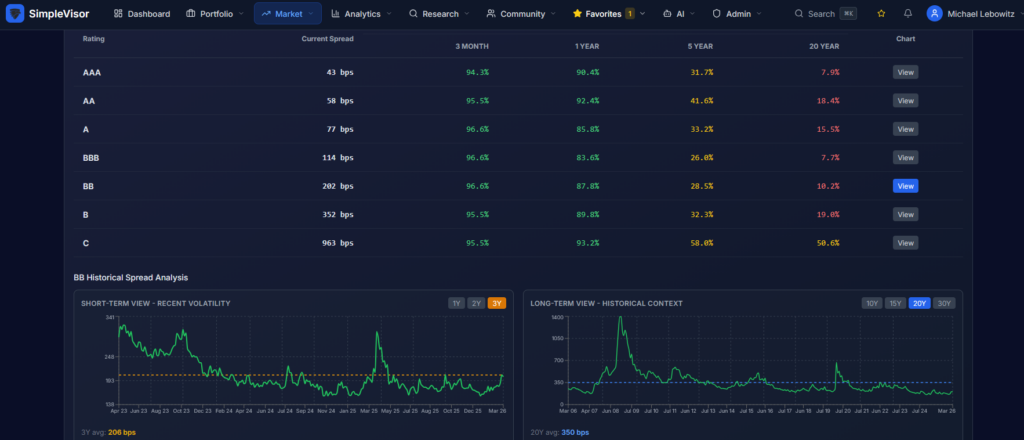

Track credit spreads on SimpleVisor. As we show below on our soon-to-be-released version, spreads have been widening, but on a long-term basis, they remain very tight.

Gold Falls On Higher PPI And Oil Prices: Confused?

The price of gold opened about 2% lower on Wednesday despite oil trading near $100 and PPI coming in hotter than expected. If you think gold is an inflation hedge, you must be a little confused. Let us explain.

For starters, the daily gyrations of gold or any other asset are not always aligned with fundamentals. Longer-term trends tend to better reflect fundamentals. However, Wednesday's price decline has some rationale. The quote below from FinViz explains why.

Gold futures plunged 2% as oil prices held above $100/barrel from Iran-Israel conflict escalation fueled inflation fears and hawkish Fed bets

Because higher oil prices are potentially inflationary, it becomes more likely that the Fed shifts to a more hawkish policy stance. Historically, gold prices are more closely correlated with real interest rates (yields less inflation) than with inflation. When real rates are low or negative, it means the Fed's policies are overly dovish. Such aggressive monetary policy often goes hand in hand with higher gold prices. Conversely, when real rates are high, as they are today and as investors expect going forward, gold tends to do poorly. That has not been the case over the last few years, although it has been for many years, as we share in the graph below from our article, Gold Investors Are Betting On the Fed (2/22/2023). The orange squares indicate that the correlation weakened in 2022. It has further eroded since then.

The consideration for gold bulls is whether gold prices may be returning to their real rate basis. If so, a hawkish Fed may not bode well for gold prices.

Private Credit Stress: Will The Fed Backstop Exuberance Again?

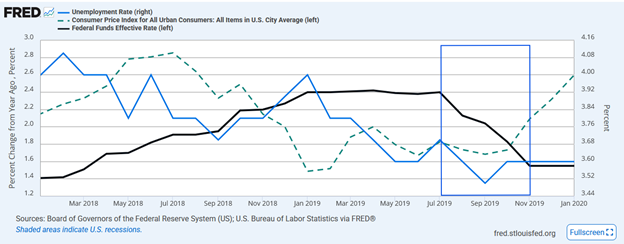

The Fed has a history of cutting rates and boosting liquidity when the labor market and inflation levels don’t necessitate action. For instance, in 1998, the Fed cut rates three times in rapid succession and orchestrated a private-sector rescue of Long-Term Capital Management to prevent the hedge fund’s collapse from cascading through Wall Street. More recently, in 2019, the Fed injected hundreds of billions of dollars into the repo markets and cut rates when overnight funding rates spiked, but with no immediate connection to inflation or unemployment, as we show below.

To help you evaluate whether rising stress in the private credit market will warrant Fed action, we explain what private credit is, identify the key players, compare the current situation to the subprime crisis, and explain how this stress could prompt the Fed to act.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post A Fed Balancing Act: Oil, Iran, Slower Growth appeared first on RIA.

Full story here Are you the author?You Might Also Like

Credit Spreads Are Widening: Omen Or No Bother?

Credit Spreads Are Widening: Omen Or No Bother?

2026-03-05

Increasing corporate credit spreads, or a growing divergence between corporate bond yields and similar-maturity Treasury yields, can be an omen of stock market weakness. Recent troublesome defaults in the private credit markets are showing signs of spreading concern to the more liquid corporate debt markets. Thus, it’s appropriate to review corporate credit spreads. in the …

2026-01-20

Supporting the dollar-debasement narrative is the claim that money supply growth is out of control. For instance, we saw a post claiming “US money creation is happening at an alarming pace.” Specifically, he says the money supply increased by $1.65 trillion in 2025. Quoting the money supply, as he does, in absolute dollar terms is …

2026-01-09

Every January, it happens like clockwork: you drive by gym parking lots that look like a Taylor Swift concert. Go to the store, and the salad aisles are ransacked like there’s a lettuce shortage, and half of your coworkers suddenly start quoting Warren Buffett while buying stock in companies they can’t spell. You got it, …

Tesla EV Deliveries Continue to Lag Global Rivals

Tesla EV Deliveries Continue to Lag Global Rivals

2026-01-05

Tesla EV deliveries totaled 1.64 million vehicles in 2025, leaving the company behind China’s BYD, which delivered more than 2.2 million EVs for the year. The result marks a second consecutive annual decline in Tesla EV deliveries, reinforcing the growing pressure on the company’s core automotive business. Fourth-quarter deliveries fell sharply year over year, underscoring …

Permanent Job Losers: A Worrying Facet Of Today’s Economy

Permanent Job Losers: A Worrying Facet Of Today’s Economy

2025-11-24

Given the two-month delay, Thursday’s BLS employment report on September labor market conditions was not nearly as pertinent as the BLS data typically is. Despite it being old news, it is worth sharing that the number of jobs increased by 119k, but the unemployment rate ticked up from 4.3% to 4.4%. The markets didn’t seem …

Forward Return And The Importance Of Math

Forward Return And The Importance Of Math

2025-11-10

During strongly trending bull markets, investors often overlook the importance of math in predicting forward returns. Such is easy to do when the market just seemingly continues to rise without regard to fundamentals. The current environment is also heavily influenced by the impact of “passive indexing,” which has distorted market dynamics as well. However, none …

Tags: Featured,newsletter