| In ancient times, like as far back as the 1990s, housing prices grew roughly inline with inflation rates because they were generally set by supply and demand forces determined by a market where buyers mostly just bought houses so they could live in them. Back in those ancient days, a more practical group of world citizens saw their homes as a place to raise a family rather that just another asset class that should be day traded to satisfy their gambling habits.

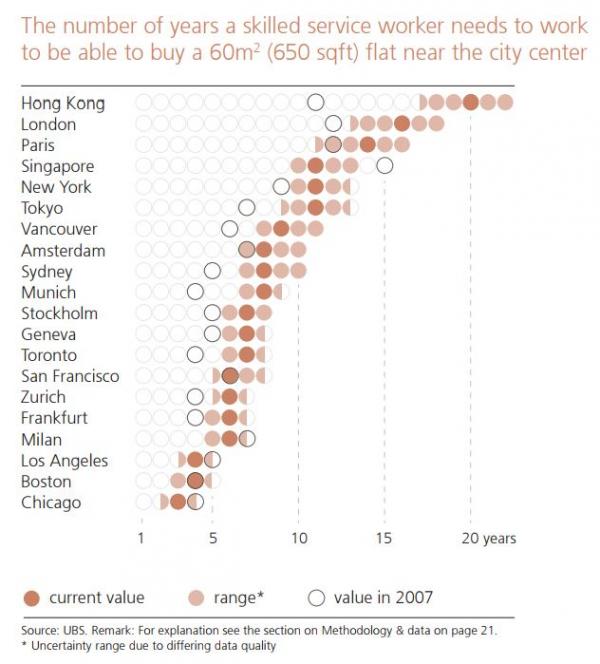

But, thanks to the efforts of global central banks, the days where home prices roughly reflected the ability of the marginal local buyer to afford those homes, is long gone. As a general rule of thumb, a house was historically considered “affordable” if it was less than 2.5 times a family’s annual gross income…by those metrics, at least according to the UBS Global Real Estate Bubble Index released earlier today, the median buyer can’t afford housing in pretty any of the major cities of the world.

|

- Click to enlarge |

Meanwhile, the price-to-rent ratios below further reflect the insanity of global real estate bubbles where yields have gradually trended toward 0% as speculators are once again utilizing cheap mortgages to bet on price appreciation with complete disregard for underlying fundamentals.

Zurich and Munich have the peak price-to-rent ratios, followed by Stockholm and Vancouver. Extremely high multiplies indicate an undue dependence of housing prices on low interest rates. Overall, half of the covered cities have price-to-rent multiples above 30. House prices in all these cities are vulnerable to a sharp correction should interest rates rise.

Price-to-rent values below 20 are found only in the US cities of Los Angeles, Boston and Chicago. Their low multiplies reflect, among other things, higher interest rates and a relatively mildly regulated rental market. Conversely, rental laws in France, Germany, Switzerland and Sweden are strongly protenant, preventing rentals from reflecting true market levels.

But stratospheric price-to-rent multiples reflect not only interest rates and rental market regulation but expectations of rising prices, for example in Hong Kong and Vancouver. Investors anticipate being compensated with capital gains for overly low rental yields. If such hopes do not materialize and expectations deteriorate, homeowners in markets with high price-to-rent multiples are likely to suffer significant capital losses.

But there’s probably nothing to worry about…everything worked out just fine in 2009.

Full story here Are you the author?Tags: Business,central banks,Economic bubble,economy,Finance,France,Futures contract,Germany,Hong Kong,money,newslettersent,Real Estate,Real estate bubble,Switzerland,Zurich