Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

DZ BANK and KfW Complete German Digital Bond Issuance via Blockchain

DZ BANK and KfW Complete German Digital Bond Issuance via Blockchain26 Mar 2026

13 Jan 2026

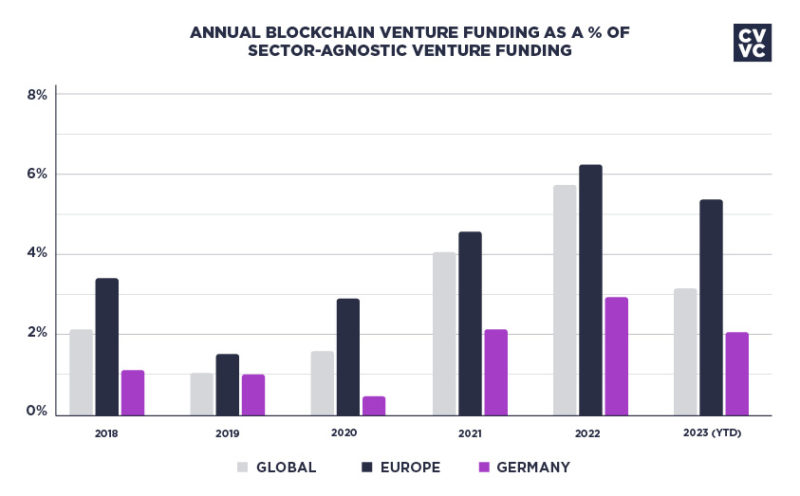

German Blockchain Funding Falls to Four-Year Low Despite $9.3B Venture Growth

German Blockchain Funding Falls to Four-Year Low Despite $9.3B Venture Growth19 Nov 2025

4 Sep 2025

Fall of French Government Does Not Roil the Markets and a BOJ Dove did not Rule out Rate Hike this Month

Fall of French Government Does Not Roil the Markets and a BOJ Dove did not Rule out Rate Hike this Month5 Dec 2024

French Government on Precipice, Presses Euro Lower

French Government on Precipice, Presses Euro Lower2 Dec 2024

Trump’s Tariff Talks Wobble Forex Market, Close Neighbors Suffer Most

Trump’s Tariff Talks Wobble Forex Market, Close Neighbors Suffer Most26 Nov 2024

The Dollar’s Surge Continues

The Dollar’s Surge Continues14 Nov 2024

Searching for Direction

Searching for Direction8 Nov 2024

Serenity Now

Serenity Now7 Nov 2024

Greenback Consolidates

Greenback Consolidates22 Oct 2024

Risk of 50 bp cut by the Fed Tomorrow Keeps the Greenback on the Defensive

Risk of 50 bp cut by the Fed Tomorrow Keeps the Greenback on the Defensive17 Sep 2024

Siemens Launches €300 Million Digital Bond on Blockchain

Siemens Launches €300 Million Digital Bond on Blockchain10 Sep 2024

The Market Discounts around a 40% Chance of not One but Two 50 bp Cuts in last Three FOMC Meetings of the Year Ahead of Jobs Report

The Market Discounts around a 40% Chance of not One but Two 50 bp Cuts in last Three FOMC Meetings of the Year Ahead of Jobs Report6 Sep 2024

US Benchmark Payroll Revisions Over-Hyped? Dollar may Benefit from Buying on Fact after Being Sold on Rumors

US Benchmark Payroll Revisions Over-Hyped? Dollar may Benefit from Buying on Fact after Being Sold on Rumors21 Aug 2024

BOJ Offers Verbal Support, Extends the Yen’s Pullback

BOJ Offers Verbal Support, Extends the Yen’s Pullback7 Aug 2024

Greenback Catches a Bid

Greenback Catches a Bid18 Jun 2024

Double Whammy: US CPI and Federal Reserve

Double Whammy: US CPI and Federal Reserve12 Jun 2024

Powell, PPI, and US Tariff Announcement on China Featured

Powell, PPI, and US Tariff Announcement on China Featured14 May 2024

Will the Market Push the Dollar Above JPY152 as Japanese Prime Minister Heads to the US?

Will the Market Push the Dollar Above JPY152 as Japanese Prime Minister Heads to the US?8 Apr 2024