Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Is It Being Demanded?

Is It Being Demanded?29 May 2022

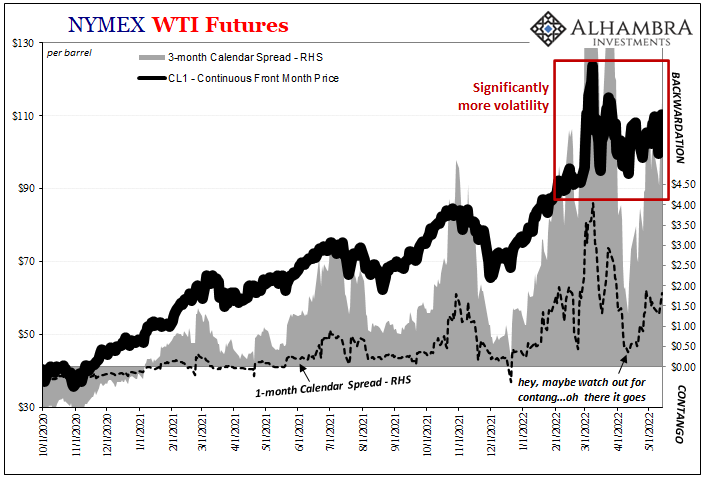

Crude Contradictions Therefore Uncertainty And Big Volatility18 May 2022

Playing Dominoes19 Dec 2021

Inflation Hysteria #2 (WTI)

