To address the many emails we received, we present our take on the Supreme Court's tariff ruling.

First, President Trump has multiple ways he can implement trade restrictions beyond what the Supreme Court ruled against. In fact, he implemented a 150-day 15% global tariff after the court's ruling. As we share below, the effective tariff rate is only 1% below its prior level. The 15% tariff gives Trump time to enact new trade policies. Among the most likely are tax measures based on national security provisions. In addition, he could increase foreign-paid taxes through anti-dumping rules, targeted industry restrictions, procurement policy, or negotiated arrangements with other nations. These options and others effectively function as tariffs but may likely survive judicial review. Trump's tariff policy is not binary, allowed or blocked. In reality, the President and Congress possess a wide range of options to achieve similar economic outcomes, and we believe he will do so.

Second, the market was priced for this ruling. The betting markets were posting 75%+ odds that the Supreme Court would overturn tariffs. Despite reduced government revenue, bond yields opened slightly lower on Monday morning. Stocks are opening lower, but not by a meaningful amount. It's also worth noting that industrial and material stocks had been among the best performing. These types of companies were among the most affected by tariffs. Might their outperformance be the market front running the Supreme Court Decision?

When markets are already positioned for an outcome, the actual event tends to produce more short-term repositioning than a lasting fundamental shift. Our take is that the tariff ruling changes the legal pathway, not the broader trajectory of trade policy or the economic assumptions investors had embedded into prices.

What To Watch Today

Earnings

Economy

Market Trading Update

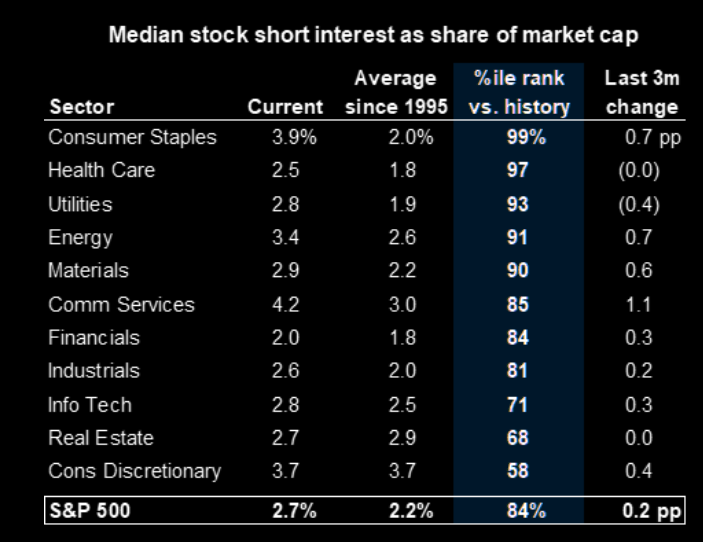

Yesterday, we discussed the technical backdrop of the market heading into this week. One interesting note about the current market is the sharp increase in short interest, which is now at very elevated levels. The median S&P 500 stock carries short interest equivalent to 2.7% of market cap, ranking in the 84th percentile since 1995 and the 97th percentile over the last five years.

