In early November, we sounded the alarm about a recent Hindenburg Omen. Per the Commentary's summary:

Bottom line: market breadth is horrendous and will likely lead to a rotation favoring out-of-favor sectors and stocks. Thus, it’s not surprising that the Hindenburg Omen was triggered. If we continue to see more of these Omens, the threat of a drawdown grows.

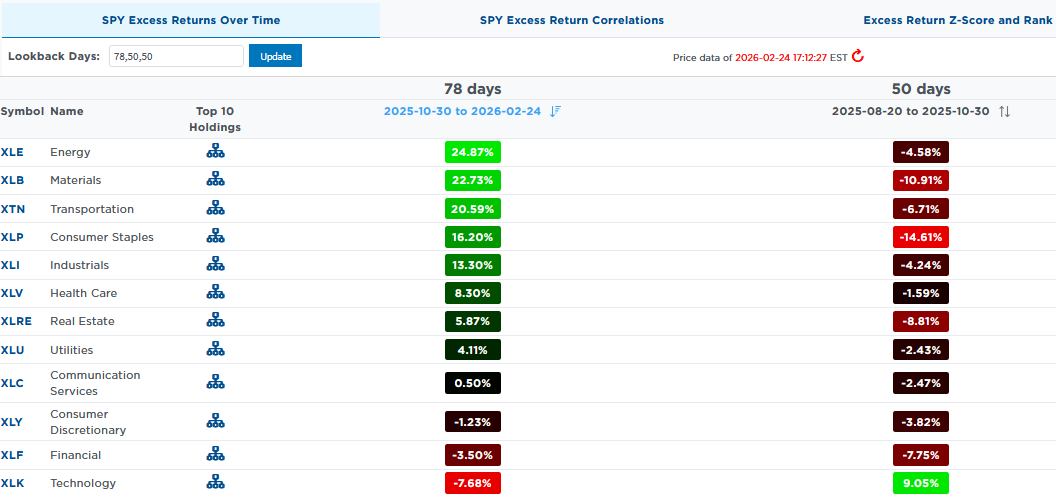

At the time, Mega-Cap stocks were grossly outperforming the market, while many sectors lagged the market. Since that Hindenburg Alarm, our expectations have come to fruition. We have, in fact, seen a "rotation favoring out-of-favor sectors and stocks." The graphic below, courtesy of SimpleVisor, shows the significant change in fortunes between sectors. The first column shows each sector's excess returns (vs. the S&P 500) since the Hindenburg Omen on October 29th. The second column shows the excess returns over the 50-day period preceding the alarm.

The Hindenburg Omen has sent 6 alarms over the last month. The last batch of Hindenburg alarms signaled drawdowns in the leaders and strong performance in the laggards. Is this Hindenburg Alarm signaling a rotation back to large-cap growth? Or might it be more ominous for the entire market? The last time this technical indicator triggered six times in a month was preceding the Pandemic crash of 2020, as we share in the Tweet of the Day.

What To Watch Today

Earnings

Economy

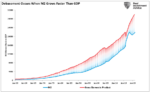

Market Trading Update

Yesterday, we discussed the potential market topping indications, we will also do a deeper dive in this weekend's #BullBearReport.

Today, I want to dig into a report from Citadel Securities discussing the current narrative that "AI will eat everything." In a February 2026 report titled "The 2026 Global Intelligence Crisis," Citadel Securities strategist Frank Flight pushes back against the prevailing AI doom narrative, arguing that fears of imminent mass labor displacement are overstated. Despite a recent market panic triggered by a viral Substack scenario predicting widespread white-collar job destruction, Citadel points to real-world data telling a different story: unemployment sits at 4.28%, software engineer job postings are up 11% year-over-year, and new business formation is rapidly expanding.

The report's central thesis is that recursive technological capability does not necessarily translate into recursive economic adoption. Technology diffusion historically follows an S-curve: A slow early uptake, accelerating growth, then a plateau. Currently, AI shows no signs of breaking this pattern. St. Louis Fed data on AI use at work reveal unexpectedly stable adoption trends with no signs of imminent displacement. Moreover, scaling AI to replace white-collar work would demand vastly more compute than currently available, and if compute costs rise above the cost of human labor for certain tasks, substitution simply won't happen.