Inflation Hysteria #2 (WTI)12 Dec 2020

Extending the Summer Slowdown20 Nov 2020

Counting The Corroborated Stall, Not The Coming Lawfare Election Mess6 Nov 2020

What’s Going On, And Why Late August?29 Oct 2020

Inflation Karma15 Sep 2020

Bottleneck In Japanese9 Sep 2020

A Big One For The Big “D”13 May 2020

COT Black: No Love For Super-Secret Models

COT Black: No Love For Super-Secret Models1 May 2020

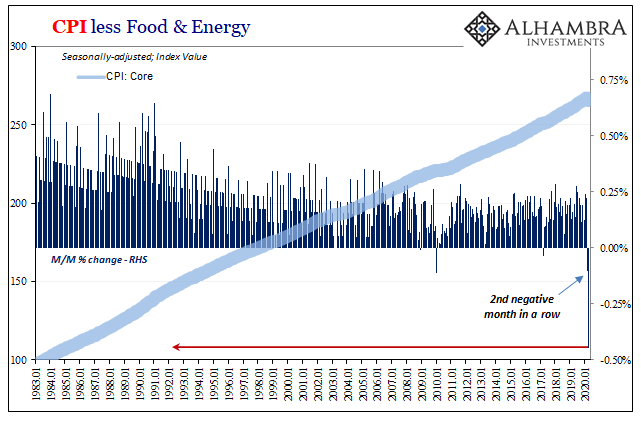

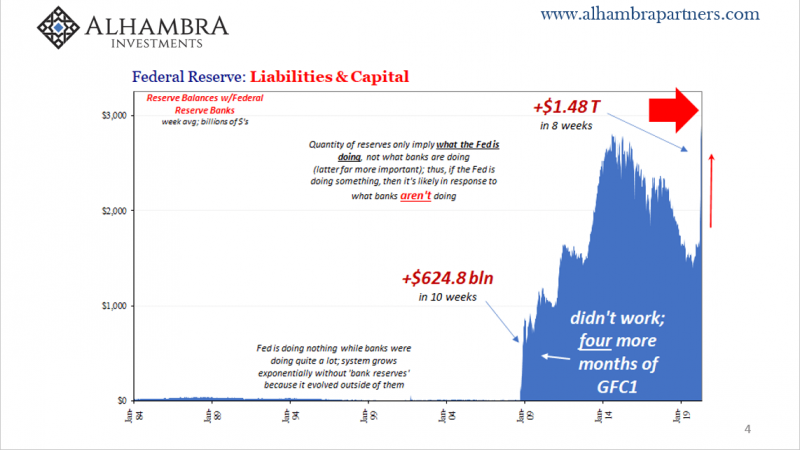

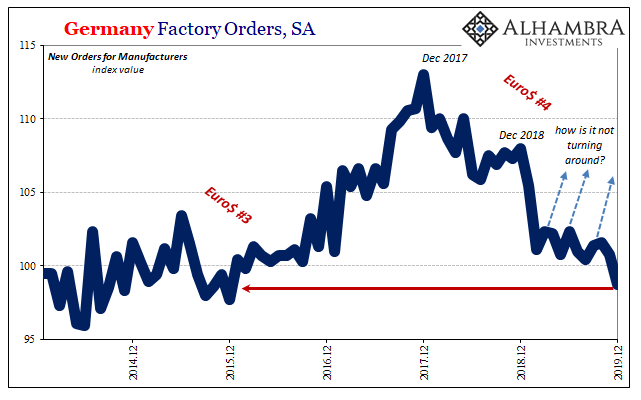

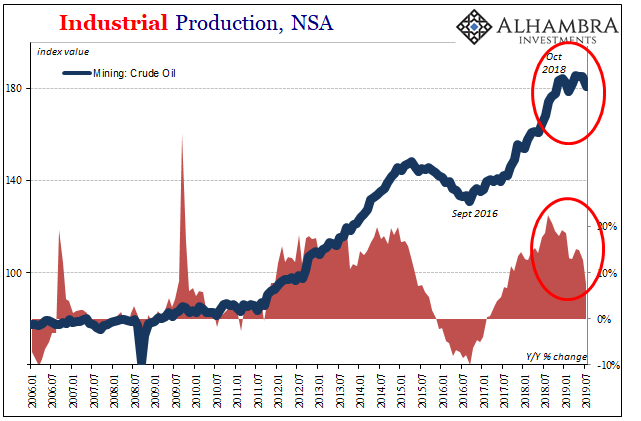

COT Black: German Factories, Oklahoma Tank Farms, And FRBNY9 Feb 2020

US Industrial Downturn: What If Oil and Inventory Join It?16 Aug 2019

Inflation Falls Again, Dot-com-like16 Feb 2019

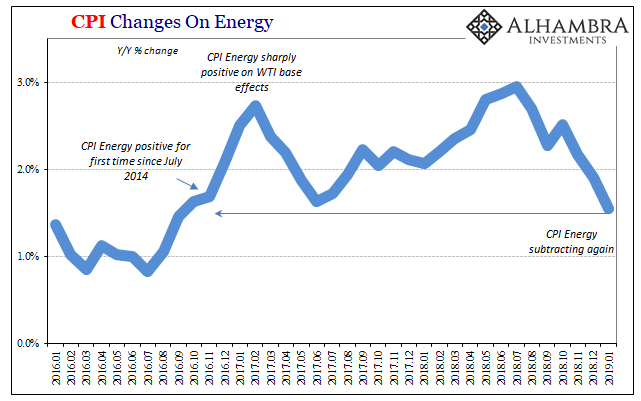

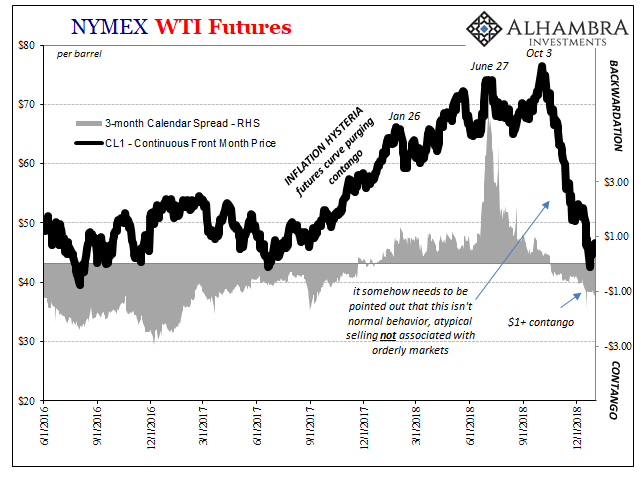

Nothing To See Here, It’s Just Everything4 Jan 2019

Wasting the Middle: Obsessing Over Exits28 Dec 2018

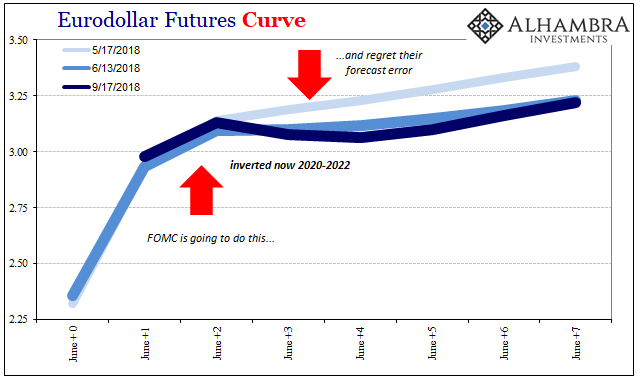

Eurodollar Futures: Powell May Figure It Out Sooner, He Won’t Have Any Other Choice20 Nov 2018

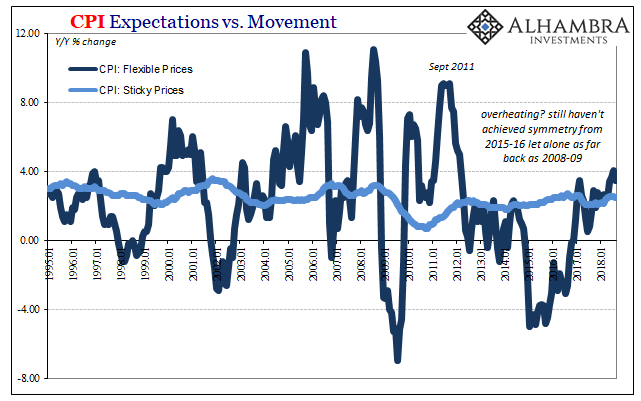

Downslope CPI16 Sep 2018

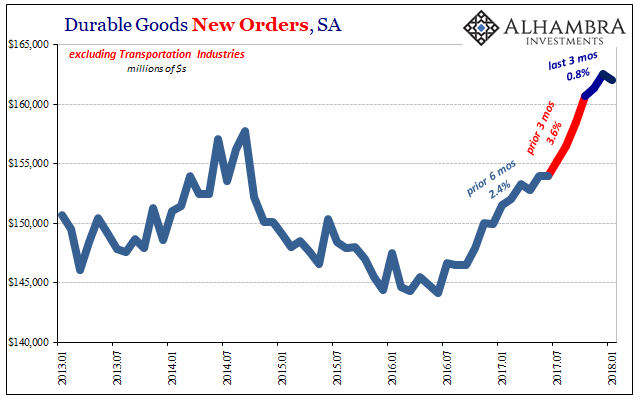

Durable and Capital Goods, Distortions Big And Small4 Mar 2018

Reduced Trade Terms Salute The Flattened Curve10 Dec 2017