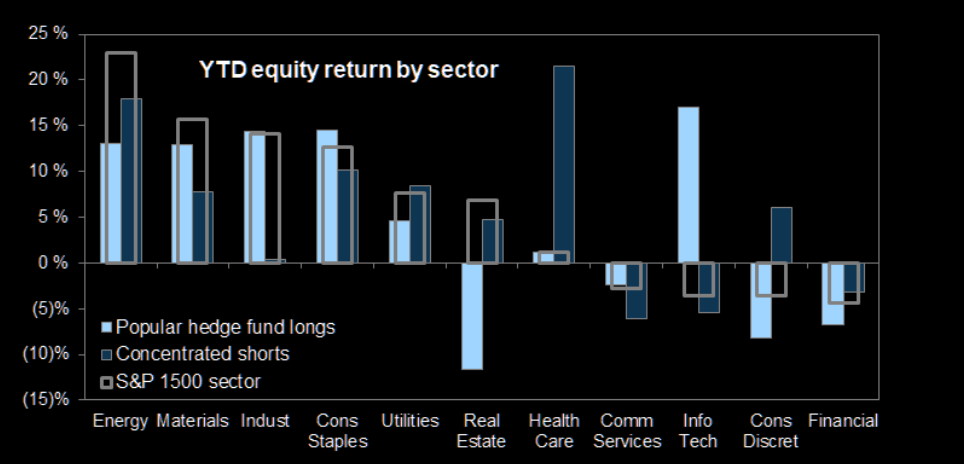

The rise in short interest is not necessarily an immediate alarm bell, but high levels of short interest have previously coincided with poorer returns. Recently, however, that short squeeze has affected nearly every sector. The most concentrated short positions have outperformed popular longs in 6 of 11 sectors YTD. Those sectors, of course, are Materials, Industrials, Staples, Transports, Utilities, and Energy. On the other hand, concentrated shorts have declined outright YTD in Communication Services, Info Tech, and Financials.

As we discussed last week, the bifurcation in market sectors is very notable, and value stocks are not trading as "value" but rather "momentum." In other words, those sectors are not cheap, and with short interest in those defensive sectors at the highest levels relative to history, the risk is rising. Short interest is close to 30-year highs in Consumer Staples and Health Care, and is why Consumer Staples is up +13% YTD.

This is just another one of the many reasons to consider taking profits and rebalancing risk in the traditional "cyclical" and "defensive" areas of the market, and look for an eventual rotation into the areas most beaten up over the last several months. As we noted this past weekend in the #BullBearReport:

