Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

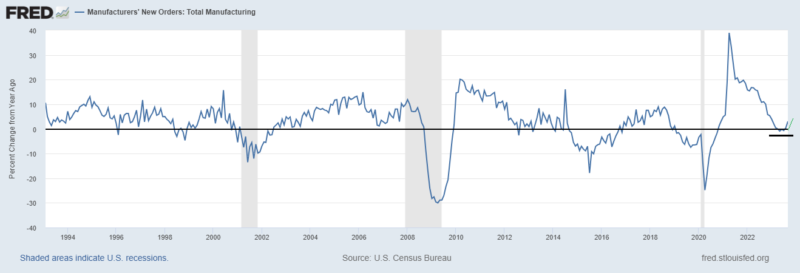

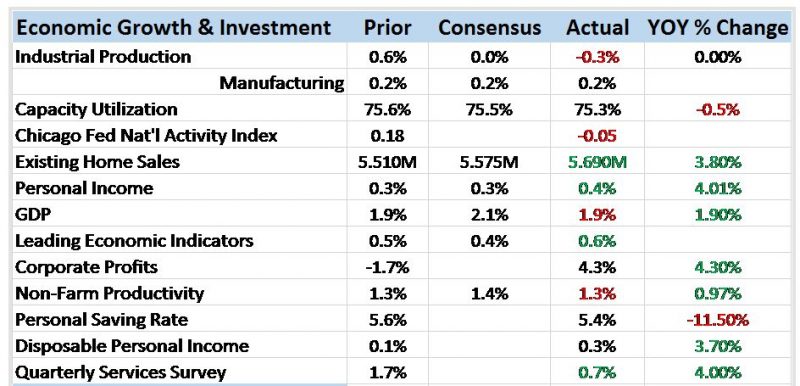

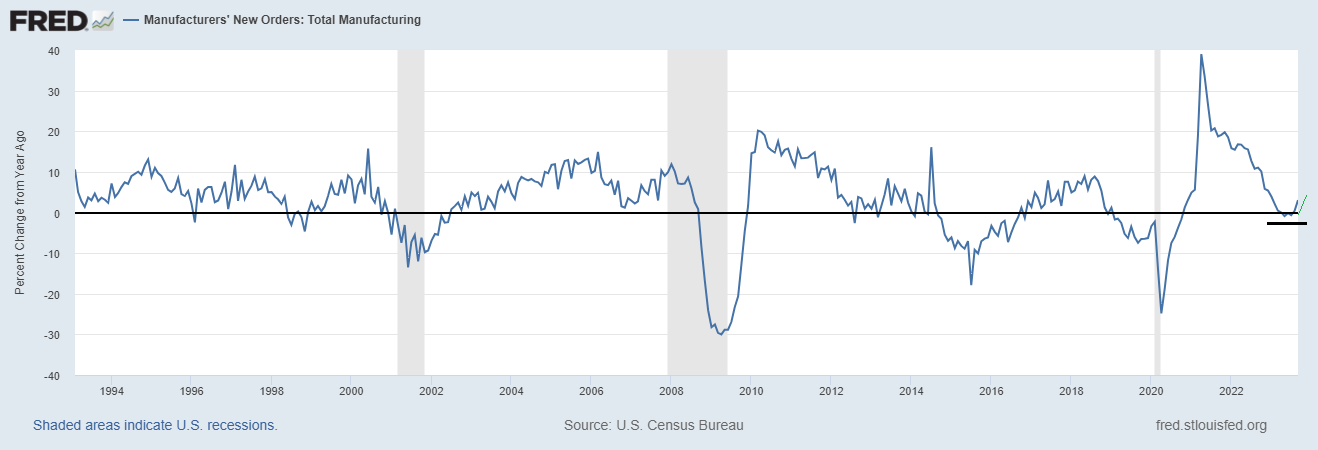

Macro: Factory Orders — revision

Macro: Factory Orders — revision2 Nov 2023

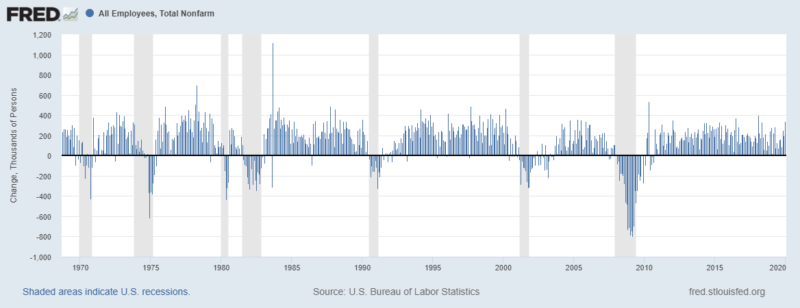

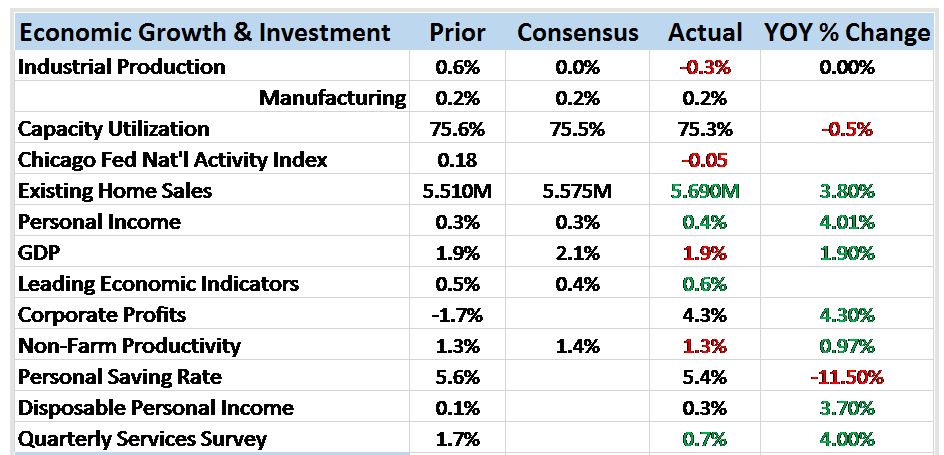

Weekly Market Pulse: A Most Unusual Economy

Weekly Market Pulse: A Most Unusual Economy11 Jul 2022

GDP Red Flag31 Oct 2021

The Enormously Important Reasons To Revisit The Revisions Already Several Times Revisited29 Oct 2021

