Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

What The PMIs Aren’t Really Saying, In China As Elsewhere

What The PMIs Aren’t Really Saying, In China As Elsewhere1 Jul 2020

Copper Confirmed4 Sep 2019

China’s Global Slump Draws Closer4 Dec 2018

How Global And Synchronized Is A Boom Without China?4 Feb 2018

Three Years Ago QE, Last Year It Was China, Now It’s Taxes13 Dec 2017

Bonds And Soft Chinese Data4 Nov 2017

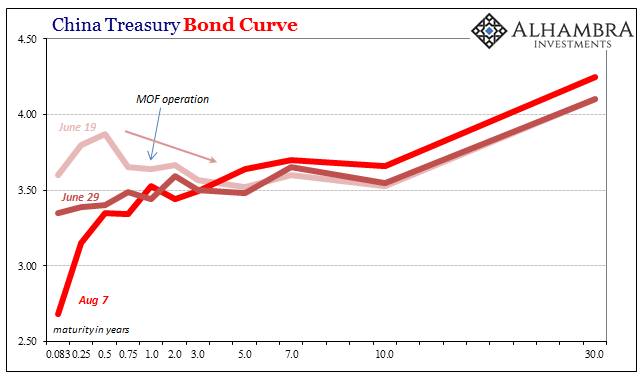

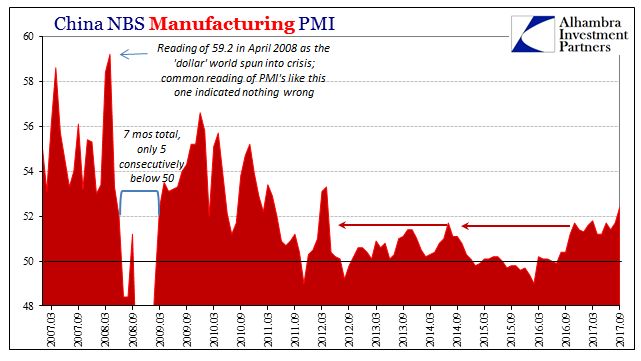

Noisy PMI’s In China14 Oct 2017

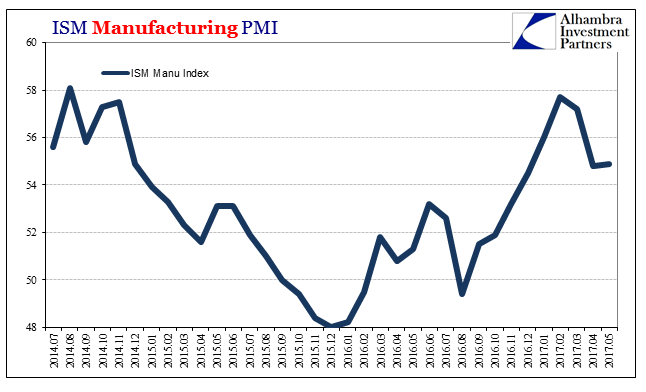

Dollars And Sent(iment)s9 Jun 2017

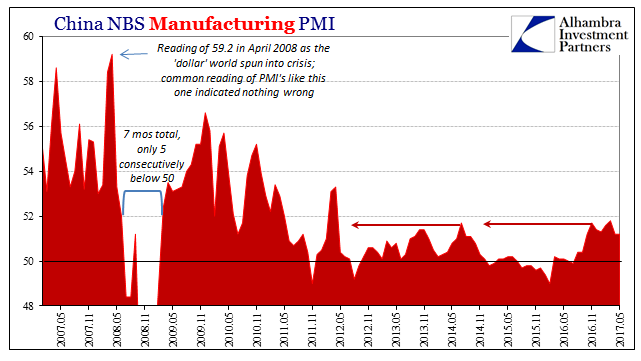

Pay No Attention To 508 Jun 2017