Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

USD Looks Oversold on Intraday Basis Ahead of a Possible Risk-Off North American Session

USD Looks Oversold on Intraday Basis Ahead of a Possible Risk-Off North American Session26 Jan 2024

China Surprises While the Dollar Begins Week Softer21 Aug 2023

Week Ahead: More Evidence US Consumption and Output are Expanding, and RBNZ and Norges Bank to Hike13 Aug 2022

Macro and Prices: Sentiment Swings Between Inflation and Recession14 May 2022

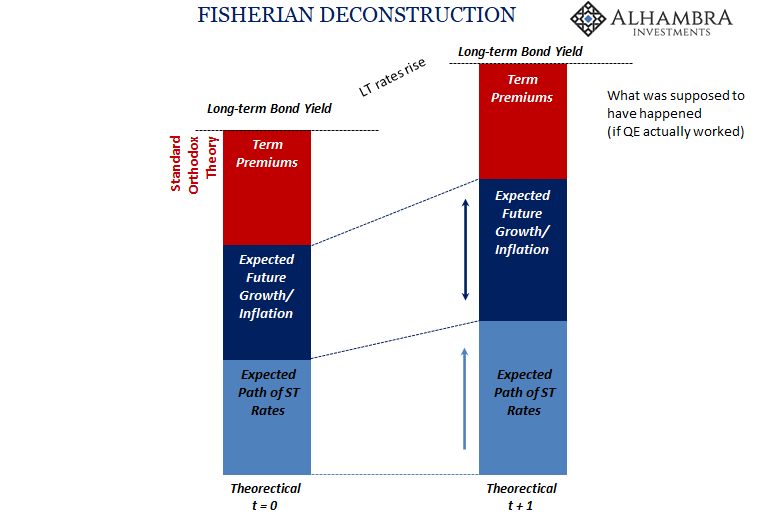

Good Time To Go Fish(er)ing Around The Yield Curve21 Jan 2022

The Chagrin of Beijing and the Problem of Time19 Dec 2021

US Retail Sales and Industrial Output to Accelerate; China not so Much13 Nov 2021

Week Ahead: The First Look at US and EMU Q3 GDP and more Tapering by the Bank of Canada23 Oct 2021

FX Daily, April 29: US GDP: The V29 Apr 2021

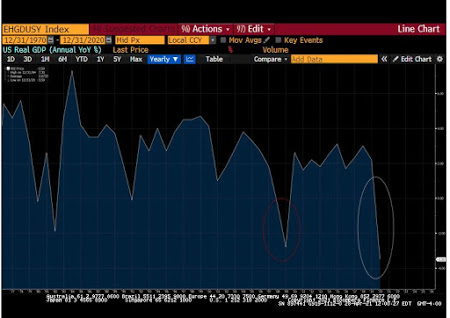

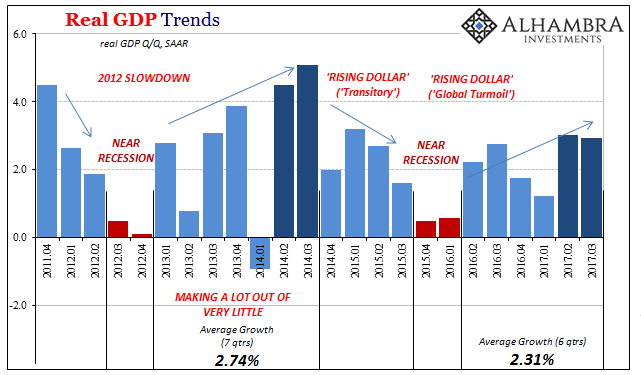

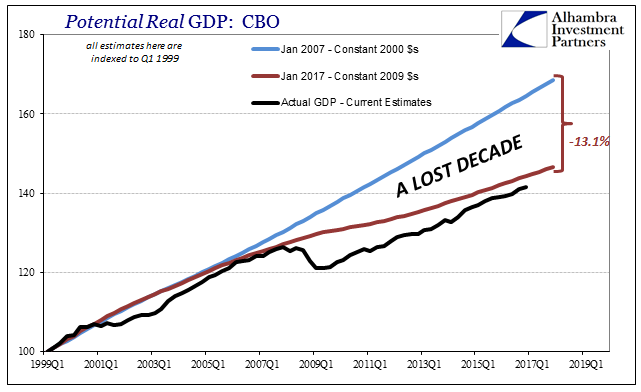

Strong Growth? Q3 GDP Only Shows How Weak 2017 Has Been3 Nov 2017

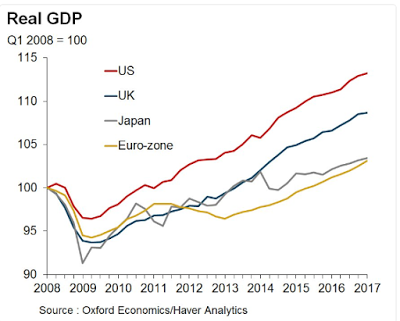

Great Graphic: Selected GDP Performance since 2008 and Policy22 Jun 2017

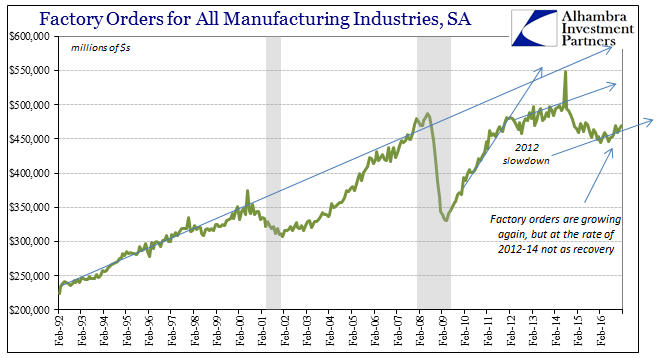

Manufacturing Back To 20147 Mar 2017

The Stinking Politics of It All22 Feb 2017

US GDP Misses, but Final Domestic Sales Accelerate27 Jan 2017

Some Thoughts on Q3 US GDP30 Nov 2016

Yellen and Fischer Still Singing from the Same Song Book28 Oct 2016

Demographics and a New Old Paradigm23 Oct 2016