With No Second Half Rebound, Confirming The Squeeze29 Jan 2020

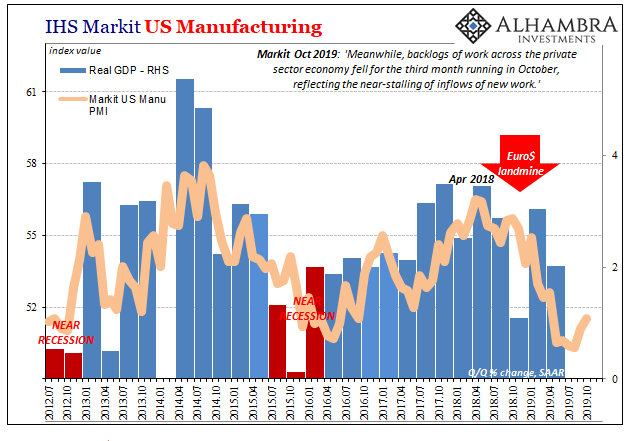

More Down In The Downturn25 Oct 2019

Monthly Macro Monitor: Doom & Gloom, Good Grief12 Oct 2019

Definitely A Downturn, But What’s Its Rate of Change?28 Aug 2019

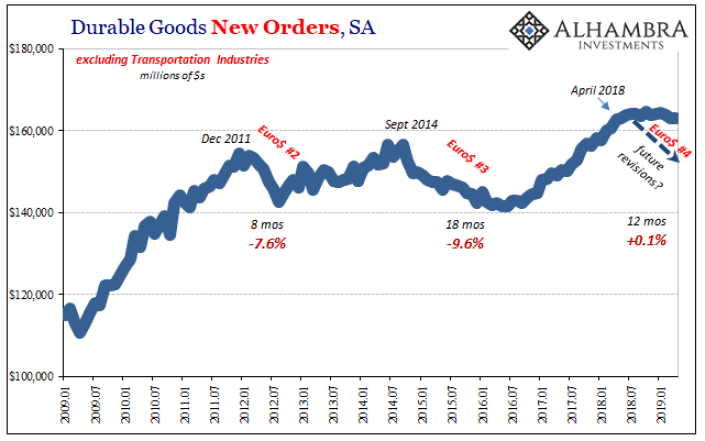

Durably Sideways28 Apr 2019

Slump, Downturn, Recession; All Add Up To Sideways22 Mar 2019

US Manufacturing Questions6 Feb 2019