Citadel also frames AI as a productivity shock. Fundamentally, a positive supply shock lowers costs, expands output, and raises real incomes. Every major technological revolution, from steam power to personal computing, has followed this pattern. The report cites Keynes's famous 1930 prediction of a 15-hour workweek, noting that he was right about productivity growth but wrong about its consequences: societies consumed more rather than working less because human wants proved highly elastic.

For AI to produce a sustained economic contraction, the report argues, one would need simultaneous near-total labor substitution, no fiscal or regulatory response, and unconstrained compute scaling, all an implausible combination. Historically, technological revolutions have altered the composition of work rather than eliminating it, and long-term trend growth in advanced economies has remained near 2%. AI may simply be enough to offset current headwinds from aging populations, climate change, and deglobalization.

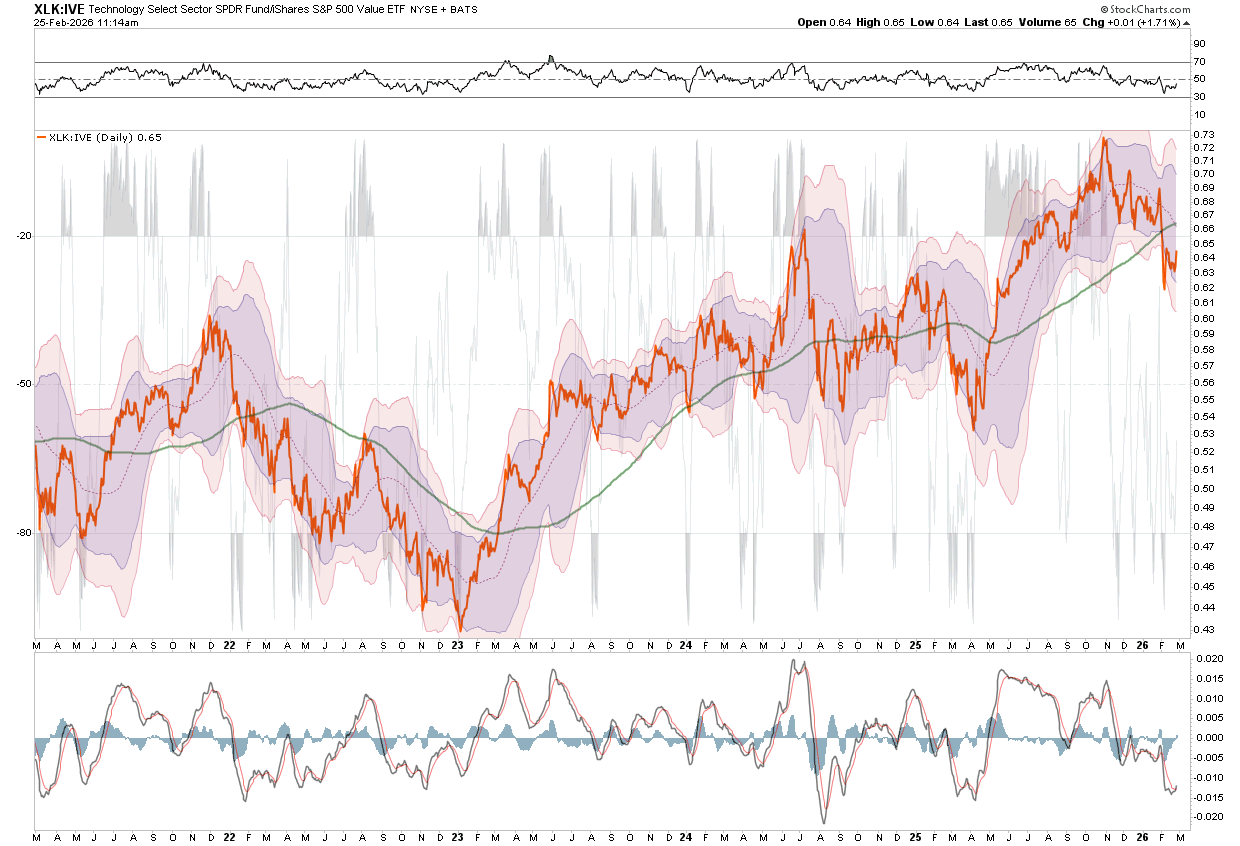

So, with this in mind, the revaluation of Technology may be providing a compelling opportunity in the future. The companies that are leading the way have low valuations, in many cases, high rates of earnings and revenue growth, and broad moats to protect them. Looking at a long-term chart of the Technology sector, such previous setups have been decent entry points for longer-term investors.

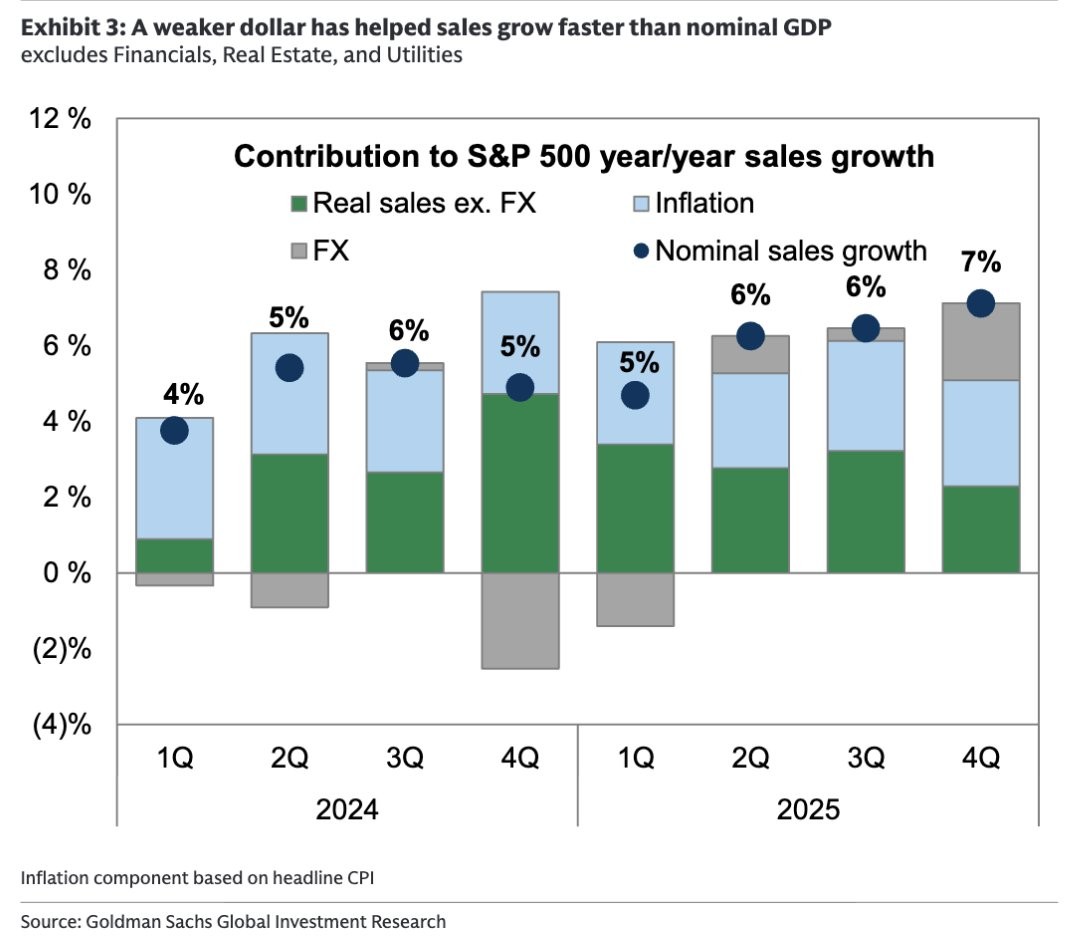

Inflation & The Dollar- Can These Earnings Tailwinds Continue?

