Charles Hugh Smith

My articles My offerMy siteAbout meMy videosMy books

Follow on:TwitterFacebookYoutubeAmazon

Extreme levels of debt and overvaluation characterize the entire global economy, and are not limited to any one nation or sector.

Financial crises come in two flavors: fraud and credit-valuation over-reach.Fraud-based financial crises may differ in particulars, but they share many traits: perverse incentives are institutionalized; the perverse incentives reward figuring out how to evade oversight via fraud, embezzlement, masking risk, etc. which are soon commoditized; regulations are gutted by insider-funded lobbying; regulators fail to do their job in hopes of getting lucrative positions in the industry they’re supposed to be regulating; reports of systemic, commoditized fraud are ignored because everyone’s getting rich, and so on.

The resolution has to 1) eliminate the perverse incentives that fueled the crisis; 2) institutionalize oversight that actually functions to limit dangerous excesses and 3) all the malinvestment / bad debt must be liquidated and the losses taken / distributed.

Correspondent David E. recently sent me this insightful outline of how the Texas Savings & Loan financial crisis arose and was slowly and painfully resolved in the 1980s:

“The S&L crisis provides an excellent example of both how to make a problem worse and how to resolve it in the end. (note: I watched this play out in Texas; some of your readers may have a different perspective).

1. Prior to the mid-1970s, S&Ls lived by the 3-6-3 rule – pay depositors 3%; make home loans at 6%; and be on the golf course at 3 o’clock. This cozy little world had been in place since the 1950s.

2. Inflation in the 70s wrecked this calculation. The loans (long term home mortgages) still paid 6%, but the S&L’s were having to pay the depositors more – often more than the 6% they were making on the loans. Bankruptcy loomed.

3. The S&L owners were some of the more prominent local business people, especially in smaller towns scattered across the US – and more importantly, in Congressional districts scattered across the US.

4. They went to Congress and said, “we’re in trouble, but if we could only invest in commercial real estate, we could grow our way out of this mess, and it won’t cost the taxpayer a dime.”

5. Congress, faced with a $50 billion problem as well as the prospect of alienating multitudes of prominent local citizens, agreed, and thus kicked the can down the road.

6. At least in Texas, this is when the “cowboys” moved in. The smarter S&L owners saw what was happening and realized the game was up. They sold their institutions to the cowboys (and the smart ones took the highest cash offer, ignoring any stock or profit-sharing).

7. The predictable and well documented abuses took off (“fiduciary pornography” in the words of one regulator afterward).

8. Things went on for a few years but were beginning to unravel even before the Saudis flooded the oil market in early 1986 and drove the price of crude down to $9.

9. Now for what was done right – if only by accident. Texas was the first to tumble, and people in other states remembered our oil boom bumper stickers. “Drive 90 and freeze a Yankee” among others. As a result, there was ZERO sympathy for Texas’ economic problems.

10. Federal regulators thus had a free hand to clean house. Even large banks were declared insolvent. Shareholders lost everything. Over 1000 bank executives went to prison. I personally know at least two who slithered free in the end, but many did not. A lawyer friend spent a couple of years in the late 1980s doing little other than foreclosing houses in Highland Park (old money Dallas).

11. It was a rough 3-4 years in Texas, but two decades of accumulated rot had been burned away, setting the stage for the economic boom that followed.

The other big factor was the tax reform of 1986. People today need to be more cognizant of what really happens when marginal rates go up to 70%. Do the rich pay more tax? NO. Instead the world becomes infested with tax shelters and other avoidance schemes, which produce tremendous waste.

In late 70s/early 80s Texas, a lot of this tax shelter money intersected with the S&L pirates in the form of commercial real estate, especially apartment complexes, in an orgy of malinvestment. I still remember the TV ads in Houston marketing yuppie-villes: gorgeous women in bikinis by the pool, and one unending party. After the bust, these complexes turned into Section 8 housing almost overnight and many remained blighted for a couple of decades before they were finally torn down.

If the next bust starts out affecting only one region, there may be a chance to do the right thing (basically, let her rip and things will settle out on their own). But that didn’t happen in 2008, and probably won’t happen next time.”

