A recent Bloomberg article, "Microsoft, Meta Add to $700 Billion Surge in Data Center Leases," reminds us that the massive growth in data centers will continue for the foreseeable future. However, it also warns that the massive investments in AI infrastructure by the largest AI companies exceed what their financial statements suggest.

The article notes that Microsoft and Meta each committed nearly $50 billion in additional data center leases in their most recent quarters. As the Bloomberg graph below shows, data center lease commitments from the largest cloud computing companies are above $700 billion. Oracle leads the group with $261 billion, much of which is tied to its contract with OpenAI. Data center leases do not appear on balance sheets because accounting rules require recognition only when payments begin. In other words, investors may not be fully aware of the true amount of capital commitments these companies have made but have not yet paid for the AI infrastructure buildout.

Could the massive AI-related spending, both on- and off-balance-sheet, become a dangerous overcommitment? The answer lies in the amount and timing of AI-related revenue. While the question is unanswerable today, it's worth appreciating that history is littered with examples of industries that spent massively on infrastructure in anticipation of demand that arrived more slowly than expected. The most recent example is the fiber-optic networks of the late 1990s.

The AI revolution may well justify every dollar of investment committed and maybe more, but investors would be wise to assess whether the revenue models will mature quickly enough to service the obligations being incurred today.

What To Watch Today

Earnings

Economy

Market Trading Update

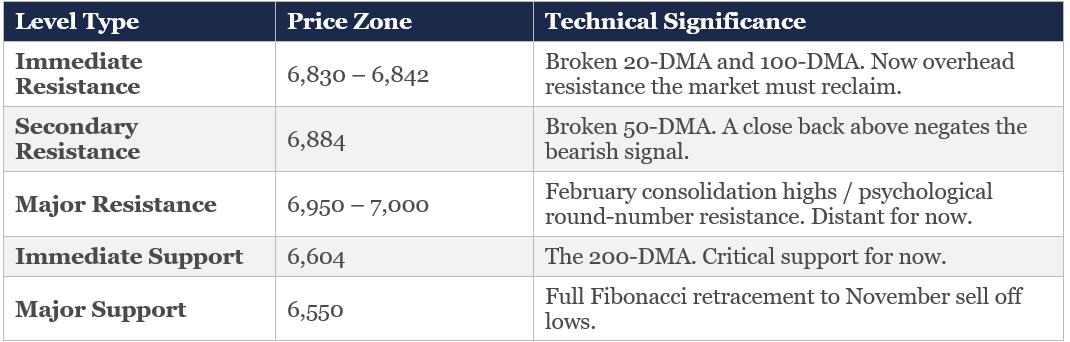

The S&P 500 closed Friday at 6,632, capping a brutal three-week losing streak—the first in roughly a year. From the late-January high of 7,002, the index is now down 5.3% and has broken every major moving average below. The March 9th selloff, triggered by Operation Epic Fury and the Iran escalation, wiped nearly $900 billion from equities in a single session. On Thursday, Iran’s new Supreme Leader declared the Strait of Hormuz must remain closed, sending Brent temporarily above $100 per barrel for the first time since August 2022.

The technical damage is significant. The index decisively is pushing toward support at the 200-DMA (~6,604) on Friday, after a reflexive bounce off the previous intraday low failed at the 50-DMA. The 50-DMA (~6,884) and 100-DMA (~6,842) are now overhead resistance.

As we noted in Thursday's Daily Market Commentary,

"The volume profile clearly tells the story. The Point of Control for the past 90 days sits in the 6,860–6,900 range on the S&P 500, meaning that’s where the heaviest concentration of transactions occurred during the recent consolidation phase. With the index now trading well below that zone, the majority of those positions are underwater. That matters enormously for what happens next — because it fundamentally changes the behavioral calculus of a large swath of market participants.

Here’s the mechanics: when investors are trapped in losing positions, they don’t behave like buyers, but sellers-in-waiting. This is what we term “trapped longs,” as every relief rally, every bounce on a ceasefire rumor, a dovish Fed comment, or a better-than-expected data print, becomes an exit opportunity rather than a signal to add exposure. "

The MACD sits at −28.92, firmly in sell territory and oversold. The 14-day RSI has plunged to 33, and is approaching oversold but not yet at the extreme washout levels that mark durable bottoms. In other words, next week could see some selling pressure down to the 200-DMA, but look for buyers to step in with markets more oversold.

Bottom line: We have shifted from a “buy the dip” market to a “sell the rip” environment. If the market breaks the 200-DMA, that will be technically significant. Historically, when the index violates that level on high volume, it takes months to establish a durable floor. That said, RSI is nearing oversold, breadth deterioration remains selective (concentrated in mega-cap tech), and the war premium in oil may dissipate if geopolitical conditions stabilize. The 6,600 level is the immediate test; failure there opens 6,300–6,400 and a full 10% correction. A close above the 100-DMA (~6,850) would be the first sign that the worst has passed. Until then, reduce exposure into strength, raise cash, define risk levels, and avoid catching falling knives.