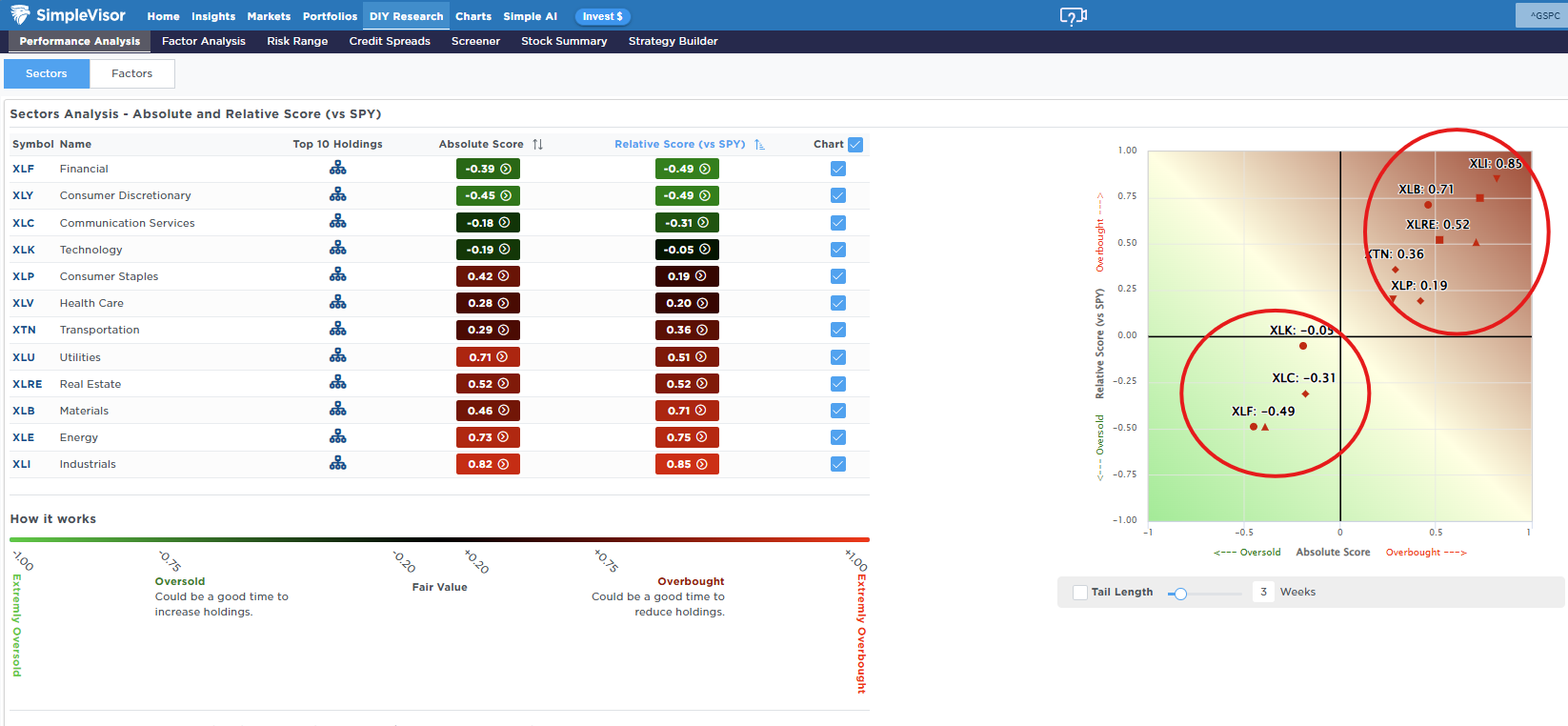

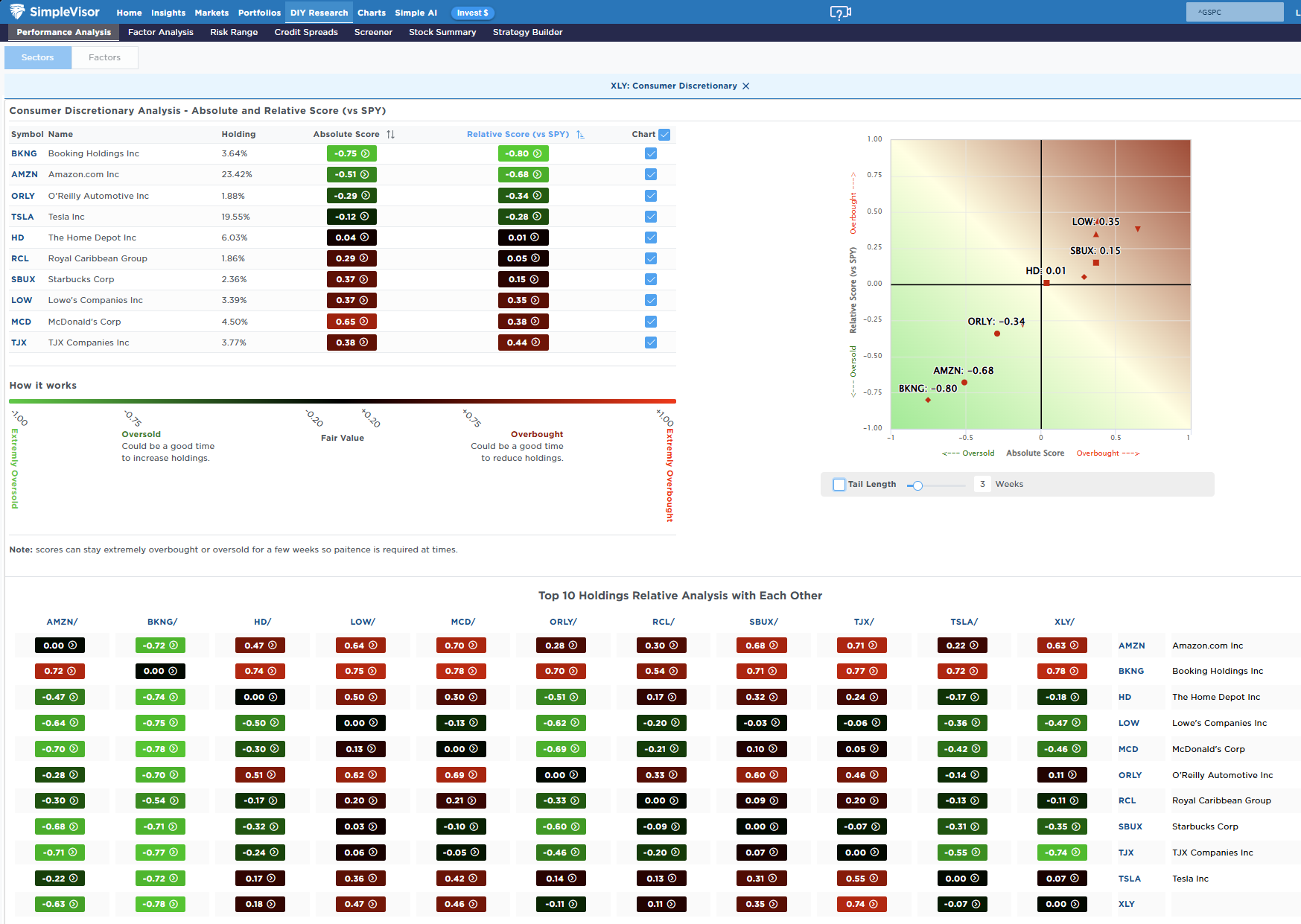

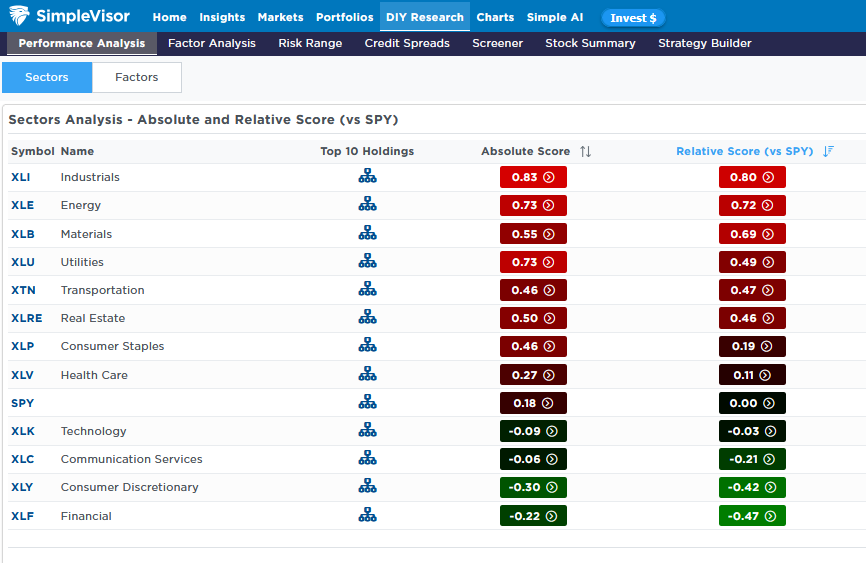

As we noted last week, the “bifurcation” in market-sector performance is pretty telling. Financials, Discretionary, Services, and Technology (the largest sectors of the S&P 500) are the most oversold, while Industrials, Energy, Materials, and Real Estate are the most overbought.

While Financials are the most oversold, I wanted to look at Discretionary given the recent selloff in those stocks. The most oversold in the sector are AMZN and BKNG, with TSLA not far behind. Given the weighting of TSLA and AMZN in the S&P 500, any rotation into these companies will lift the entire index.

Trade accordingly.

Midcaps Lead The Way

Midcap growth stocks led the markets last week, rallying by over 2%. Breadth was better, with large-cap growth stocks up 1.75%. Value stocks underperformed slightly last week. While breadth was improved as judged by returns, the SimpleVisor relative and absolute analysis shows a stark divergence between midcap growth and megacap growth. With a relative score of 0.87, midcap growth stocks are extremely overbought on a relative basis. It is highly likely they start to underperform the market. That said, midcap and small-cap stocks were more impacted by the Supreme Court's tariff ruling than larger stocks. Thus, the positive tariff impact may boost those stock factors for a while longer.

On the sector side, industrials remain grossly overbought. Here, too, however, the removal of tariffs may benefit some industrial stocks that import many of their parts or goods. Like midcap stocks, industrials are due for a relative correction.

Is China Really Dumping US Treasuries?

