Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: A Most Unusual Economy

Weekly Market Pulse: A Most Unusual Economy11 Jul 2022

Another Month Closer To Global Recession26 May 2022

Worry Walls Don’t Explain Repeated Falls

Worry Walls Don’t Explain Repeated Falls9 Apr 2022

All Eyes On Inventory24 Sep 2021

ISM’s Nasty Little Surprise Isn’t Actually A Surprise7 Jul 2021

There’s Two Sides To Synchronize3 Mar 2021

Where Is It, Chairman Powell?15 Nov 2020

Counting The Corroborated Stall, Not The Coming Lawfare Election Mess6 Nov 2020

Inflation Karma15 Sep 2020

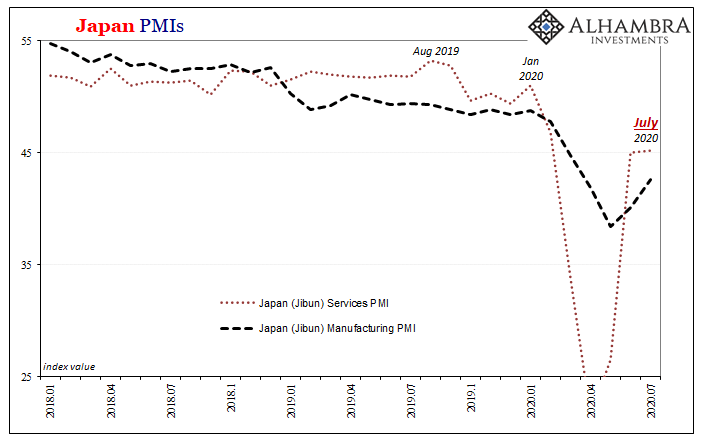

A Japanese Stall?24 Jul 2020

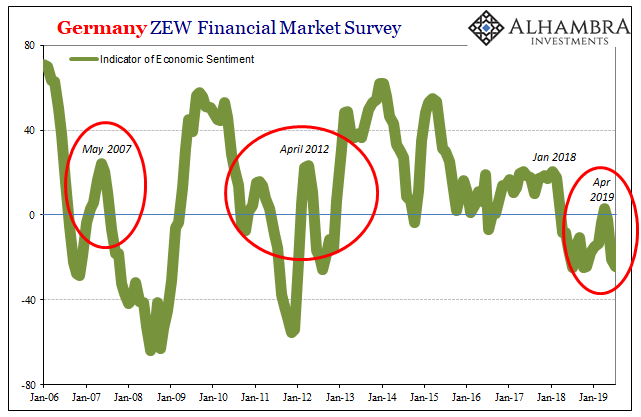

Latest European Sentiment Echoes Draghi’s Last Take On Global Economic Risks19 Dec 2019

All Signs Of More Slack7 Dec 2019

You Have To Try Really Hard Not To See It7 Nov 2019

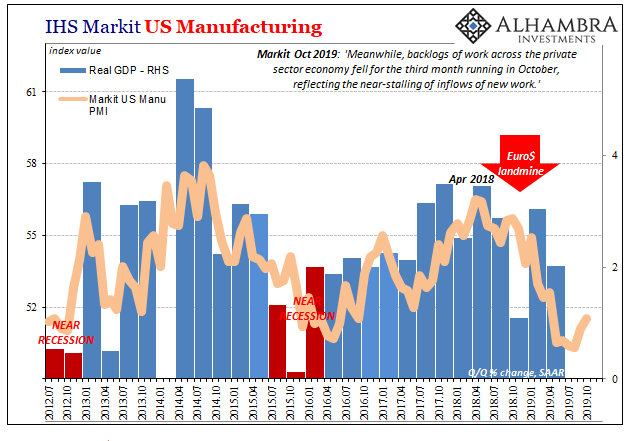

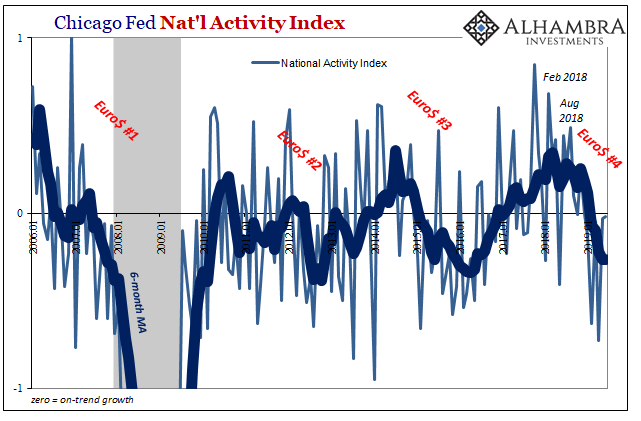

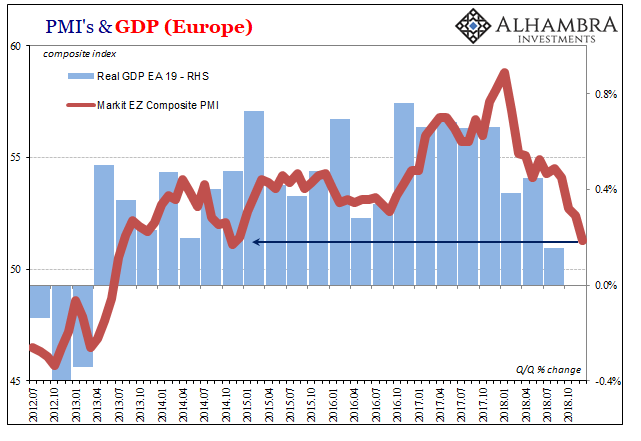

More Synchronized, More Downturn, Still Global3 Nov 2019

Somehow Still Decent European Descent

Somehow Still Decent European Descent28 Oct 2019

More Down In The Downturn25 Oct 2019

No Longer Hanging In, Europe May Have (Been) Broken Down24 Sep 2019

US Economic Crosscurrents Reach the 50 Mark27 Jul 2019

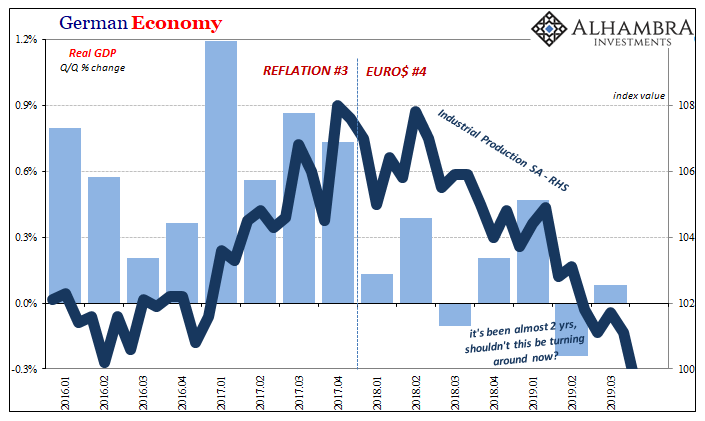

Germany Struggles On25 Jul 2019

Just In Time For The Circus26 Dec 2018