Thank you, David, for a very insightful summary of how financial crises arise and how the scale of the crisis affects the resolution: in 2008, banking had become so centralized and the fraud/leverage so extreme that the implosion of a relatively marginal slice of the mortgage market (subprime mortgages) triggered a loss of faith and liquidity that very nearly brought down the entire global financial system.

Rather than clean house, politicos bailed out the banks and regulators added new regulations that left the system essentially unchanged. As was easily predictable, the regulations increased the banks’ costs and created incentives to move mortgage origination into non-bank (and thus less regulated) entities.

Interestingly, modern financial crises seem to oscillate between fraud and over-reach: the S&L crisis resulted from the commoditization of mortgage fraud, the 2000 dot-com crash resulted from extremes of over-valuation and margin debt, the 2008 Global Financial Meltdown resulted from the globalized commoditization of securitization fraud, and now the pins are being set up for the next financial crisis triggered by extremes of credit and overvaluation.

The dot-com meltdown arose from unprecedented extremes of overvaluation for tech companies profitable and unprofitable alike. High levels of margin debt ensured that the sell-off would gather steam as punters were forced to liquidate portfolios to meet margin calls.

The dot-com meltdown was famously concentrated in the tech sector: while certainly a major part of the economy, tech and the Internet high-flyers were still a relatively modest share of total assets: all stocks, all bonds, all real estate, etc.

Sector rotation enabled capital to be preserved. As the Federal Reserve slashed interest rates, the value of bonds rose and real estate got a boost as assets flowed from stocks to housing. Simply put, not every asset crashed in unison.

|

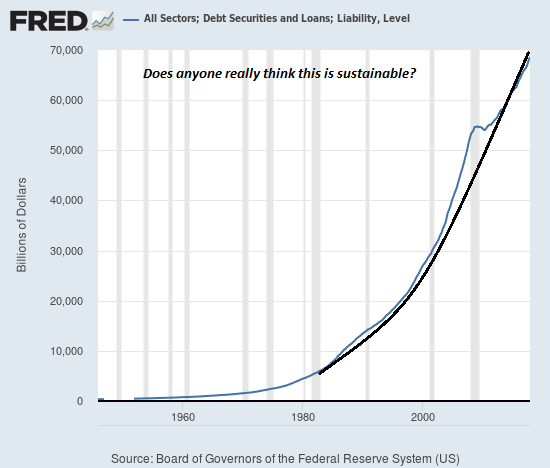

The brewing financial crisis will be different: the twin sins of extreme levels of debt and extreme overvaluation of assets now characterize corporate bonds, many sovereign bonds, stocks and real estate. Pretty much the only traditional assets that aren’t at nosebleed levels are precious metals and bat guano. (Cryptocurrencies are as yet non-traditional assets, though this may change in the next financial crisis.)

Extreme levels of debt and overvaluation characterize the entire global economy, and are not limited to any one nation or sector. When this crisis gathers steam, there will be few avenues of escape. Adding regulations won’t stop it, adding liquidity won’t stop it, waving chicken entrails and dancing the humba-humba around the MMT/Keynesian campfire won’t stop it.

Attempting to force extremes to even more extended extremes won’t stop it.

|

All Sectors, Debt Securities and Loans, Liability, 1960 - 2019 - Click to enlarge |

THREE NOTES OF NOTE:

1. I just added a new benefit for all subscribers/patrons: a monthly Q&A where I respond to your questions/topics. You get other exclusive benefits with a $1, $5 or $10/month patronage via patreon.com.

2. Resistance, Revolution, Liberation: A Model for Positive Change is on sale this month: $4.95 Kindle edition, $9.95 print edition, a 33% discount.

3. Did you know there are 3 new audiobooks available now?

My new book is The Adventures of the Consulting Philosopher: The Disappearance of Drake. For more, please visit the book's website.

Full story here

Are you the author?

At readers' request, I've prepared a biography. I am not confident this is the right length or has the desired information; the whole project veers uncomfortably close to PR. On the other hand, who wants to read a boring bio? I am reminded of the "Peanuts" comic character Lucy, who once issued this terse biographical summary: "A man was born, he lived, he died." All undoubtedly true, but somewhat lacking in narrative.

Tags: newsletter