Wall Street is forecasting a resurgence in earnings growth for the large majority of non-mega-cap S&P 500 stocks. Before blindly assuming that will be the case its worth understanding what drives earnings. Earnings are the results of sales. For many companies, sales are primarily a function of economic activity. However, as we share below, courtesy of Goldman Sachs, inflation and changes in the dollar also play meaningful, often underappreciated roles.

As shown below, inflation above pre-pandemic levels has boosted sales growth by approximately 2-3% over the past two years. Furthermore, the weakening dollar has benefited sales over the last three quarters. Looking ahead at sales and ultimately earnings, we must consider that inflation is showing signs of returning to pre-pandemic levels, and the dollar appears to be stabilizing. Assuming inflation continues to decline to the Fed’s 2% target and the dollar remains flat or even appreciates, as we suspect it may, earnings forecasts face a headwind that Wall Street analysts may not have factored in when making their optimistic beginning-of-year projections.

Software Stocks: Navigating The SaaSpocalypse

Like most narratives, the SaaSpocalypse has some truth and some falsehoods. There is also a large degree of speculation buried within it. Furthermore, the truth shouldn’t be applied broadly to all software companies and their products. In fact, AI will make some software companies more profitable and strengthen their moats. Other companies may fail as competition becomes fierce. The goal for an investor is to figure out who the winners and losers will be. Such is not a simple task, but doing so can provide significant rewards if your research proves correct.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post Hindenburg Alarm: Another Rotation Or Worse? appeared first on RIA.

Full story here Are you the author?You Might Also Like

Bond Yields May Plummet: Five Potential Catalysts

Bond Yields May Plummet: Five Potential Catalysts

2026-02-11

The top graph below, courtesy of Bloomberg, shows that the price of TLT, the 20+ year Treasury bond ETF, has been drifting sideways for the last couple of years. Often, when a security trades in a tight range over an extended period, as we see with bonds currently, a breakout from the range can be …

Fed’s Soft Landing Narrative Meets Economic Data

Fed’s Soft Landing Narrative Meets Economic Data

2025-12-20

🔎 At a Glance 💬 Ask a Question Have a question about the markets, your portfolio, or a topic you’d like us to cover in a future newsletter? 📩 Email: [email protected]🐦 Follow & DM on X: @LanceRoberts📰 Subscribe on Substack: @LanceRoberts We read every message and may feature your question in next week’s issue! 🏛️ …

Does AI Capex Spending Lead To Positive Outcomes?

Does AI Capex Spending Lead To Positive Outcomes?

2025-12-12

As someone who views corporate finance through a pragmatic lens, I’ve been closely watching the current surge in capital expenditures (capex) tied to artificial intelligence (AI). The question I’m addressing here is this: when a company spends massive amounts of free cash flow and takes on increasing debt, in this case for AI CapEx, does …

Fed QT Ends. What Does That Mean For Markets?

Fed QT Ends. What Does That Mean For Markets?

2025-11-01

🔎 At a Glance 💬 Ask a Question Have a question about the markets, your portfolio, or a topic you’d like us to cover in a future newsletter? 📩 Email: [email protected]🐦 Follow & DM on X: @LanceRoberts📰 Subscribe on Substack: @LanceRoberts We read every message and may feature your question in next week’s issue! 🏛️ …

2025-10-27

We live in what Brett Arends claimed as “The Dumbest Stock Market In History,” but I believe it is potentially the most dangerous era. That phrase is not hyperbole as it reflects structural distortion, extreme valuations, and an investor base intoxicated by momentum and narrative. The MarketWatch piece puts it bluntly: “At one level, there …

Money Supply Growth: A Thesis With A Fatal Flaw

Money Supply Growth: A Thesis With A Fatal Flaw

2025-10-24

Recently, MarketWatch ran a provocative headline: “When the world’s largest asset manager and the Bond King both agree: Run to gold, silver, and bitcoin.” The article highlighted how Larry Fink’s BlackRock and Jeffrey Gundlach, often dubbed the “Bond King,” see deficits and “money printing” as reasons for investors to escape fiat currencies and pile into …

Tags: Featured,newsletter