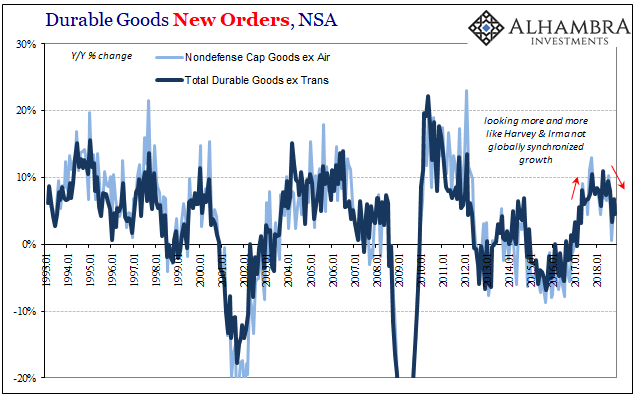

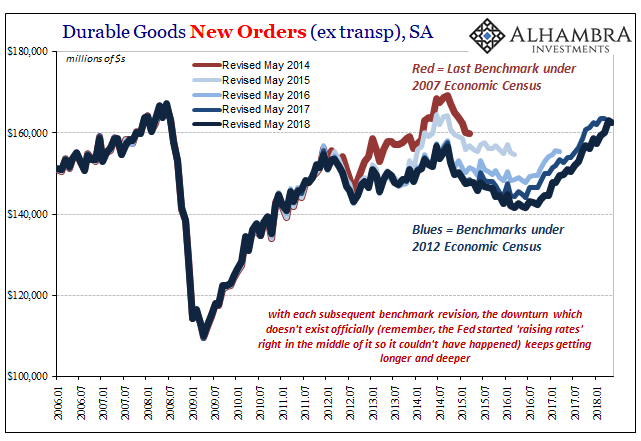

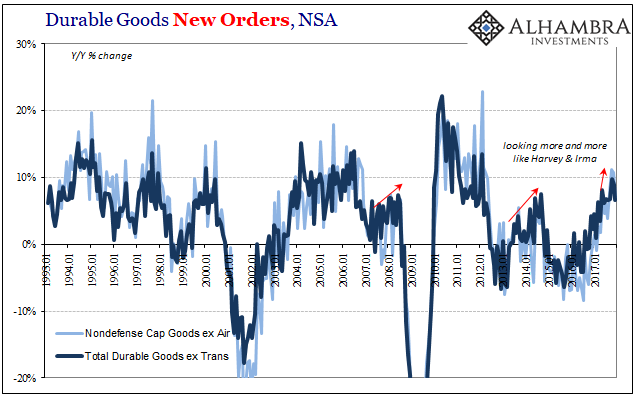

Revisiting The Revised Revisions30 Jun 2018

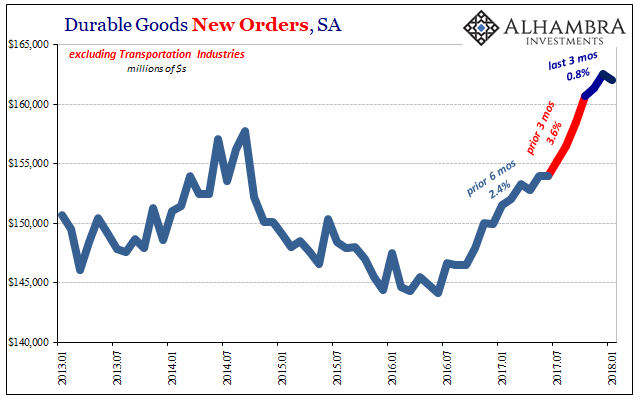

Durable and Capital Goods, Distortions Big And Small4 Mar 2018

December Durable Goods29 Jan 2018

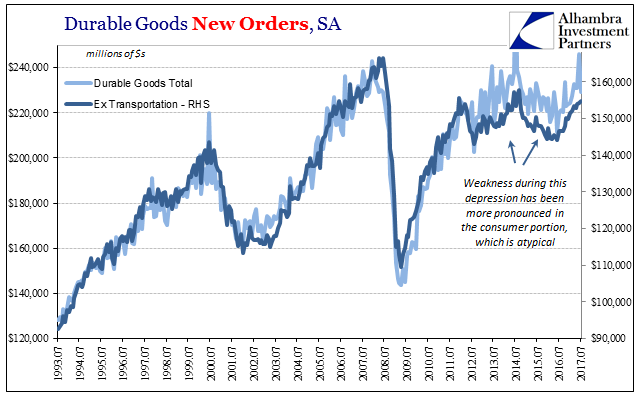

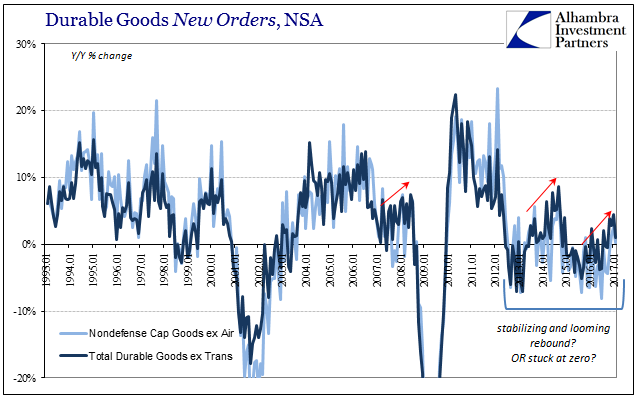

