Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: The Sober Spending Of Drunken Sailors

Weekly Market Pulse: The Sober Spending Of Drunken Sailors24 Jun 2024

Retail Sales Data Suggests A Strong Consumer Or Does It

Retail Sales Data Suggests A Strong Consumer Or Does It26 Apr 2024

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?15 Apr 2024

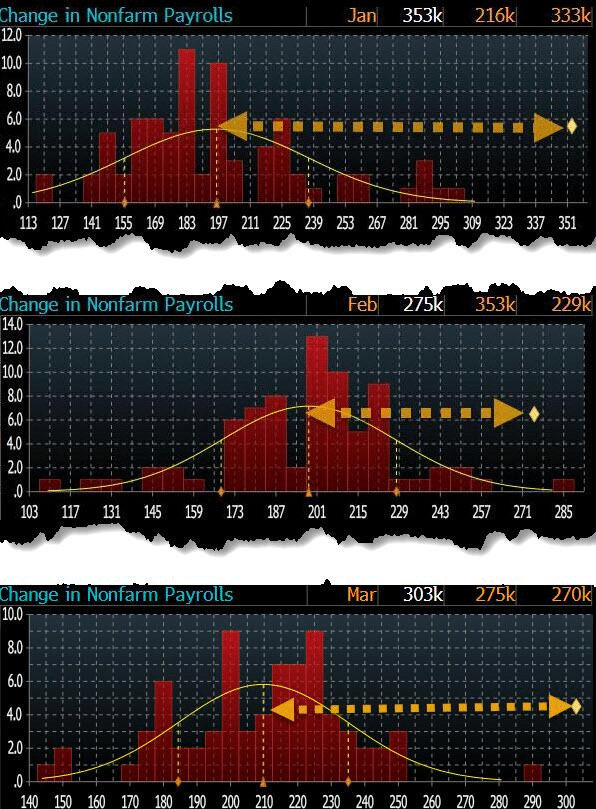

Immigration And Its Impact On Employment

Immigration And Its Impact On Employment12 Apr 2024

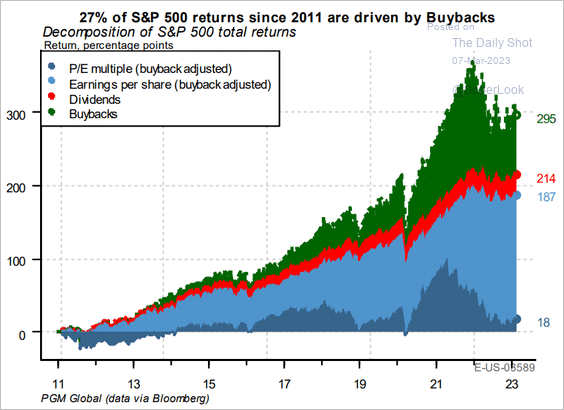

Blackout Of Buybacks Threatens Bullish Run

Blackout Of Buybacks Threatens Bullish Run19 Mar 2024

Gold Outlook 2024 Brief

Gold Outlook 2024 Brief12 Mar 2024

Digital Currency And Gold As Speculative Warnings

Digital Currency And Gold As Speculative Warnings12 Mar 2024

Presidential Elections And Market Corrections

Presidential Elections And Market Corrections10 Mar 2024

Valuation Metrics And Volatility Suggest Investor Caution

Valuation Metrics And Volatility Suggest Investor Caution5 Mar 2024

Fed Chair Powell Just Said The Quiet Part Out Loud

Fed Chair Powell Just Said The Quiet Part Out Loud16 Feb 2024

US Dollar Offered Ahead of Employment Data after US 10-year Yield Set New Low for the Year

US Dollar Offered Ahead of Employment Data after US 10-year Yield Set New Low for the Year2 Feb 2024

Weekly Market Pulse: Monetary Policy Is Hard

Weekly Market Pulse: Monetary Policy Is Hard6 Nov 2023

Dollar Eases, Stocks and Bonds Advance

Dollar Eases, Stocks and Bonds Advance22 Aug 2023

Weekly Market Pulse: Look Up In The Sky! It’s A UFO! Or Not!

Weekly Market Pulse: Look Up In The Sky! It’s A UFO! Or Not!13 Feb 2023

Ep 52 – Jeff Snider: Solving the Eurodollar Puzzle

Ep 52 – Jeff Snider: Solving the Eurodollar Puzzle24 Jan 2023

Weekly Market Pulse: A Fatal Conceit

Weekly Market Pulse: A Fatal Conceit24 Jan 2023

Weekly Market Pulse: Currency Illusion

Weekly Market Pulse: Currency Illusion28 Nov 2022

How to Build and Destroy a Pension Fund System in 22 Easy Steps

How to Build and Destroy a Pension Fund System in 22 Easy Steps26 Oct 2022

Weekly Market Pulse: The Real Reason The Fed Should Pause

Weekly Market Pulse: The Real Reason The Fed Should Pause11 Oct 2022

Ed Steer Gold And Silver – We Ain’t Seen Nothing Yet!

Ed Steer Gold And Silver – We Ain’t Seen Nothing Yet!5 Oct 2022

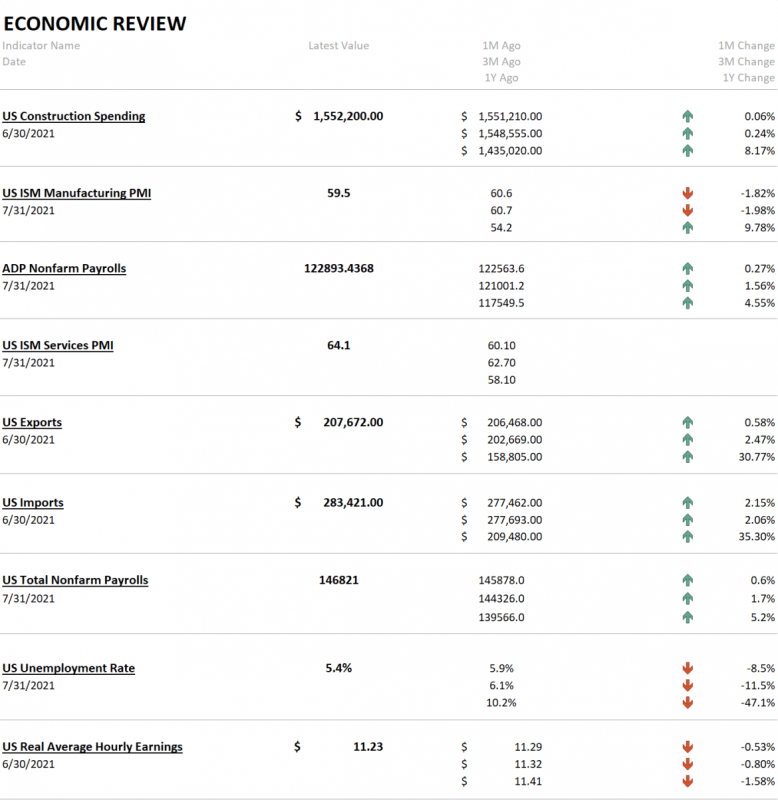

Quantitative Easing: A Boon or Curse?

2021-07-24

by Stephen Flood

2021-07-24

Read More »