Over one hundred years ago, Austrian economist Ludwig von Mises discovered what causes the boom-bust business cycle.

As Mises explained, the boom is caused by central and commercial banks creating money out of thin air. This lowers interest rates, which encourages businesses to borrow this newly created money to fund capital-intensive investment projects.

The bust is caused when the money creation process slows. It is then that businesses discover there are not enough scarce resources to complete their projects, so these projects must be liquidated to allow for labor and other resources to be allocated to where they are most desired by consumers.

As a result, not only does the boom-bust business cycle cause tremendous short-term hardship, but it also lowers long-term living standards by wasting scarce capital. This is another application of the economics fact that “there is no such thing as a free lunch.” The only way to keep the boom-bust business cycle from recurring is to prevent banks from creating money out of thin air in the first place.

This explanation of the business cycle is known as the Austrian business cycle theory, in honor of Mises and those who further developed his groundbreaking theory.

One of his best students was economist Murray N. Rothbard, who summarized the theory as follows:

When the government and its central bank encourages the expansion of bank credit, it not only causes price inflation, but it also causes increasing malinvestments, specifically unsound investments in capital goods and underproduction of consumer goods. Hence, the government-induced inflationary boom not only injures consumers by raising prices and the cost of living, but also distorts production, and creates unsound investments. The government is then faced repeatedly with two basic choices: either stop its monetary and bank credit inflation, which then will necessarily be followed by a recession which serves to liquidate the unsound investments and return to a genuinely free-market structure of investment and production; or continue inflating until a runaway inflation totally destroys the currency and brings about social and economic chaos.

As Rothbard noted, governments and banks have a choice: either slow down their money creation and cause an economic bust, or accelerate their money creation and cause hyperinflation.

Thus, money supply growth holds the key to forecasting the boom-bust business cycle.

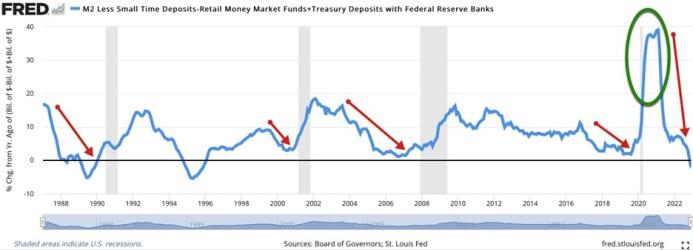

Money Supply Is Now Declining in the US

Rothbard defined the best measure of money supply, which we call Austrian money supply. It is shown in the chart below and is calculated as M2 less small time deposits and retail money market funds (since they cannot be spent on demand) plus Treasury deposits with Federal Reserve banks.

We placed red arrows on periods when money supply growth slowed before prior recessions (shaded gray). We also placed a red arrow on the current 2.2 percent decline in the money supply, which is likely to cause a recession this year. This decline follows the enormous 40 percent increase in money supply due to the Fed’s covid response in 2020 (green circle), which caused the highest inflation in forty years.

And Money Supply Growth Is Also Slowing in All Other Major Economies

Unfortunately, central banks around the world have followed the Fed’s boom-bust monetary policies.

The following chart shows Europe’s M1 money supply growth is slowing rapidly and approaching zero.

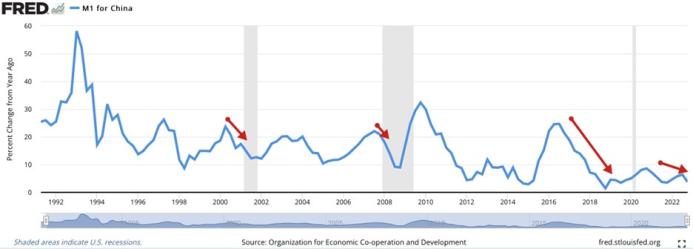

China’s M1 money supply growth is also slowing, although at a less dramatic pace, as shown below.

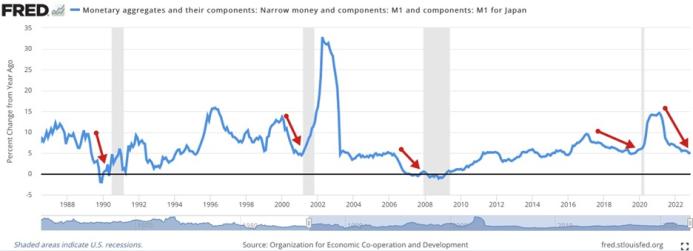

M1 money supply growth is also slowing in Japan, as the following graph shows.

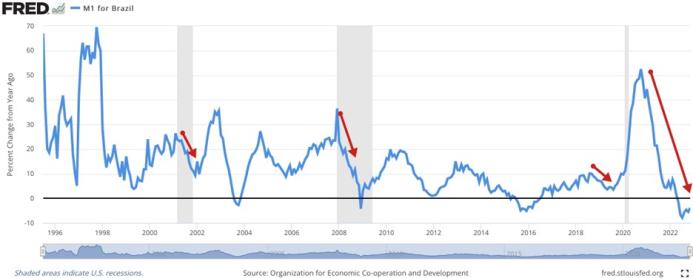

Lastly, as this chart shows, Brazil’s M1 money supply is also declining, along with that of the US.

Leading Economic Indicators Point toward a Global Recession

Due to the broad-based slowdown in money supply growth over the past year in the major economies of the world, global leading economic indicators are falling into recessionary territory.

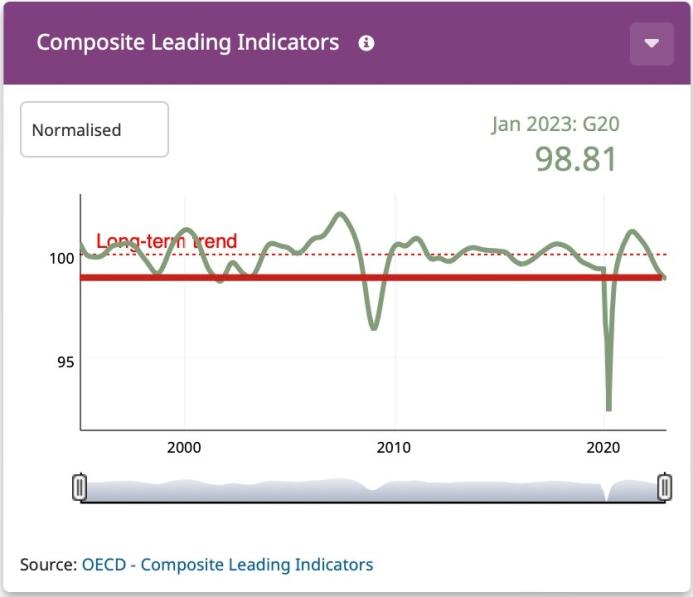

For example, the Organization for Economic Cooperation and Development (OECD) composite leading indicators for the Group of Twenty (G20, the twenty largest economies in the world, including the US, Europe, China, Japan, Brazil, India, Australia, etc.) have fallen to levels only seen during global recessions, as shown below.

Conclusion

Global recessions tend to be more severe than recessions confined just to the US since there is no major country in the world to serve as a growth engine to help revive the global economy. Based on the message currently being sent from money supply growth and other leading economic indicators, now is the time to prepare for the bust phase of the boom-bust business cycle.

Full story here Are you the author?Tags: Featured,newsletter