“China is dumping US Treasuries to get out of the dollar.” This claim has been circulating the mainstream feeds lately, with the narrative that the “end of the dollar is near,” or “the US will lose its funding base” and the “bond yields will surge.” But are those claims valid? Such is what we will explore in more detail.

Let’s start with the chart that has everyone concerned. As shown, China’s holdings of US Treasury bonds have fallen from nearly $1.2 trillion to $600 billion, or a 50% decline. On the surface, you can certainly understand the reasons for concern, as the decline in holdings over the last decade supports a clean storyline.

However, the problem is the step between observation and conclusion. A lower line item for “China, Mainland” does not equal a forced sale, it does not prove intent, nor does it prove a structural exit. What it does show is a lack of understanding about the dynamics of reserve currency management, and, in the case of China, the need to protect those reserves.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post Our Take On Tariffs appeared first on RIA.

Full story here Are you the author?You Might Also Like

Investment Risk Is Underappreciated

Investment Risk Is Underappreciated

2026-01-24

🔎 At a Glance 🏛️ Market Brief – The “Greenland” Impact This week’s markets were driven by headline risk, economic uncertainty, and the early innings of earnings season. With the markets closed last Monday for the Martin Luther King holiday, U.S. equities sold off sharply on Tuesday. President Trump’s tariff threats against key European allies, …

5x Leverage Is Too Much Says The SEC

5x Leverage Is Too Much Says The SEC

2025-12-05

Wall Street’s financial engineers thought they had found yet another way to turn financial markets into casinos. The gimmick this time is with 3x, 4x, and even 5x leveraged ETFs tied to individual stocks and cryptocurrencies. The SEC just ruled against these new proposals, apparently drawing the line at 2x leverage as the rules state. …

2025-12-03

Starting in the aftermath of the 2008 financial crisis, a profound change to the Fed’s liquidity-providing role in the capital markets was underway. We can sum up the Fed regime change with a popular quip: The Fed has shifted from lender of last resort to the lender of only resort! In our articles QE Is …

HSBC Casts Doubt On OpenAI’s Future

HSBC Casts Doubt On OpenAI’s Future

2025-12-01

Per the Financial Times (LINK), HSBC has serious doubts about OpenAI’s financial wherewithal. The following bullet points outline HSBC’s assumptions, which highlight the challenging financial path OpenAI faces. The graphic below from the article shows that HSBC expects OpenAI to run a massive operating loss in the year 2030. Accordingly, they have serious concerns about …

SRF: The Fed’s Newest Liquidity Backstop In Action

SRF: The Fed’s Newest Liquidity Backstop In Action

2025-10-20

In July of 2021, after the pandemic and the liquidity issues that arose in 2019, the Fed established a new liquidity backstop. This program, the Standing Repo Facility (SRF), allows financial institutions to borrow on a collateralized basis from the Fed. Unlike the Overnight Reverse Repurchase facility (ON RRP), which allows financial institutions to park …

Rally Into Year-End: 3-Reasons To “Buy Dips”

Rally Into Year-End: 3-Reasons To “Buy Dips”

2025-10-18

🔎 At a Glance 💬 Ask a Question Have a question about the markets, your portfolio, or a topic you’d like us to cover in a future newsletter? 📩 Email: [email protected]🐦 Follow & DM on X: @LanceRoberts📰 Subscribe on Substack: @LanceRoberts We read every message and may feature your question in next week’s issue! 🏛️ …

Capitalism: The Road To Wealth And Happiness

Capitalism: The Road To Wealth And Happiness

2025-10-15

The graph below presents another opportunity to revisit how capitalism and the economic freedom it entails lead to prosperity. The scatter plot below shows the intersection of The Fraser Institute’s Economic Freedom Index with per capita GDP for 102 of the largest economies. Before analyzing the graph and what it implies for capitalism, let’s gain …

2025-10-08

It’s odd to consider, but a recession could flip our bullish outlook on bonds to bearish. It’s unusual because typically, inflation drops during a recession, leading to lower yields and higher bond prices. While we believe that if an economic downturn or recession occurs soon, the immediate effect on bonds will be favorable. However, the …

Tags: Featured,newsletter