Stock MarketsEM should trade firmer this week on news over the weekend that the FBI said its conclusion on Clinton’s emails remained unchanged. That should lift the cloud of suspicion that grew when the FBI said new emails had been uncovered. With risk appetite likely to rebound a bit, the Mexican peso should benefit the most as the week gets under way.

The central banks of Korea, the Philippines, Thailand, Poland, and Peru all meet, and none are expected to change policy. Still, individual country risk matters. The Turkish lira hit a record low last week on intensifying political risks, and weakness should continue. More China data for October should confirm that the economy is stabilizing in Q4.

|

Stock Markets Emerging Markets November 02 Source: Economist.com - Click to enlarge |

TaiwanTaiwan reports October trade Monday. Exports are expected to rise 2.6% y/y, while imports are expected to rise 5.7% y/y. Taiwan reports October CPI Tuesday, which is expected to rise 0.5% y/y vs. 0.3% in September. The central bank does not have an explicit inflation target. However, low inflation will allow the central bank to ease again if needed. Czech RepublicCzech Republic reports September retail sales Monday, which are expected to rise 6.0% y/y vs. 11.1% in August. It then reports September industrial and construction output as well as trade Tuesday. October CPI will be reported Wednesday, which is expected to rise 0.7% y/y vs. 0.5% in September. While this remains below the 1-3% target range, inflation has been creeping higher and has led the central bank to become more confident that the CZK floor will end around mid-2017.

ChileChile reports October trade Monday. It then reports October CPI Tuesday. Inflation has been within the 2-4% target range for several months, but the central bank is likely to remain cautious for now. Next policy meeting is November 17, no change is expected then. The weak economy argues for an easing cycle, but that is a 2017 story.

ChinaChina reports October trade Tuesday. Exports are expected to contract -6.0% y/y, while imports are expected to contract -1.8% y/y. It then reports October CPI and PPIWednesday, which are expected to rise 2.1% y/y and 0.9% y/y, respectively. Rising price pressures and concerns about asset bubbles should keep the PBOC on hold for now.

TurkeyTurkey reports September IP Tuesday. It then reports September current account Friday. The external accounts are worsening even as the economy remains sluggish and inflation remains high. The fundamental backdrop is worsening, which when taken into conjunction with political risks argues for continue underperformance of Turkish assets.

HungaryHungary reports October CPI Tuesday, which is expected to rise 0.8% y/y vs. 0.6% in September. Inflation remains below the 2-4% target range, which gives the central bank leeway to ease further as it sees fit. It also reports September IP that day, which is expected to rise 3.1% y/y vs. 3.5% in August. September trade will be reported Wednesday. Central bank minutes will also be released that day.

ThailandBank of Thailand meets Wednesday and is expected to keep rates steady at 1.5%. CPI rose 0.3% y/y in October, which remains well below the 1-4% target range. However, the economy remains robust and so the BOT sees no need to ease right now. If the economy slows, low inflation gives the central bank leeway to ease as needed.

PolandNational Bank of Poland meets Wednesday and is expected to keep rates steady at 1.5%. CPI fell -0.2% y/y in October, the shallowest deflation since July 2014. Outright inflation seems likely in the coming months, which should keep the central bank on hold whilst looking for an eventual rate hike.

BrazilBrazil reports October IPCA inflation Wednesday. It then reports September retail sales Thursday. Inflation is slowly moving towards the 2.5-6.5% target range, but the pace will keep the central bank cautious for now. Next COPOM meeting is November 30, and most are looking for another 25 bp cut to 13.75%.

MexicoMexico reports October CPI Wednesday. CPI is moving steadily higher, but remains within the 2-4% target range. Barring another collapse in the peso, we expect no further tightening ahead. Next policy meeting is November 17, no change expected then. Mexico then reports September IP Friday.

PhilippinePhilippine central bank meets Thursday and is expected to keep rates steady at 3%. CPI rose 2.3% y/y in October, which remains in the 2-4% target range. Rising inflation and peso weakness has likely ended the central bank’s easing cycle. September trade will also be reported that day.

South AfricaSouth Africa reports September manufacturing production Thursday, which is expected to rise 0.8% y/y vs. 2.2% in August. Markets have been buoyed by signs that President Zuma may be pushed out. However, we caution that the fundamental backdrop remains poor.

PeruPeru central bank meets Thursday and is expected to keep rates steady at 4.25%. CPI edged unexpectedly higher to 3.4% y/y in October. This moves inflation further away from the 1-3% target range. While further tightening is unlikely, this will most likely delay the start of the easing cycle.

KoreaBank of Korea meets Friday and is expected to keep rates steady at 1.25%. CPI rose 1.3% y/y in October, the highest since February but still below the 2% target. For now, the BOK is likely to keep rates steady, especially in light of the rising political uncertainty.

|

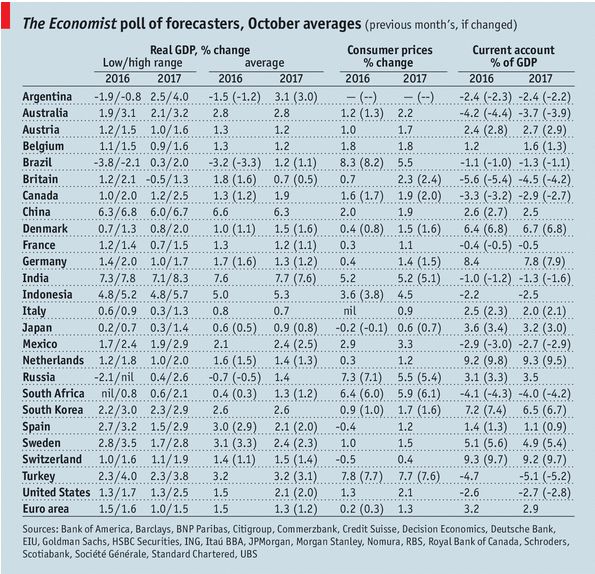

GDP, Consumer Inflation and Current Accounts Source: Economist.com - Click to enlarge |

Graphs and additional information added by the snbchf team.

Full story here Are you the author?Win Thin is a senior currency strategist with over fifteen years of investment experience. He has a broad international background with a special interest in developing markets. Prior to joining BBH in June 2007, he founded Mandalay Advisors, an independent research firm that provided sovereign emerging market analysis to institutional investors. He received an MA from Georgetown University in 1985 and a B.A. from Brandeis University 1983. Feel free to contact the Zurich office of BBH

Tags: Emerging Markets,newslettersent,win-thin