Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Eurodollar Futures Interpretation Is Everywhere

Eurodollar Futures Interpretation Is Everywhere1 Jul 2022

Can’t Blame COVID For This One3 Jun 2022

A Clear Balance of Global Inflation Factors30 Jun 2021

Copper Corroding PPI17 Jun 2021

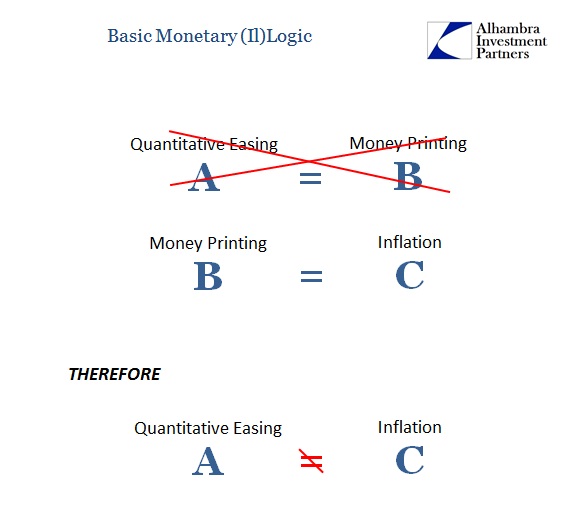

Even The People ‘Printing’ The ‘Money’ Aren’t Seeing It7 Feb 2021

Meanwhile, Outside Today’s DC5 Nov 2020

It’s Not That There Might Be One, It’s That There Might Be Another One1 Feb 2019

ECB (Data) Independence15 Sep 2018

Brent’s Back In A Big Way, Still ‘Something’ Missing12 Jun 2018

What Really Happened In Europe10 May 2018

Globally Synchronized What?31 Jan 2018

Europe Is Booming, Except It’s Not7 Nov 2017

Global Inflation Continues To Underwhelm19 Oct 2017

Data Dependent: Interest Rates Have Nowhere To Go18 Aug 2017

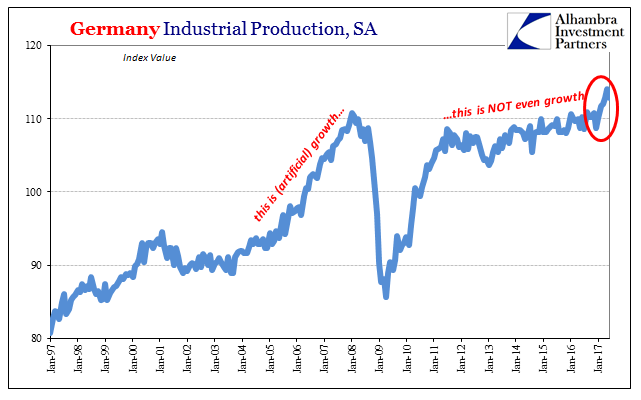

Industrial Production: Irreführende Statistiken11 Aug 2017

Global Manufacturing PMI’s, Inflation and CPI: Some Global Odd & Ends9 Jul 2017

Repeat 2014: Praying Again To The God of ‘Global Growth’22 Jun 2017

16 Jun 2017

Ultra-Loose Terminology, Not Policy8 Apr 2017

Consensus Inflation (Again)4 Apr 2017