Trade accordingly.

The Week Ahead

The Fed will meet this week to discuss monetary policy. As we share below, the market is pricing in a minisclue 0.8% chance of a rate cut. While the likely "no change to policy" statement is well anticipated, investors will keenly focus on how the Fed is thinking about inflation and economic growth in light of the conflict in Iran and the surge in oil prices.

We think it's probable that the Fed has become even more entrenched with the idea of leaving rates alone, given the risk that higher oil prices could pressure inflation higher. However, it will be interesting to see whether Fed members are equally concerned about the prospect that higher oil prices reduce consumption of other goods, resulting not only in an offset of inflationary pressures but also in weaker economic activity.

Also of note, we are interested in how attuned Fed members are to recent problems in the private credit market and how that might impact the financial system and, ultimately, monetary policy.

Fitzpatrick: Soros CEO & CIO Warn Of Reckoning

Dawn Fitzpatrick says overallocated LPs, frozen distributions, and mounting margin-call risk are converging into a sector-wide shakeout. Such will eventually separate survivors from the casualties. I used Claude to source data on private credit and equity funds, sources disclosed at the end.

In July 2024, I penned an article entitled “Private Equity: Why Am I So Lucky,” which began with:

“Lately, I have been getting many questions about investing in private equity. Such is common during raging bull markets, as individuals seek higher rates of return than the market generates. Also, during these periods, Wall Street tends to bring new companies to market to fill the demand of the investing public. Private equity is always alluring, as is the tale of someone who bought the company’s shares when it was private and made a massive fortune when it went public. Who wouldn’t want a piece of that?”

The private equity (PE) business is huge. When I say huge, I mean $4.4 trillion huge.

However, as we warned then, the risks have come home to roost. The private equity and private credit industry is heading into a gut-wrenching period of consolidation. That, according to one of Wall Street’s most influential investors, Dawn Fitzpatrick, CEO of Soros Fund Management. She told attendees at Bloomberg Invest this week that a “massive culling” of alternative asset managers is coming. And that the industry has no one to blame but itself.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post Data Center Leases: Is Spending Mindful Of Revenues? appeared first on RIA.

Full story here Are you the author?You Might Also Like

2026-02-04

Over the last couple of weeks, we have shared evidence that supports the reflationary narrative and some that defies it. Today, we share the latest ISM Manufacturing data, which lends credence to the reflationary narrative. The ISM Manufacturing survey showed a big improvement in sentiment, as shown below. The gauge shot up 4.7 to 52.6, …

Private Credit Funds Falling Out Of Favor

Private Credit Funds Falling Out Of Favor

2026-02-03

Private credit funds were all the rage in 2024 and 2025 as institutional and high-net-worth retail investors sought more risk and higher returns. Over the last few months, that trend has started reversing. The FT reports that private credit investors pulled more than $7 billion from some of the biggest private credit funds in the …

Bears Are An Endangered Species

Bears Are An Endangered Species

2026-01-31

🔎 At a Glance 🏛️ Market Brief – Market Volatility Returns Markets ended the week mixed as investors processed the Federal Reserve’s latest policy decision, rising geopolitical tensions, and the early results of the S&P 500 earnings season. The Fed held the federal funds rate steady at 3.50–3.75 percent, as expected. Chair Jerome Powell maintained …

Do Sentiment Trends Boost Reflation Odds

Do Sentiment Trends Boost Reflation Odds

2026-01-27

On Monday, we discussed how the Truflation inflation gauge points to a sudden price decline, which clouds the reflation outlook. Today, we share recent consumer sentiment readings that counter the disinflation story and support the reflation narrative. On Friday, the University of Michigan reported that its consumer sentiment index improved in January to a five-month …

2025-12-13

🔎 At a Glance 💬 Ask a Question Have a question about the markets, your portfolio, or a topic you’d like us to cover in a future newsletter? 📩 Email: [email protected]🐦 Follow & DM on X: @LanceRoberts📰 Subscribe on Substack: @LanceRoberts We read every message and may feature your question in next week’s issue! 🏛️ …

ChatGPT Gives Financial Advice On Volatile Markets

ChatGPT Gives Financial Advice On Volatile Markets

2025-10-13

Following Friday’s selloff amid the resurgence of tariff threats on China, I asked ChatGPT a simple question: ” How to Stay Calm In The Stock Market?” That simple question generated an engaging and humorous take on financial advice for navigating volatile markets. In this week’s post, I thought it would be helpful to review ChatGPT’s advice …

OpenAI: Fueling Massive AI Stock Gains

OpenAI: Fueling Massive AI Stock Gains

2025-10-08

As we led in yesterday’s Commentary, AMD rose 25% on the news that OpenAI would purchase 10% of AMD. In exchange, OpenAI will become a significant customer of AMD. This symbiotic relationship is just one of many that OpenAI is forming with companies at the forefront of the AI revolution. The bullet points and graphic …

Tags: Featured,newsletter