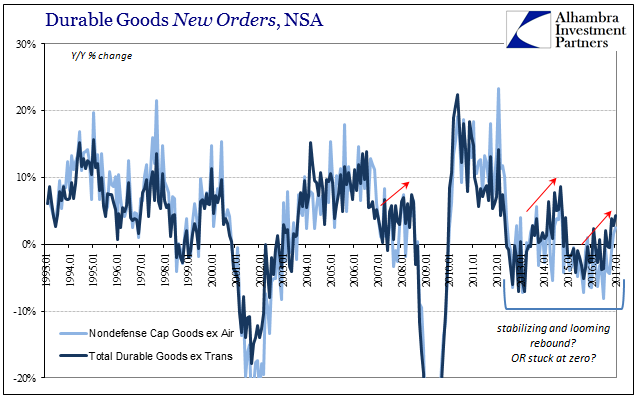

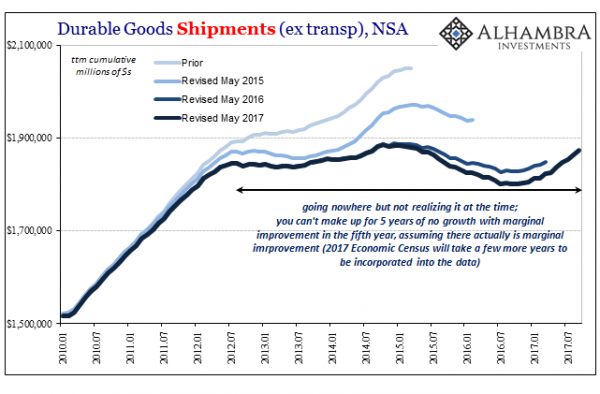

Durable Goods Only About Halfway To Real Reflation25 Nov 2017

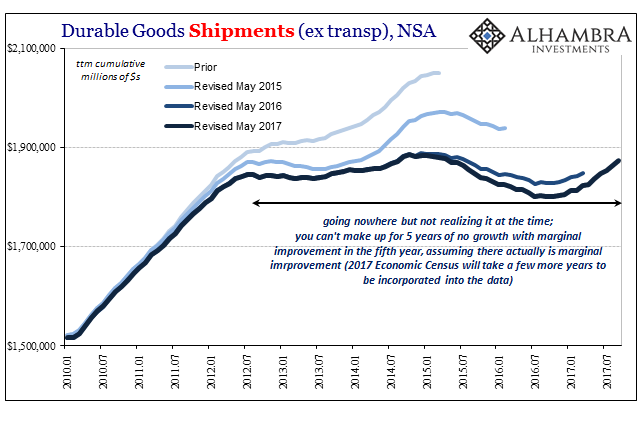

Subject To Gradation

Subject To Gradation31 Oct 2017

United States Durable Goods In July; Rinse, Repeat27 Aug 2017

Durable Goods After Leap Year25 Mar 2017

Bi-Weekly Economic Review

Bi-Weekly Economic Review13 Mar 2017

Durable Goods Groundhog28 Feb 2017